Buy Amcor

We recommend investors buy Amcor at $14.90.

We recommend investors buy Amcor at $14.90.

Since December 1st, the price of WTI Crude Oil has rallied over 14%.

Just in the last 5 days the WTI price has risen 5% from $60.25 to a 3.5 year high today of $63.50.

Recent reductions in crude inventories combined with Geo-political tensions in the Middle-East have support prices.

However, there have been many analyst sceptical that this will be a protracted rally in Crude prices.

This scepticism can be seen in the price action of some of the local oil-based names.

Despite the 5% rise in WTI over the last week, shares of OSH have dropped by 2.5% to $7.90, and the share price of WPL and STO have been consolidating off their recent highs and look to be pointing lower.

We urge caution on the sustainability of the recent run up in Crude prices and would suggest exiting long exposure to WPL, STO and OSH

Woodside

Santos

Oil Search

Based on the positive macro data, cost savings, benefits from US tax changes and the transformation program Ansell announced, we see upside to Ansell’s upcoming earnings result on the 12th February.

ANN currently trades at 17x 2019 earnings and a forward dividend yield of 2.7%.

We’re buyers on near-term weakness ahead of the upcoming earnings result.

Ansell

ALL’s exposure to recurring revenue is increasing, although the business remains exposed to cyclical trends.

The market’s response to Aristocrat acquiring Big Fish has been mixed.

We see the the deal as 3 – 4% EPS accretive in 2019 and will help to underpin EPS growth of 20%, placing ALL on a 2019 dividend yield of 3.3% and a PE of 20x earnings.

ALL is among the best performing stocks in our ASX 50 model and we advise investors to look for near-term buying support along with the next Algo buy signal.

Aristocrat

SUN is due to release its 1H18 results on Thursday 15 February.

We are expecting NPAT of $510m, which is around 50% of the full year target of $1.05b

FY18 EPS growth should be around 5% and the dividend will remain flat at $0.73 placing Suncorp on a forward yield of 5.3%.

Our Algo Engine triggered a sell signal on the recent “lower high” formation and, therefore, we do not hold this name in our model.

Last week we mentioned that shares of TAH had reached overbought levels in the $5.75 area.

The share price has dropped 5 days straight and is now approaching the buy zone at $5.30.

We expect the synergy between TabCorp and Tatts to enrich the value of the company and believe TAH is a reasonable addition to investor portfolios for 2018.

TAH will go ex-dividend on February 7th for 12.5 cents per share. At $5.30 per share, this pencils out to a 4.7% yield.

TabCorp

Our Algo Engine triggered a buy signal in AGL on the 22nd August at $22.64.

Considering the recent “higher low” formation at $24.00, we recommend investors add AGL to their portfolios.

AGL is a current holding in the ASX 50 model portfolio and we’ve added a covered call option to enhance the yield.

AGL pays a 41 cent in dividend on the 23rd of February.

AGL

Our ALGO engine triggered a buy signal in QANTAS on December 8th at $5.25.

Since then the share price dipped to a low ow $4.84 on a combination of higher oil prices and a stronger AUD/USD.

With analysts forecasting QAN to post record earnings of 10.32% over the course of 2018, investors could expect shares of the flying kangaroo to reclaim some of last year’s upside trajectory.

Internal momentum indicators are pointing higher and the next key technical target is the mid-December high of $5.45.

QANTAS

With bond yields likely to stabilise and strong passenger growth numbers, (across Australia’s east coast), we see SYD as a buying opportunity.

We also recommend selling covered call options to enhance the yield.

SYD is expected to release full year traffic numbers in late January 2018.

Sydney Airport

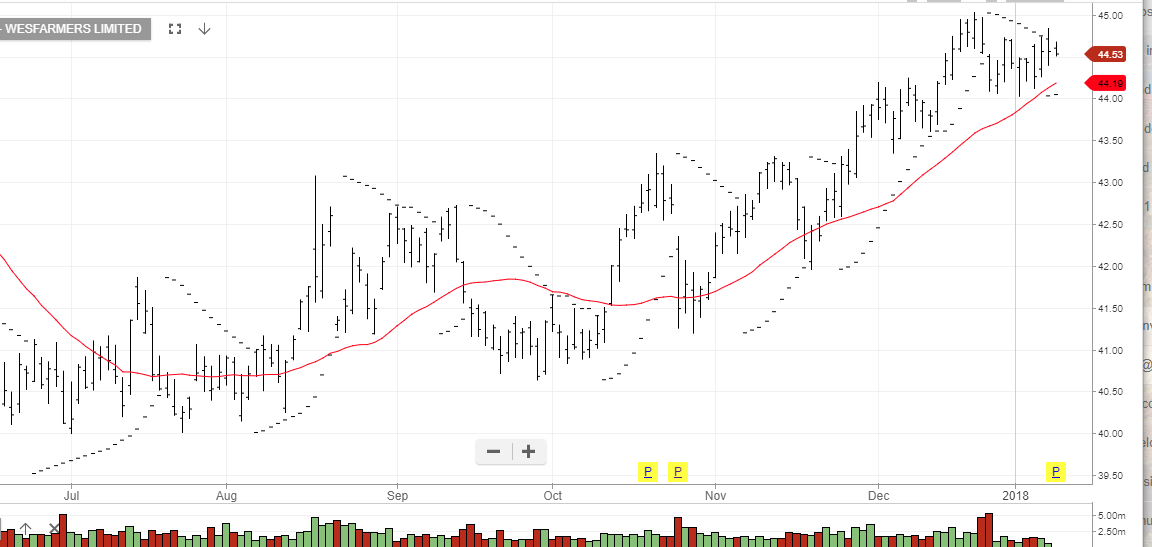

Wesfarmers (WES) has agreed to sell its Curragh coal mine in Queensland to US miner Coronado Coal Group for $700 million plus a value share agreement.

We suggest the company is likely to reduce borrowings to some degree, as earnings have been reduced, and subject to franking credits may return capital to shareholders.

We believe a reasonable strategy is to sell $45.00 June call options for $1.02 credit and expect to keep exposure to the $1.03 dividend declared on the 20th February.

Wesfarmers

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453