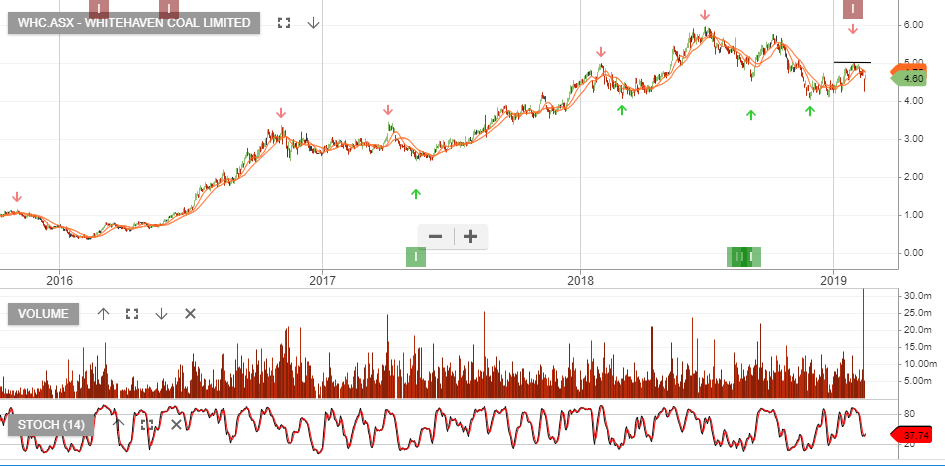

Whitehaven Coal

Whitehaven Coal is open position in the ASX200 Trade Table.

As an investor looking at Whitehaven Coal (WHC.ASX) in March 2026, here are the critical updates and fundamental metrics you should know following the recent H1 FY26 results and significant credit rating news.

### 1. Key Catalysts & Recent News

- Credit Rating Milestone (March 12, 2026): Whitehaven recently secured investment-grade credit ratings from all three major agencies (S&P: BB+, Fitch: BB+, Moody’s: Ba1), with a stable outlook. This is a major turning point that allows the company to refinance its $1.1 billion acquisition facility on much more favorable terms, potentially saving $30–$40 million in annual interest costs.

- Capital Management: An interim fully franked dividend of 4.0 cents per share was paid today (March 13, 2026). Additionally, the company has launched a new $32 million share buy-back program through June 2026, signaling management’s view that the stock remains undervalued.

- Asset Integration: The integration of the Daunia and Blackwater metallurgical coal mines (acquired from BHP) is progressing well, diversifying Whitehaven’s revenue toward higher-margin steelmaking coal.

### 2. Fundamental Valuation Metrics

Whitehaven currently appears undervalued relative to its historical averages and industry peers:

- P/E Ratio: ~11.0x – 12.4x (Industry average is closer to 20x).

- EV/EBITDA: ~5.4x (Significant discount to the industry median of ~8.2x).

- Price to Book (P/B): ~1.34x.

- Intrinsic Value: Analysts estimate a DCF fair value between $11.30 and $14.45, implying potential upside from the current price (~$9.05).

### 3. H1 FY26 Earnings Recap (Feb 19, 2026)

- Revenue: $2.5 billion (Down from $3.4B in H1 FY25 due to lower year-on-year prices).

- Underlying EBITDA: $446 million.

- Statutory Profit: $69 million (Impacted by non-recurring items; underlying loss was $19M).

- Production: Managed ROM production was solid at 20 million tonnes, with costs controlled at ~A$135/tonne.

### 4. Market & Sector Outlook

- Coal Prices: Global thermal coal prices have surged roughly 25% year-to-date (Newcastle benchmark ~$135/t) due to energy supply disruptions in the Middle East and “fuel switching” from gas to coal in Europe and Asia.

- Analyst Sentiment: The consensus remains a “Hold” among 14 major analysts. While some brokers (like JPMorgan) remain cautious with “Sell” ratings, others see the credit upgrade and metallurgical coal exposure as strong long-term drivers.

### Summary for Investors

Whitehaven is currently at an operational and financial inflection point. The transition to a “metallurgical-heavy” producer and the recent credit boost provide a safety net against thermal coal price volatility. However, long-term ESG-related selling pressure and decarbonization trends remain the primary structural risks.