Ansell – Support

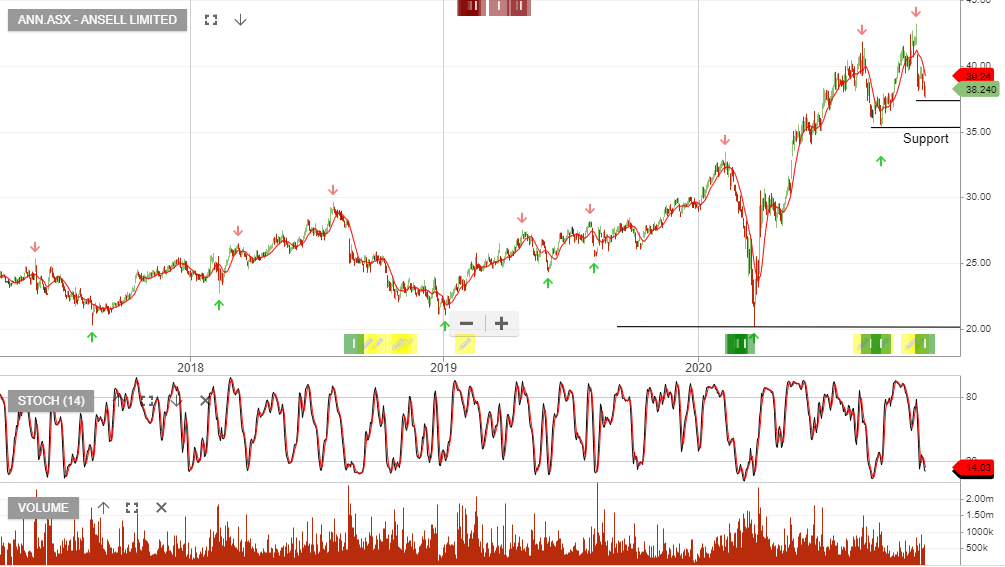

Ansell is under Algo Engine buy conditions and we see support building within the $35 – $38 level.

Ansell is under Algo Engine buy conditions and we see support building within the $35 – $38 level.

Appen is under Algo Engine buy conditions and we now add the stock to our watchlist. Monday I’ll update the financials and review the fundamental support for earnings growth in the current economic environment.

Newcrest Mining remains under Algo Engine buy conditions. We suggest investors accumulate NCM near the $29 support level.

The short-term momentum indicators have not yet turned higher and therefore close monitoring of the approaching buying support is advised.

APA is under Algo Engine buy conditions and we see support building at the recent $10.50 higher low formation.

APA goes ex-div 23c on 30 December.

Ramsay Health Care is under Algo Engine buy conditions and is a current holding in our model portfolio.

Valuation support within the $61 – $65 range.

The XJO is under Algo Engine buy conditions and we’ve shuffled the support up to 6498. A break below this may suggest that the defensive basket of BBUS, BBOZ & SNAS should be under consideration.

Ramsay Health Care is under Algo Engine buy conditions and is a current holding in our model portfolio.

Valuation support within the $61 – $65 range.

Cleanaway Waste Management is under Algo Engine buy conditions and is a current holding in our ASX model portfolio.

We see price support at $2.30 with an attractive, defensive yield.

APA is under Algo Engine buy conditions and we see support building at the recent $10.50 higher low formation.

APA goes ex-div 23c on 30 December.

Sonic Healthcare is looking oversold and we believe buying support will build within the $31 – $34 price range.

SHL has a large percentage of its diagnostic equipment revenue based in US Dollars. As such, the company will benefit from the lower Aussie Dollar.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453