IAG

Insurance Australia Group is rated “hold”.

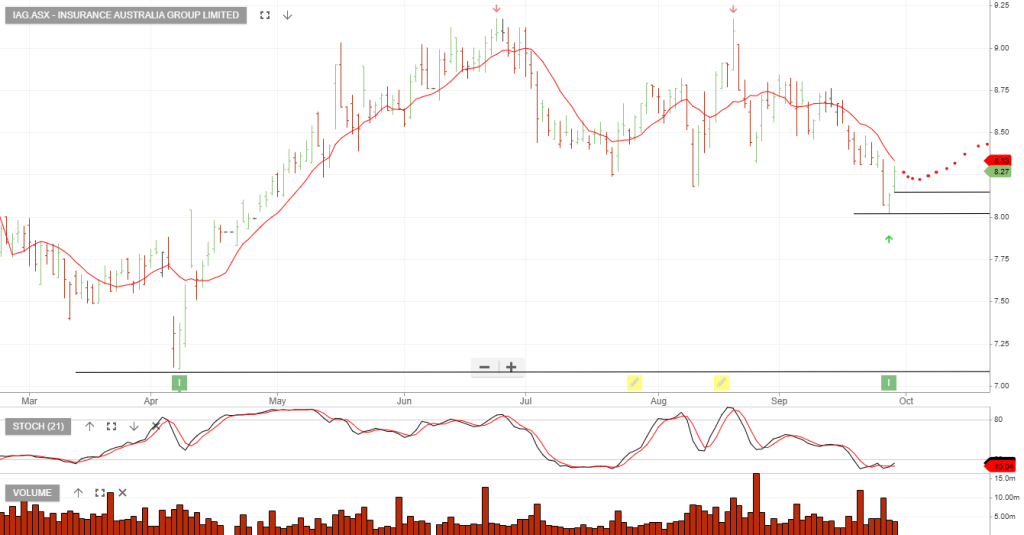

Increased buying activity in IAG.ASX over the last 10 days (approx. March 5 – March 15, 2026) is driven by a combination of corporate capital management, dividend timing, and a market reassessment of the insurance sector’s valuation.

### 1. Active $200M Share Buy-Back

The most direct cause of increased buying is IAG’s ongoing on-market share buy-back.

- Volume: Daily ASX notifications show consistent repurchasing. As of March 16, IAG reported more than 1.7 million shares had been bought back in the recent period.

- Impact: This provides a steady baseline of “forced” buying volume, supporting the share price and reducing the total supply of shares.

### 2. Interim Dividend Payment

IAG paid its 12.0 cents per share interim dividend on March 13, 2026.

- Reinvestment: Many institutional and retail investors automatically reinvest dividends back into the stock, particularly through Dividend Reinvestment Plans (DRP), which creates a concentrated spike in buying demand around the payment date.

- Yield Attraction: At current levels, the dividend yield remains a key draw for income-focused investors looking for “defensive” financial exposure.

### 3. Rebound from “AI Sell-off” (Mean Reversion)

In early March, insurance stocks (including IAG, SUN, and QBE) faced selling pressure due to fears that AI would disrupt traditional underwriting and compress margins.

- Overreaction: Over the last 10 days, market sentiment has shifted to the view that this sell-off was overdone. Analysts have highlighted that IAG was trading at a ~12% discount to its fair value (est. $8.23 vs current $7.25).

- Recovery: The stock has rallied 10.35% in the last 7 days, climbing from a low of $6.39 to approximately $7.25.

### 4. Positive FY26 Guidance Upgrades

Confidence has been bolstered by IAG’s structural growth following its RACQI acquisition.

Profitability: Management expects a reported insurance profit of $1.55 billion – $1.75 billion, signaling that premium increases are successfully offsetting claims inflation and weather-related costs.

Growth: The company recently upgraded its FY26 Gross Written Premium (GWP) growth target to approximately 10%.