National Australia Bank Limited

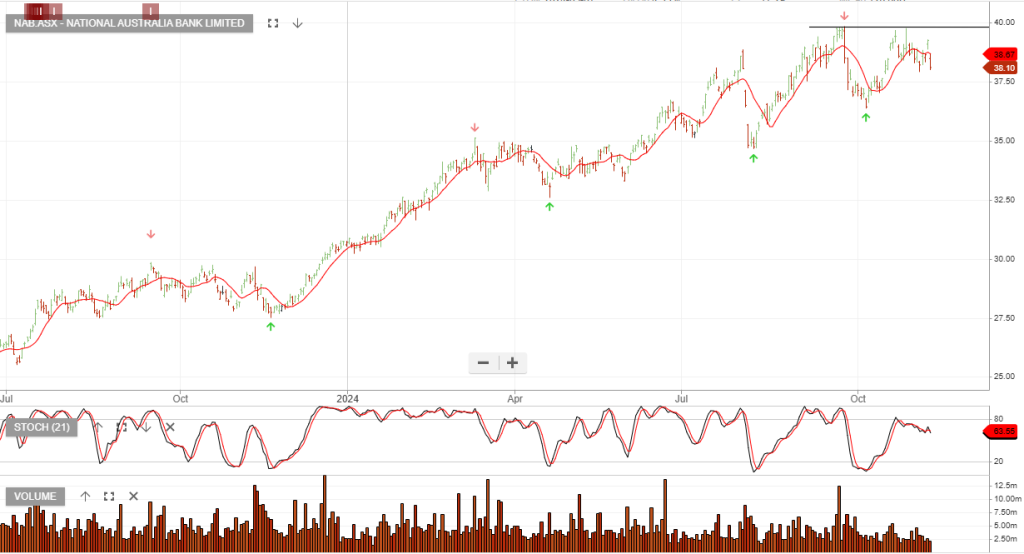

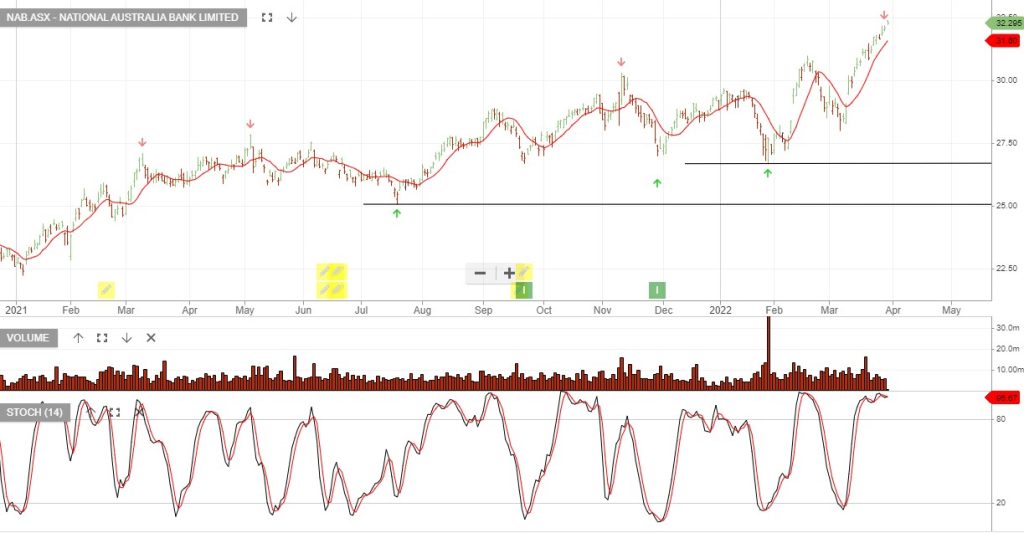

National Australia Bank: Buy with a protective stop-loss established at $40.39. This entry follows a technical signal as the bank continues to demonstrate market leadership among the “Big Four” financial institutions.

- NAB maintains a dominant market position as Australia’s largest business lender, providing a robust foundation for long-term credit growth.

- The bank continues to offer attractive fully franked dividends, supported by a strong Common Equity Tier 1 (CET1) capital ratio.

- Recent operational focus has remained on digital transformation and streamlining retail banking services to improve cost-to-income efficiency.

[/cb_decision]