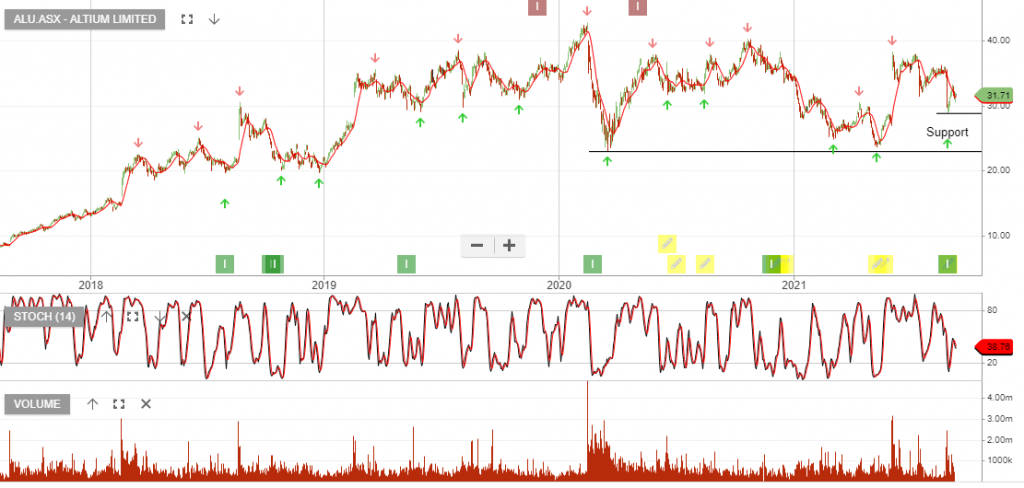

Altium – Buy Signal

Altium is under Algo Engine buy conditions.

Altium is under Algo Engine buy conditions.

If you’re an Investor Signals member and have been joining us on Monday night webinars, you would have made some changes to your portfolio allocations.

To protect portfolios we’ve taken the following approach (for members only)…

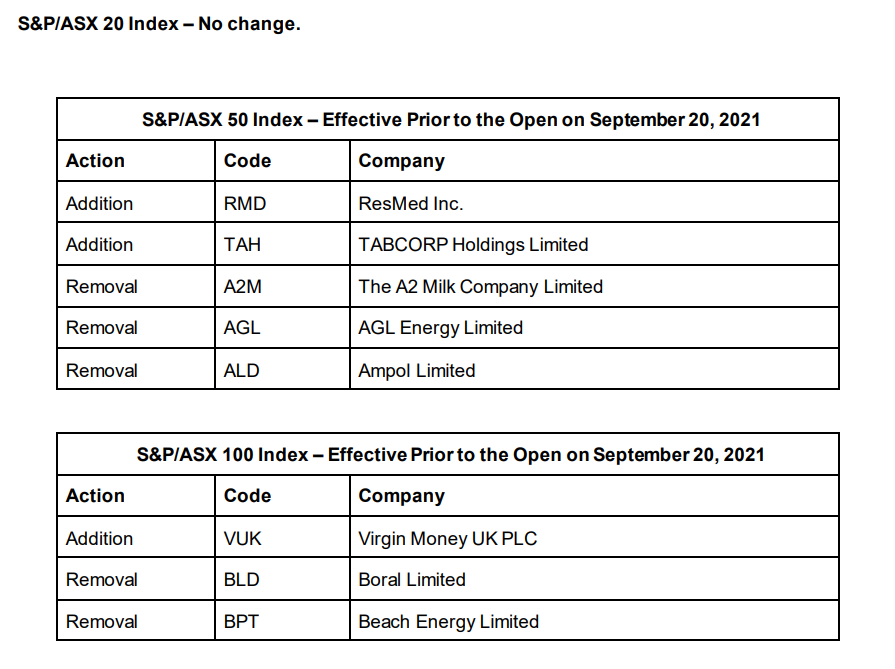

Index rebalance RMD and TAH are added to the top 50 index, both are under Algo Engine buy conditions.

A2M, AGL and ALD are removed, all three are under Algo Engine sell signals.

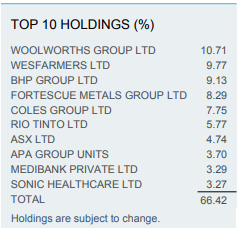

Coles Group is under Algo Engine buy conditions.

Investors should look to accumulate a position in Coles, within the highlighted price range.

BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

Altium is under Algo Engine buy conditions.

Aurizon Holdings is under Algo Engine buy signals.

Aurizon reported underlying earnings before interest taxation depreciation and amortisation (EBITDA) of $1.48 billion and told investors to expect underlying EBITDA of between $1.42 billion-$1.5 billion in fiscal 2022.

Zip Co is under Algo Engine buy conditions.

PayPal Holdings said it would acquire Japanese buy now, pay later firm Paidy in a $2.7 billion largely cash deal, taking another step to claim the top spot in an industry experiencing a pandemic-led boom.

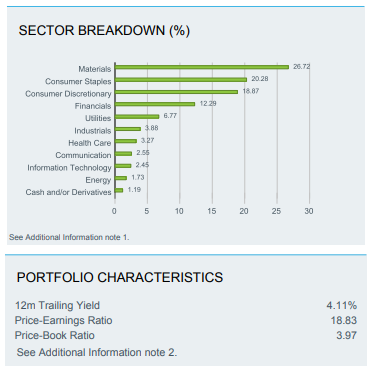

iShares S&P/ASX Dividend Opportunities is now under Algo Engine buy conditions and has been added to our ETF model portfolio.

The fund aims to provide investors with the performance of the S&P/ASX Dividend Opportunities Accumulation Index, before fees and expenses. The index is designed to measure the performance of 50 ASX listed stocks that offer high dividend yields while meeting diversification, stability and tradability requirements.

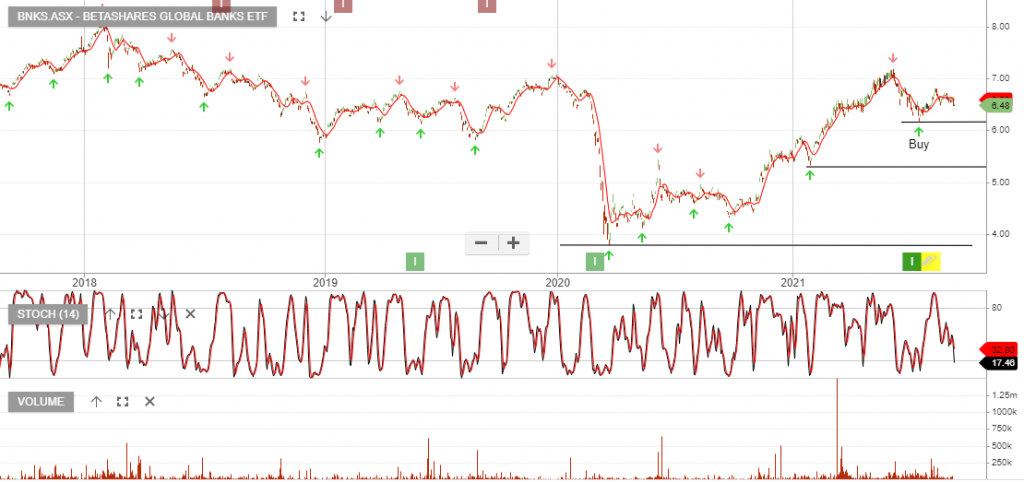

US bank profits fell 8.3% to $70.4 billion in the second quarter of 2021 as firms slowed their reductions in credit loss provisions, the Federal Deposit Insurance Corporation reported.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453