On 13th of January, the first of the major US financial institutions begin announcing their fourth quarter earnings results. Bank of America, JP Morgan and Wells Fargo will be the key results to watch.

The rise in US financials has been significant by any measure; multiples have expanded ahead of what investors are hoping to be record levels of profit and bullish forward guidance. The US financial sector has been boosted by the expectation of higher interest rates, deregulation and high trading earnings to drive profits.

However, we have concerns: economic growth in the US is not that strong, the year-over-year GDP growth rate was only 1.7 percent in the third quarter, S&P500 average year on year EPS growth was only +4% in the third quarter and it’s had to see growth improve dramatically in 2017, especially with a stronger US dollar.

Chart – Bank of AmericaChart – JP MorganChart – Goldman Sachs

Looking across the financial horizon, it appears by many measures that 2016 is ending with similar dynamic as 2015: G-7 stock indexes are at or near their highs, the USD Index is on an upswing, the US Federal Reserve lifted rates causing bond yield to firm and Gold prices are stabilizing after a sharp November drop.

As such, the financial media is content to wrap up the year by only focusing on the price action from the last two months and ignoring the two-way market volatility experienced in the previous 10 months.

Looking into 2017, it’s worth noting that as optimistic as the end of 2015 outlook was, the SP 500 started 2016 under pressure and dropped over 250 points, or 12% by January 20th.

We have identified three potential flashpoints which may trigger a significant correction from the recent post-US election rally during the month of January.

First, the Italian banking sector continues to sag as political manoeuvring has greatly outpaced the progress of any meaningful economic solution. At this point, the focus has been on the bailout of Monte Paschi Bank. Recent “stress tests” have shown that the solvency gap needed to rescue Italy’s oldest lender has grown from €5.5 billion to over €10 billion.

The immediate contagion risk has spread to 10 other EU banks who are holding substantial Monte Paschi debt obligations.

The second potential flash point stems from recent liquidity shocks in the Chinese bond market. Credit conditions have tighten sharply over the last two weeks as over 25 corporate bond issue face a potential default.

This pressure has seen 2-year swap rates spike higher, which has forced the Peoples Bank of China (PBoC) to inject over $60 billion into the short-term money market just to keep the secondary Treasury market from triggering a trading halt…….like it did on December 15th.

Many investors overlook the impact that even temporary credit shocks can have on global equity markets. However, according to some estimates, the global bond market has more than tripled in size over the last 15 years and now exceeds over $ 100 trillion.

By contrast, Dow Jones Research puts the value of the global stock market at just under $65 trillion. In the US alone, bond markets make up over $40 trillion in value, compared to less than $20 trillion for the domestic stock market. In this sense, as G-7 Central bank policies have removed traditional market anchors, a liquidity or solvency shock in a domestic bond market can have a profound impact on global equity markets.

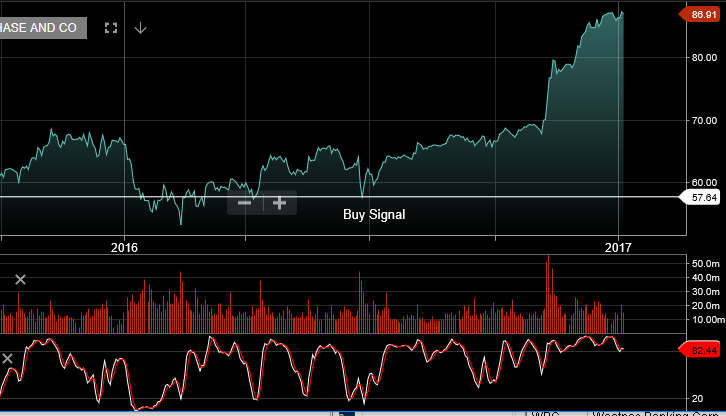

The third potential flash point involves the US earnings season. US companies will begin reporting in the fist week of January with JP Morgan , BoA and Wells Fargo leading the banks starting on January 13th. Forward estimates suggest that the post-election rally has lifted many of the banking names into price valuations which the earnings reports may not be able to support.

It’s not our base case that an external market shock will trigger a protracted sell off in global equity prices and derail the bull market structure during 2017. However, we feel that it’s important for investors to be aware of the potential of such risks and have a strategy in place to protect portfolio holdings during a market correction.

A product which fits this description is the BetsShares BEAR Exchange traded fund (ETF). The BEAR EFT Gives investors a simple and accessible way to obtain ‘short’ exposure to the market.

If you would like to learn more about how the Beta-Share BEAR ETF can protect the long-side of your portfolio, or if you just want to learn how to profit from a downside correction in the ASX 200, get in contact with us and we’ll be happy to introduce you to this dynamic product.

