CIMIC – Earnings

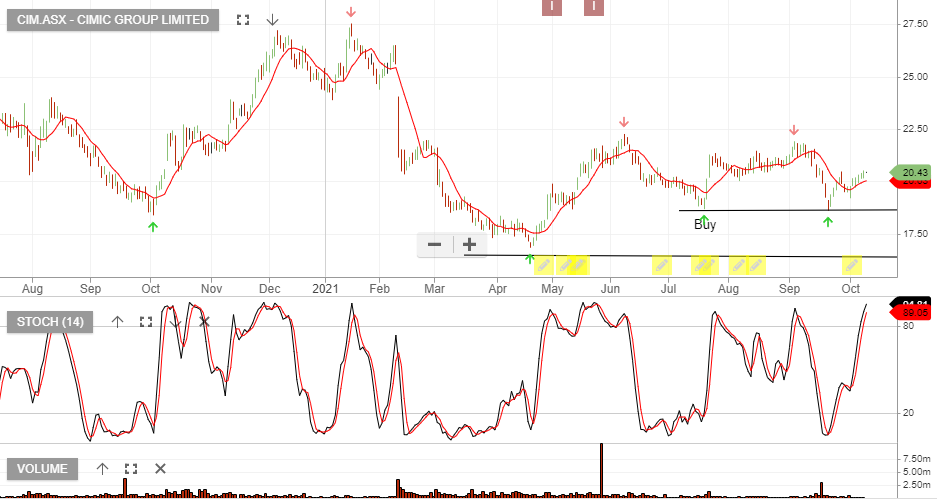

CIM:ASX is likely to see improved earnings in FY22 and we expect to soon see a recovery in the share price.

CIMIC is a high-risk counter-trend investment with the prospect of a multi-year recovery, once earnings hit an inflection point.

| Upcoming key dates | |

| Full year financial results | 10 February 2022 |