Inghams

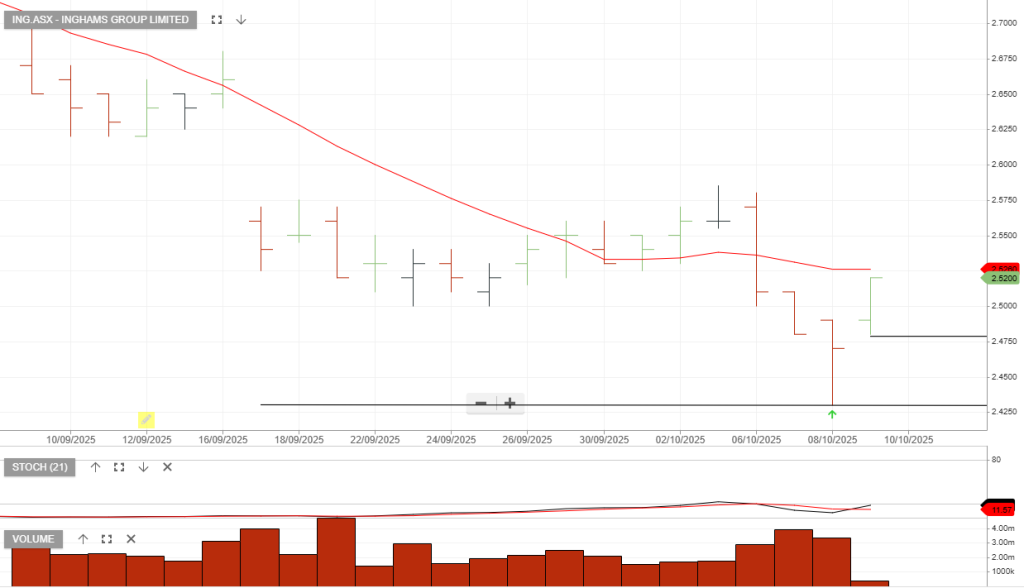

Inghams Group shares rose 6.2% to $1.80 following a trading update that reassured investors about the company’s full-year outlook despite significant external headwinds.

Although Inghams has struggled over the past 12 months (with the share price down over 50% in that period), the market reacted positively to signs of “stabilising” trading conditions and the company’s ability to maintain its earnings forecast despite the spike in diesel and logistics costs.

FY26 Guidance & Financials

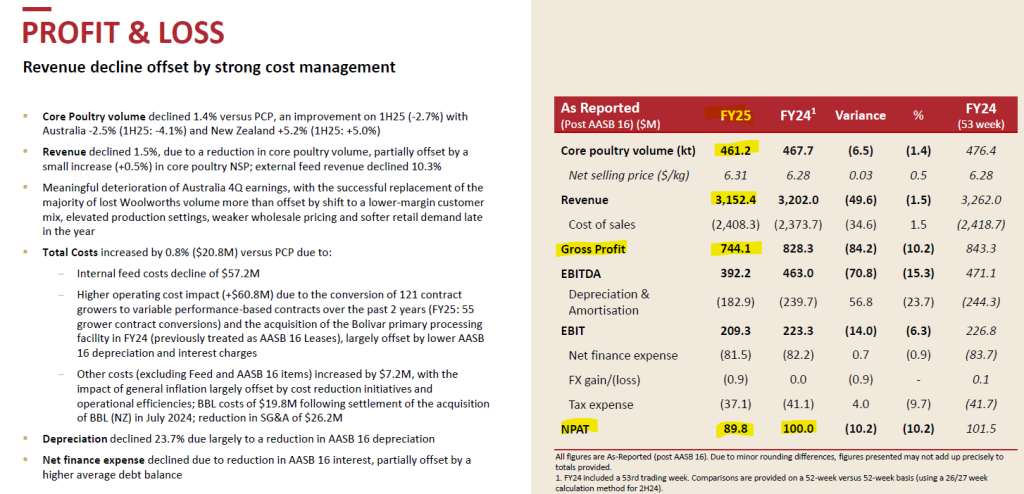

- EBITDA Reaffirmed: Inghams maintained its FY26 underlying EBITDA (pre-AASB 16) guidance of $180 million to $200 million.

- Previous Cut: This guidance had been revised downward in February 2026 (from a previous $215M–$230M range), so the reaffirmation provided the market with much-needed stability.

- Operational Momentum: For the first nine months of FY26, group poultry volumes rose 1.1%, and net selling prices also increased by 1.1% compared to the prior corresponding period (PCP).

Strategic & Defensive Measures

To protect its margins against fuel and packaging inflation, Inghams is executing several key initiatives:

- Cost-Cutting Program: Targeting $60 million to $80 million in annualised savings.

- Inventory Management: Reduced frozen inventory by $25 million, improving cash flow and system balance.

- Capital Expenditure: Revised FY26 CapEx guidance to approximately $80 million.