Going into 2017, one of the biggest decisions investors face is what portfolio weighting to allocate to Australian banks.

Over the past three years, the Australian banking sector has grown to represent over 30% of the ASX 100 capitalization.

This growth has been supported by record bank profits, weakness in other sectors and the chase for yield by offshore investors as central banks in Europe, Japan and the USA have pushed interest rates to historically low levels.

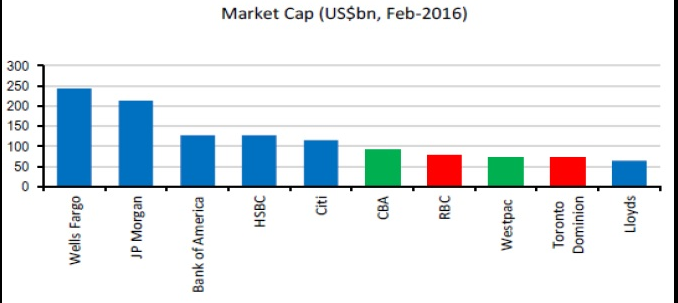

This has contributed to all four of Australia’s primary banks now being in the top 15 global banks by market capitalization, despite their relatively small footprint in the global financial system. In fact, as of February 2016, both CBA and Westpac were listed in the top 10 global banks in terms of market capitalization.

Over the past five years, Australian banks have been very successful in generating profits from their domestic branches which operate in a snug banking oligopoly. Competition from non-bank lenders hasn’t increased materially in the mortgage area and bad debts remain at manageable levels.

Nevertheless, Australian banking shares (while offering high dividend yields) are likely to face a fairly constrained pricing environment and higher loan losses, should the domestic economy continue to slow in 2017.

It’s been reported that international fund managers have been systematically, shorting Australian banks based on the belief that the domestic housing market is overvalued and primed for the same dramatic decline which occurred in Ireland, Spain and the USA over the last 10 years.

Furthermore, a growing number of analysts are suggesting that protracted weakness in the local economy will burst the housing bubble, contributing to the Government losing its AAA credit rating and putting downward pressure on Australian bank share prices throughout 2017.

Our base case is not quite that grim. However, we do expect to see limited upside to the share prices of the big four banks from current levels and eventual rotation into healthcare companies and yield names.

From a technical perspective, we expect to see price resistance for the four major banks around the following levels: WBC $33.50, CBA $86.00, ANZ $32.50, NAB $32.00.

Flash points for the global equity markets in 2017 remain Italian Banks, Chinese Economy & uncertainty around Trump presidency.

Japan continues to struggle to shake off deflationary pressures as the November consumer price index fell for the ninth straight month. Bank of Japan Governor,Haruhiko Kuroda rejected claims the BOJ’s yield curve control and 2% inflation target may be too ambitious and that the central bank has room for more economic stimulus.

China’s 6.5% economic growth target may not be maintained, especially if it continues to compound the rising debt issues the country faces and creates too much risk.

During 2016 we’ve been bullish on the Chinese equity markets which performed inline with our forecasts. The strength and the breakout in the Japanese equities on the other hand, caught us a little by surprise.

The breakout in the Nikkei has been fuelled by the BOJ’s broad-based equity ETF being program and the recent weakness in the Yen.

Let’s take a quick look at a few names that should prosper from the Christmas period spending activity. In the US I’ve focused on Amazon and FedEx as two relevant examples and domestically, I’ve looked at Harvey Norman and JB HI-FI.

We had buy signals from the algo engine on these names and our preference was the long position in HVN, which has now rallied 10% from the November low.

US stock Indexes closed modestly lower during Thursday’s thinly-traded preholiday session. With the lower trading volumes expected over the holiday and US Earnings season commencing in a few weeks, investors seemed reluctant to bid up prices of indexes that are already hovering near all-time highs.

The SP 500 and the NASDAQ Composite booked their first consecutive losses in three weeks, as the post-election rally has lost momentum over the last few sessions.

It’s worth noting that since November 4th, all three of the major US Index have posted respectable gains with the Dow Jones 30 rising 11.2%, the SP 500 up 8.3% and the NASDAQ Composite gaining over 9%.

Therefore, it’s really not surprising to see stocks take a breather going into the Christmas break.

Shares of FedEx are down 3% at $192.80 in after market trade as the parcel delivery giant fell short of fiscal Q2 earnings estimates after the NY close today.

FedEx announced Q2 earnings of $2.80 per share on revenue $14.9 billion, while the market was expecting earnings of $2.90 with revenue climbing to $14.95 billion.

