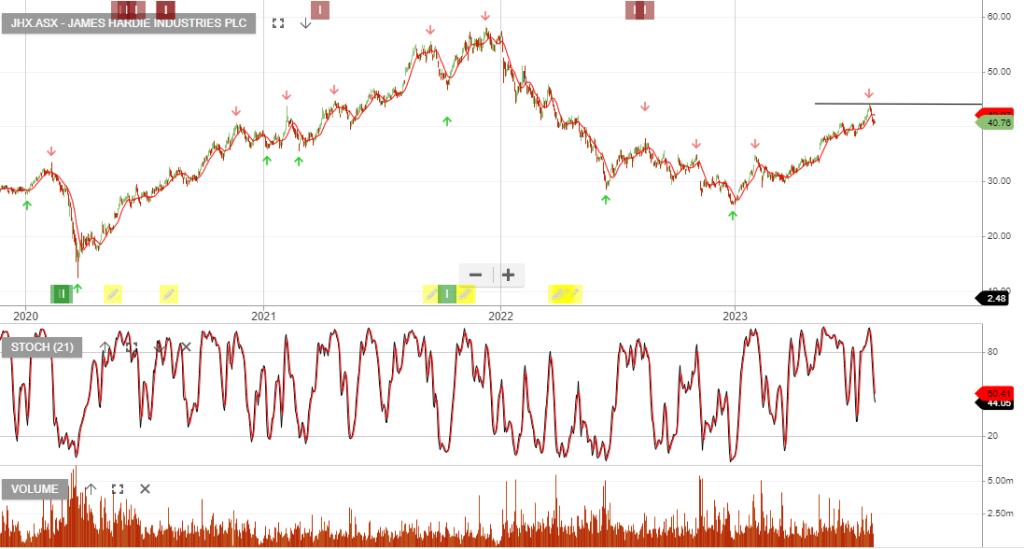

James Hardie Industries

James Hardie Industries is under Algo Engine buy conditions.

Full-Year FY26 Results – The building materials giant reported its FY26 full-year results this morning, beating underlying earnings guidance despite facing a challenging global macro environment.

Dividends: No dividend was declared or paid for the year.

Full-Year Net Sales: US$4.84 billion, up 25% (boosted by the AZEK acquisition). Siding & Trim organic sales decreased 2%. Statutory Net Profit: US$104.0 million, down 75% year-on-year, weighed down by restructuring charges, asbestos compensation claims, and AZEK integration costs. Adjusted EBITDA: US$1.27 billion, up 17%, exceeding the company’s prior guidance.

Outlook: For FY27, management targets pro forma Adjusted EBITDA growth of 4% to 8% (US$1.45–$1.50 billion) and free cash flow of at least US$500 million.