After taking a US$ 1.1 billion write-down on its GLNG project in Queensland, Santos posted a full-year loss of US$ 1.05 billion. No interim dividend was paid.

The oil and gas producer claims their free cash flow is at a Crude Oil price of US$36.50 per barrel, which is considerably lower than current levels.

The share price is essentially unchanged on the day. Longer-term investors can look for buy interest to return near the November lows at $3.50.

ASX Limited reported continued profit growth for H1 2017, up 3% to $219 million. Earnings per share was posted at $1.13 per share, which is 2.9% higher than a year ago.

The exchange operator declared a fully franked dividend of $1.02 per share, which pencils out to a 90% pay out ratio.

ASX also announced a 2.8% increase in operating revenue to $386.6 million, which is a 10.4 million increase from the previous reporting period.

Solid growth in Derivatives, OTC products and the sharp increase in ETF interest has underpinned the company’s forward guidance.

However, we see a potential “double top” pattern on the daily charts dating back to the August highs of $52.40 and would look for a pull back in the share price.

Medibank Private announced its net profit rose 1.9% in the half-year ending December 31st. The profit of $231.9 million compared to the $227.6 million earned in the year-ago period.

Directors reported an interim dividend of 5.25 cents per share out of earnings per share of 8.4 cents.

However, Medibank shares are down over 3.5% today as the company announced operating profits fell 6.4% to $250 million.

Higher claims by members and amortization on a new information technology system pushed health insurance operating profits down 8.2% to $249.4 million.

Initial chart support for the stock will be found in the $2.60 area, which will place MPL on a 4% forward yield. We own the stock in client portfolio’s and we’ve sold covered calls to enhance the yield.

Shares of Origin Energy continue to slide after announcing yesterday that the company will take a $1.031 billion impairment charge on the APLNG gas export project in Queensland. This was the largest part of a broader $1.9 billion post-tax write-down.

Origin raised the bottom end of its forecast range for annual EBITDA by 3% to $2.45 billion, but kept the top end of the forecast at $2.62 billion.

Origin shares are down over 2% so far today at $7.10. We see initial support coming in at or near the $6.88 level.

Our Algo Engine created a buy signal in September 2016 at $5.00

Stronger retail revenues helped Sydney Airports lift its 2017 guidance as 2016 annual profits were reported up 13.2% to $320.9 million.

The company announced that it will pay a full-year dividend of 31 cents per share for 2016 as total revenue climbed 11% in the year ended December 31st.

Total 2016 revenue was announced at $1.365 billion from $1.229 billion during the year ago period.

Forward guidance was higher, but slightly negative as the company forecast a 2017 dividend of 33.5 cents per share versus the street’s expectation of 34 cents per share. EBITDA rose 8.2% to $1.08 billion, and operating margins are running at 8.2%.

Total passenger numbers increased 5.6% to 41.9 million , with international passenger numbers rising 8.8% to 14.9 million.

Technically, the share price should find support at the $6.00 area, which is also the 30-day moving average.

Our Algo Engine created a short signal in December at $6.70.

Telstra shares are down over 4% in early trade as Australia’s largest telecommunication company announce half-yearly profits down 14.2% and revenue 3.6% lower.

The company reported half-yearly profits of $1.79 billion compared to $2.09 billion this time last year. Revenue fell to $12.8 billion from $13.3 billion over the same period of time.

Their EBITDA of $5.18 billion was at the low end of earlier guidance, which is a sign that Telstra is undergoing a difficult transition to the post-NBN world.

The company announced an interim dividend of 15.5 cents per share, fully franked, which returns $1.8 billion to shareholders.

Our Algo Engine created a short signal in January at $5.27

Wesfarmers‘ officials have credited their conglomerate structure for a 13.2% increase in half-year net profits to $1.57 billion. This result was well above the street’s expectation of $1.47 billion.

The company announced it will increase its interim dividend to $1.03 from 91 cents, payable on March 28th. Wesfarmers’ revenue grew by 4.3% to $34.9 billion, and EBIT were up 15.1% to 2.42 billion.

The strongest results from the conglomerate came from the industrial division, where earnings rose from $22 million to $377 million, largely from the $256 million turnaround in resources as coal prices moved higher during the quarter.

On the other side of the ledger, Coles’ same store sales grew by 1.3%, but lower prices meant revenue from the supermarket remained steady and earnings fell 6.8% .

Shares of Commonwealth bank have opened 2% higher to $84.50 after reporting a record first-half profit of $4.9 billion.

The result was 6% higher than the previous record reported in the first half of last year. An interim fully franked dividend of $1.99 was declared, which was 1 cent higher than expected.

Upside price momentum could be tempered as the bank announced net interest margin was lowered to 2.11% from 2.15% and their wealth management division saw a net profit drop of 34% compared to the same period last year.

SCG and WFD went ex-dividend yesterday at $0.105 and $0.125, respectively. With both names we’ve added tight covered calls to boost the cash flow to 10 – 12% on an annualised basis.

Ansell is a relatively new addition to portfolios and yesterday’s earnings result was slightly disappointing. Again, we’ve been aggressive with the covered calls so we’re not looking for too much on the upside with ANN and we collected between $0.80 to $1.20 for the covered calls. We will look to exit on a rally back towards $23 by April/May.

Amcor reported a terrific earnings result with underlying growth running ahead of market expectations at 5%. This could accelerate up to 8 – 10% in the second half. This supports our $15.50 price target.

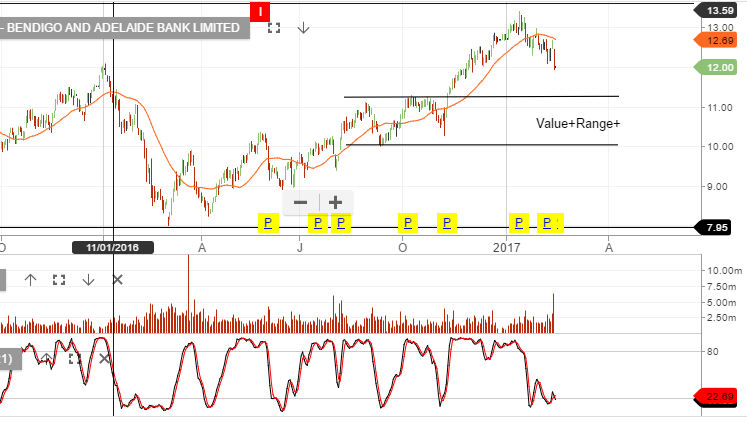

CBA’s earnings result tomorrow will be key for the banks. Thus far NAB and BEN have failed to deliver growth on the revenue and profit lines. We shorted BEN from $13.00 and we’ve been aggressive with selling call options over the top 4 banking names.

AZJ reported earnings in-line with market expectations. We remain cautious of the group’s high payout ratio with almost 100% of earnings being paid in dividends. This looks unsustainable in the medium term.

Tomorrow we will be focused on the earnings results for BLD, CBA, CPU, CSL, SHL and WES.

Chart – AmcorChart – Bendigo Bank

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.