Total operating margin shrank to 7.8% from 9.1% a year ago, due to the FedEx “Ground” unit’s network expansion and increased purchase transportation rates, as well as higher IT expenses. Looking forward, adjusted FY 2017 earnings are still seen in the $12.00 to $12.25 range.

On balance, FedEx has offered good shareholder value this year climbing over 25% since January. We would expect to see buyers at, or around, the initial support area of $173.00

Political events and Central Bank policy moves have been driving global financial markets over the last two months. During this time, direct influence from weekly economic data seems to have diminished. With dealing desks starting to thin and investors looking to the holidays, this is likely to remain the case over the next two weeks.

But even as financial markets slip into holiday mode, there are several powerful trends that are worth watching. Three of these trends have been particularly vigorous: The USD climb against the JPY, the rise in the US 10-year yields, and the rally in the SP 500 have all been very robust. In fact, these three markets have risen six weeks in a row and finished higher over nine of the last 11 weeks. Similarly, the USD Index and US 2-year yields have risen, while Gold has fallen, in seven of the last 11 week.

The key issue now is whether these trends will be extended, or if a profit taking phase will be seen into the end of the year. Arguments that these trends have gone too far too fast are now several weeks old. And even though technical readings are even more overstretched, there aren’t reliable fundamental arguments for taking aggressive positions in the opposite direction……….not yet, anyway.

The basic psychology of these recent trends suggests the new US administration will act swiftly to enact a comprehensive (fiscal) stimulus package; which will allow US stock valuations to expand and the US Dollar to appreciate vis-a-vis higher domestic interest rates.

On balance, we expect the current trends of higher US stocks, firm US Dollar and a steepening yield curve to continue, even as market flows edge into holiday mode.

The US Dollar Index has rallied to its strongest level in more than 13 years as the market continues to digest the ramifications of the FED’s more aggressive interest rate policy trajectory.

Financial markets weren’t surprised when the FOMC announced an increase to the Fed Funds target from .50% to .75%. The move had been widely expected since the October meeting and the FED funds futures had been pricing in a 100% percent certainty of the move.

However, financial markets were not expecting the FED’s “dot plots” to reflect expectations of at least three more rate moves during 2017. Since Wednesday’s announcement, we have seen the EUR/USD trade back below the 1.0400 level and the USD/JPY break the 118.50 level for the first time since February.

It’s important to remember that with a stronger USD comes headaches for other Central banks around the world who will incur a higher cost of servicing USD denominated debt. The stronger USD also poses a risk for the US economy especially in an environment of rising US finance costs.

In short, if the new administration doesn’t come up with a viable stimulus package quickly, the US economic growth story could fade. This could translate into a significant correction in US Stocks, US Treasury rates and the Greenback.

However, before hitting the sell button on long US asset trades, it is important to realize that for the dollar rally to end, dollar bulls need a reason other than year end profit taking to give up on their trades. The latest round of economic reports continues to support the bullish move in the US Dollar.

Despite a stronger USD, manufacturing activity in the NY and Philadelphia regions accelerated. Consumer prices also grew 0.2%, which was in line with expectations and jobless claims dropped to 254K from 255K. The NAHB housing market index jumped to its highest level in 11 years.

The stronger USD over the last month should have softened these data: weakened the trade figures, manufacturing activity and made it more difficult for the Fed to achieve its inflation target, but we need to see evidence of that before selling the USD and US Stocks.

In the meantime, US assets remain in a strong uptrend targeting 20,000 in the DJ 30 and a move in the direction of parity for the EUR/USD.

The US Stock market slipped lower on the back of the Federal Open Market Committee’s (FOMC) policy announcement today. The market wasn’t surprised by the FED’s 25 basis point increase in the Overnight Fed Funds target, but the “Dot Plot” forward guidance shows policymakers are looking for 3 rate hikes of 25 basis points in 2017.

This view is more aggressive than the 50 basis point move the FOMC discussed back in September, which pushed equities lower and lifted the yield on the US 10-year treasury notes to a three year high of 2.57%. It’s worth noting that the 10-year yield traded at 1.35% in July; which means the yield on the US benchmark treasury note has essentially doubled in less than 5 months.

In her post-announcement press conference, FED chief, Janet Yellen, described the move as a “very modest adjustment”, which suggests this year’s forward guidance may mean another move on rates as early as May 2017.

We don’t see this a trend-changer in the major US stock indexes. However, we do see scope for a near-term correction back to the 19,450 level in the DOW Jones 30 and a move back to 2190 in the SP 500.

Chart – Dow Jones

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.