Greatland Resources

Greatland Resources is under Algo Engine buy conditions.

In company news, Greatland Resources jumped 11.1 per cent to $10.84 as the miner lifted its Telfer gold resource by 150 per cent to 8 million ounces, driven by extensive drilling and a maiden high-grade resource at West Dome Underground.

Nvidia

NVIDIA Corporation – Common fundamentals are strengthening, with accelerating revenue growth, expanding margins, and robust demand for key products. Their data center business, especially networking, is a standout, with networking revenues up 267% and the segment maintaining strong momentum.

FY2027 Q1 signals continued acceleration, with 77% YoY revenue growth and gross margin projected at 75%. Forward P/E of 20 is now below the sector, supporting a reiterated Strong Buy rating.

AMP

A$150m share buyback (~5% of market cap) is a positive signal, helping address investor concerns post-FY25 and reinforcing capital management discipline.

Core business outlook remains constructive, with expected strong Platform inflows, revenue growth, and improving trends in Super & Investments (S&I) outflows.

Rio Tinto Limited

Rio Tinto a new position in Rio Tinto Limited at an entry price of $153.23, with a protective stop-loss price established at $142.20. The company continues to maintain its status as a global mining powerhouse, recently reporting robust production volumes across its core iron ore and copper divisions.

- Rio Tinto is a primary supplier of high-grade iron ore from the Pilbara region, benefiting from low-cost operations and strong industrial demand in Asia.

- The company is aggressively expanding its footprint in future-facing commodities, including significant investments in copper and lithium projects to support the global energy transition.

- Rio Tinto remains a key dividend-payer in the ASX 200, supported by a disciplined balance sheet and high operational margins.

[/cb_decision]

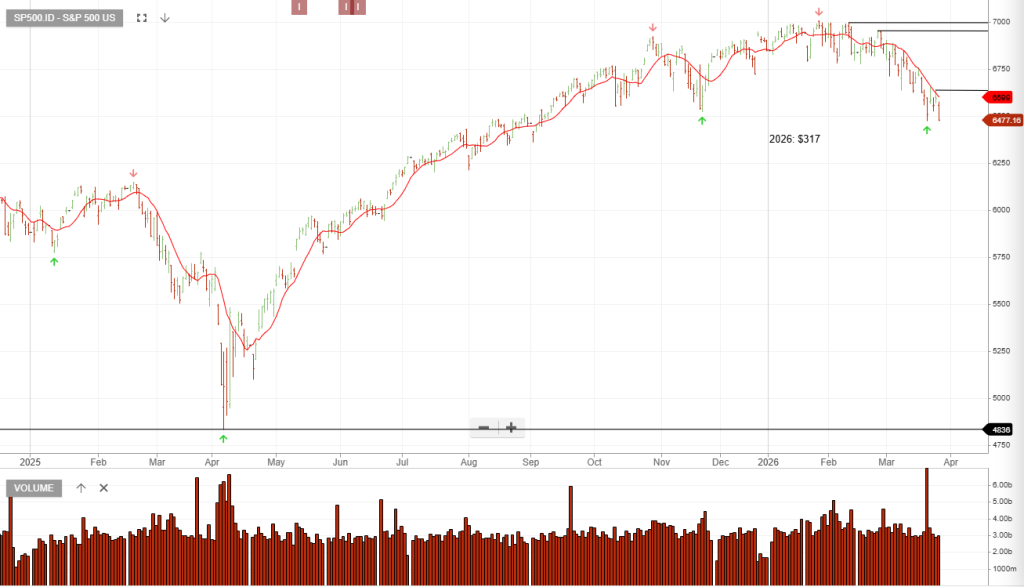

S&P500

S&P500

ASX200

XJO

Iluka

China Tech ETF

IGO Limited

IGO opened a new position at an entry price of $7.83, with a risk-management stop price set at $6.52.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453