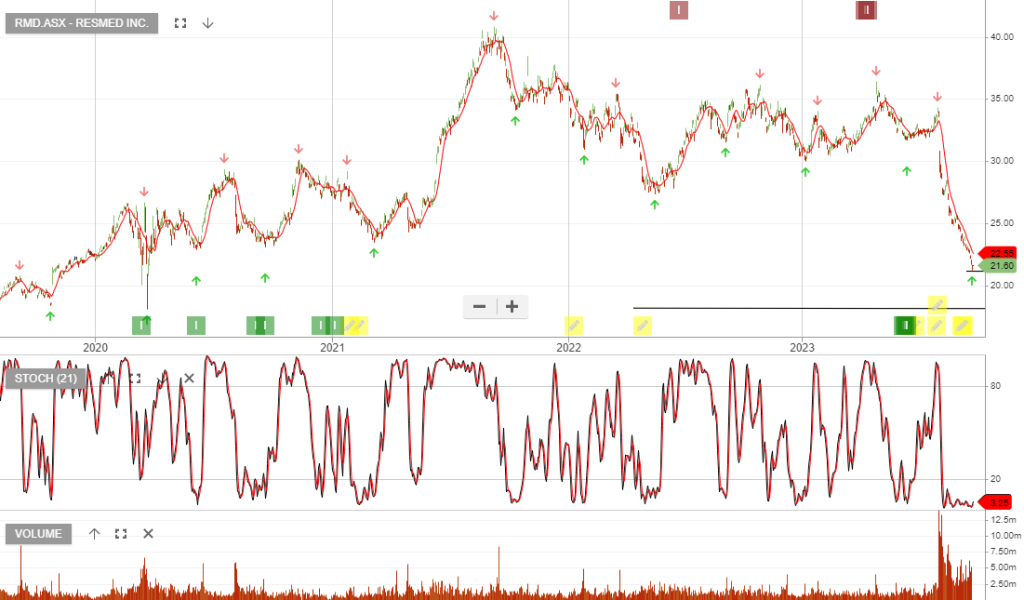

Resmed

ResMed : Buy with the stop loss $26.44

Update 2/7: Hold.

If you’re not already set in this one, consider buying and placing a tighter stop at $27.96

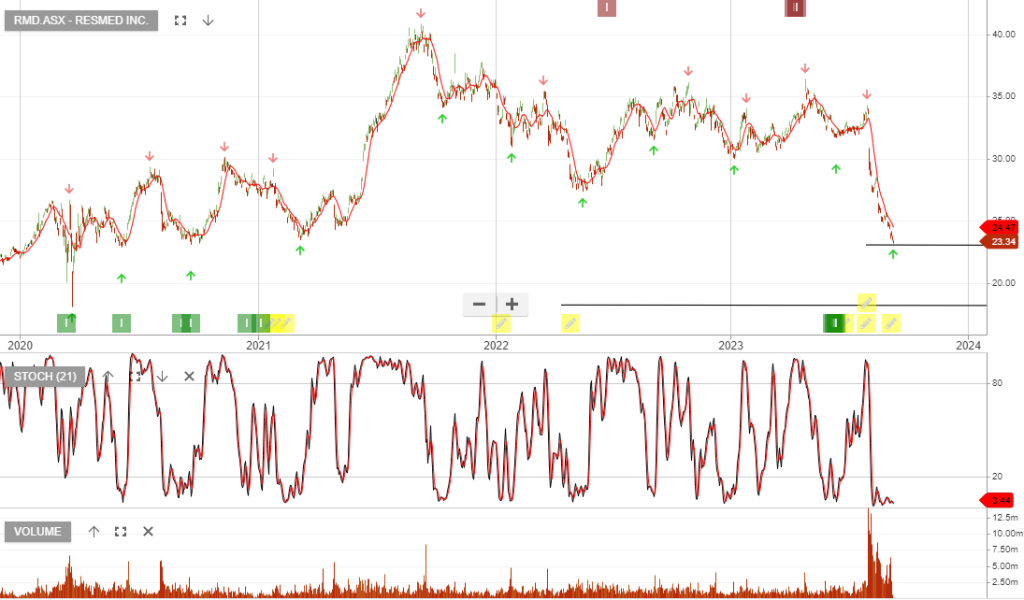

ResMed : Buy with the stop loss $26.44

Update 2/7: Hold.

If you’re not already set in this one, consider buying and placing a tighter stop at $27.96

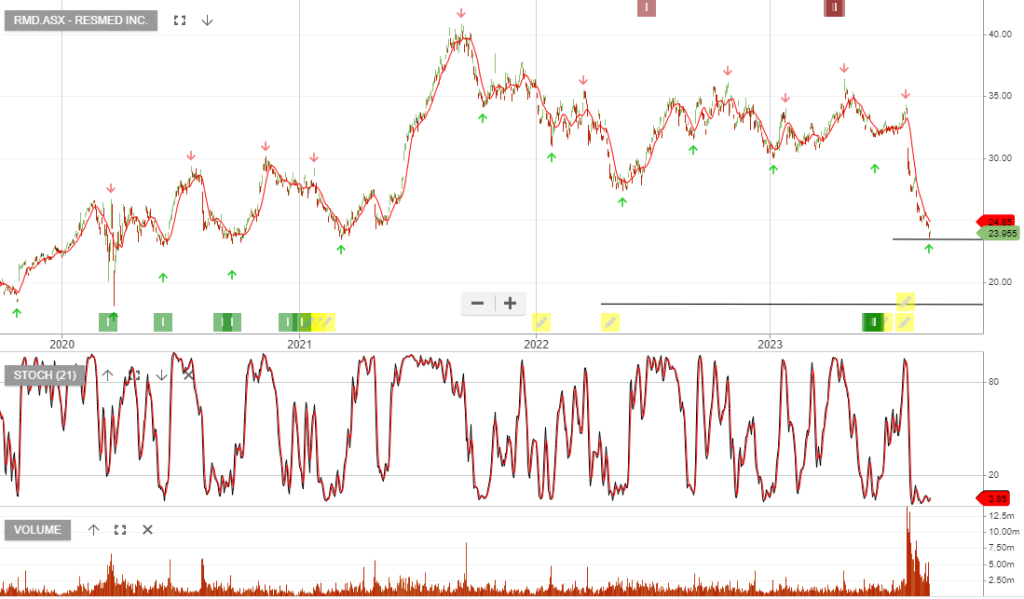

ResMed : Buy with the stop loss $26.44

ResMed is rated a buy, with the stop-loss at $27.81

ResMed add to watchlist and wait for a close above the 10-day average.

ResMed is due to report 4Q23E EPS Friday.

ResMed is due to report 4Q23E EPS Friday.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453