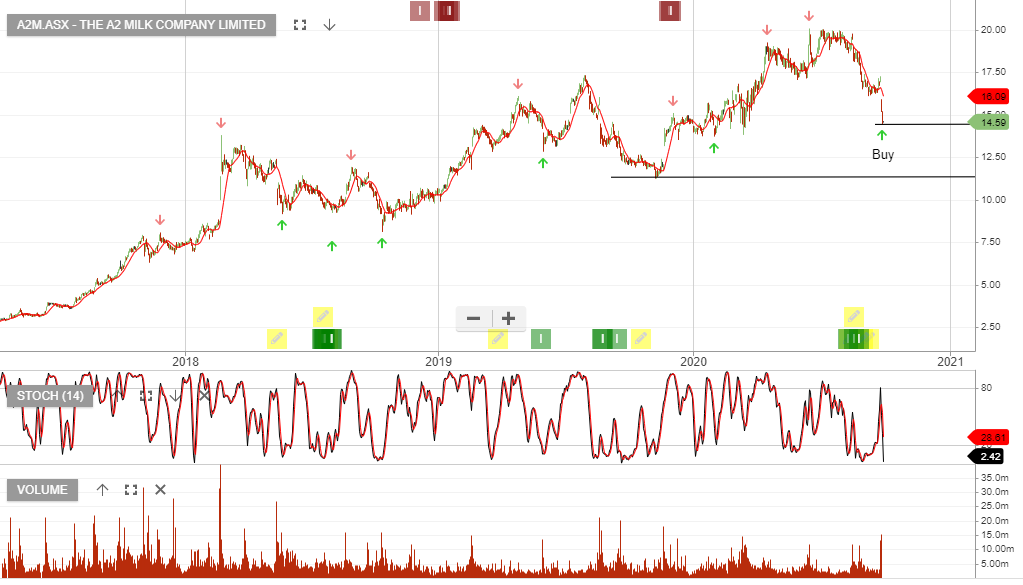

A2 milk December-half revenue will fall to between $725mn – $775mn, down from $807 million in the first half of 2020, and full-year revenues will likely be in the range of $1.8bn – $1.9bn, compared with revenues of $1.73 billion in 2020.

The guidance implies full-year EBITDA between $560mn and $590mn, which is up from the $550mn in 2020, but below prior consensus forecasts of $660mn.

$11.50 to $14.50 provides an accumulation range for A2 Milk.

Qube Holdings is under Algo Engine buy conditions and has now been added to our ASX model portfolio.

FY21 revenue is forecast to increase 3% to $1.95bn and EBITDA flat at $300m. Qube may start to deliver 8 – 10% EPS growth into FY22 and FY23, which will support the forward yield of 2%.

We see price support developing within the $2.25 to $2.50 range.

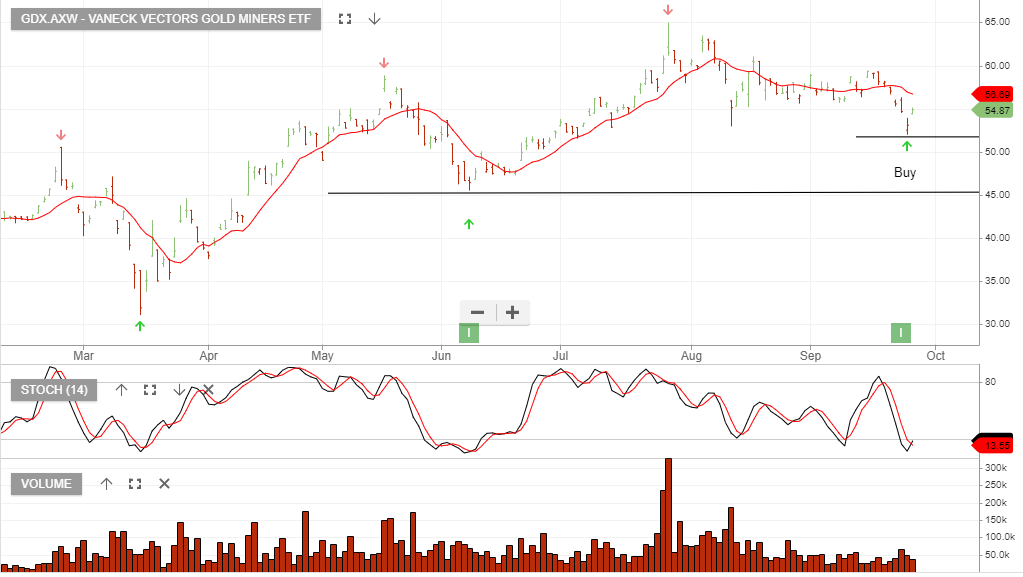

Gold Road Resources is under Algo Engine buy conditions and we expect buying interest to rebuild near the $1.50 support level.

A combination of lower gold prices in the spot market and the recently announced interruption to production has seen the GOR share price fall from the $2.00 highs reached in July.

Gold Road Resources Limited (Gold Road) reports an interruption to its September 2020 quarter production for the Gruyere Gold Mine (Gruyere) following a ball mill motor bearing failure. Gruyere is a 50:50 joint venture with Gruyere Mining Company Pty Ltd, a member of the Gold Fields Limited group (Gold Fields), who manage Gruyere.

The ball mill motor bearing failure occurred on a restart of the Gruyere processing facility after a scheduled maintenance shutdown. Upon detection of the failure, a specialist team was mobilised to site. Following a thorough inspection, the root cause of the failure has been determined, rectification measures have been taken and the available spare has been installed. As a result of the extended shutdown, production at Gruyere was impacted for 7 days after the planned shutdown, with normal processing operations resuming Thursday afternoon on 24 September.

All in Sustaining Costs (AISC) for Gold Road’s attributable share of production was expected to peak in the September 2020 quarter, with lower gold production as the operation transitioned to fresh rock processing, with the quarter’s costs impacted by reduced gold production. Configuration of the milling circuit for fresh rock processing required some additional plant downtime early in the quarter to maintain throughput rates.

Due to the ball mill motor bearing failure and additional plant downtime early in the quarter, Gold Road anticipates gold produced for the September 2020 quarter to be 53,000 to 57,000 ounces (100% basis). AISC for the September 2020 quarter are anticipated to be in the range of A$1,540 – A$1,590 per ounce.

As a result of this quarter’s production disruptions, full year production guidance for 2020 (100% basis) is anticipated at 250,000 to 270,000 ounces (previously 250,000 to 285,000 ounces) and Gold Road’s attributable annual AISC guidance is revised to between A$1,250 – A$1,350 (previously A$1,150 to A$1,250).