Macquarie Group: Buy

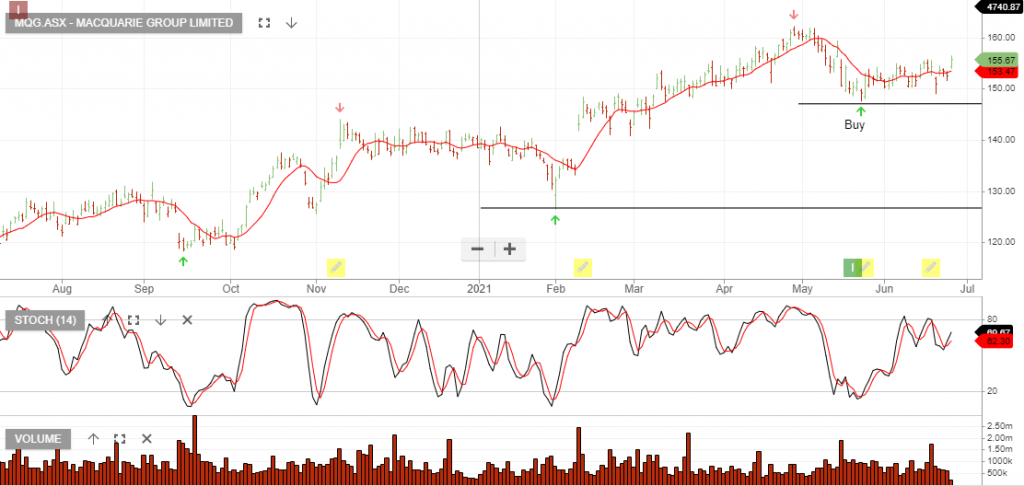

Macquarie Group is showing positive momentum after creating a higher low at $160.

Macquarie Group is showing positive momentum after creating a higher low at $160.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Macquarie Group is under Algo Engine buy conditions and is a current holding in our model portfolio.

Macquarie Group (MQG.AX) has provided an update on its guidance, in which it now expects 1H22 NPAT to be slightly down on 2H21.

The is a positive relative to the negative expectations that the market had for earnings to be down 10 – 15%.

A good outcome for the full year FY22 will be flat on FY21, which places MQG on 21x earnings and 3% dividend yield.

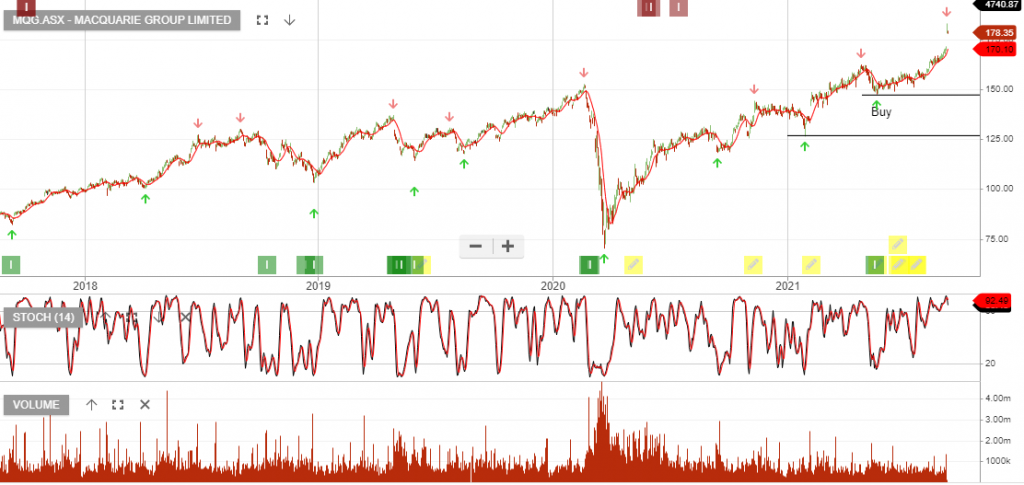

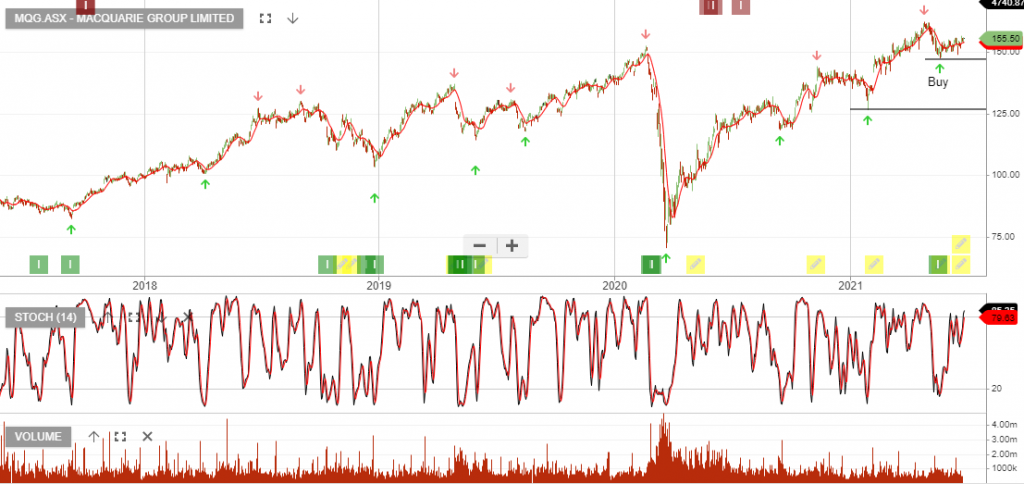

Macquarie Group is now under Algo Engine buy conditions following the recent price retracement from $162 down to $148.

We see further upside for the Macquarie share price and the stock remains our preferred sector allocation.

Macquarie Group is now under Algo Engine buy conditions following the recent price retracement from $162 down to $148.

We see further upside for the Macquarie share price and the stock remains our preferred sector allocation.

Macquarie Group is now under Algo Engine buy conditions following the recent price retracement from $162 down to $148.

Macquarie Group recently announced a net profit after tax attributable to ordinary shareholders of $3.01bn for the year ended 31 March 2021 (FY21), up 10 percent on the year ended 31 March 2020 (FY20).

Macquarie Group is now under Algo Engine buy conditions following the recent price retracement from $162 down to $148.

Macquarie Group recently announced a net profit after tax attributable to ordinary shareholders of $3.01bn for the year ended 31 March 2021 (FY21), up 10 percent on the year ended 31 March 2020 (FY20).

Macquarie Group is now under Algo Engine buy conditions following the recent price retracement from $162 down to $148.

Macquarie Group recently announced a net profit after tax attributable to ordinary shareholders of $3.01bn for the year ended 31 March 2021 (FY21), up 10 percent on the year ended 31 March 2020 (FY20).

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453