Ramsay Healthcare

Ramsay Healthcare

Ramsay Healthcare

Ramsay Health Care: first quarter revenue up 6.5 per cent and EBIT up 5.8 per cent.

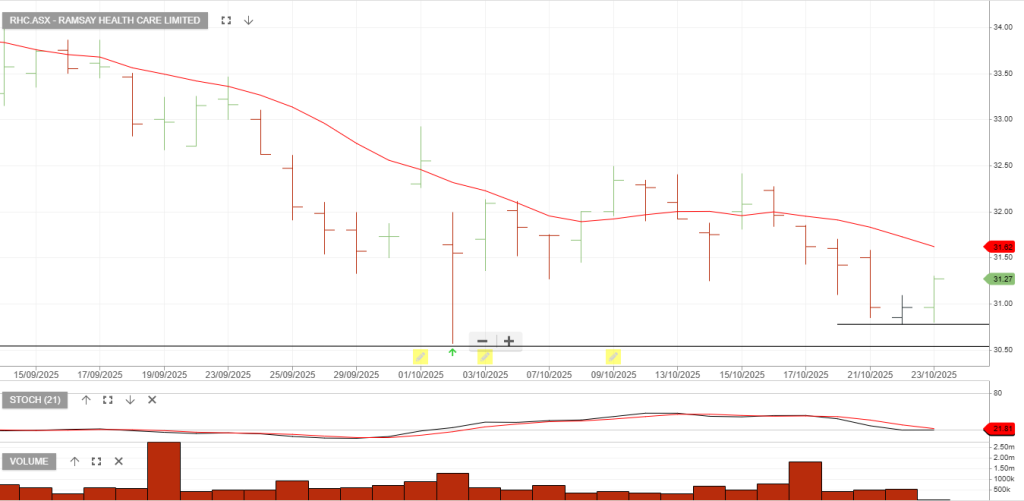

Buy on a move above the 10-day average.

Ramsay Healthcare

25/11 update: Ramsay Health Care jumped 11.3 per cent as it outperformed market expectations and tipped higher earnings this year, with first quarter revenue up 6.5 per cent and EBIT up 5.8 per cent, ahead of both RBC and consensus forecasts.

24/11 update: RHC is rated a buy with the stop loss at $31.00

Ramsay Healthcare

Ramsay Healthcare

Ramsay Healthcare

Ramsay Healthcare

Ramsay Healthcare

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453