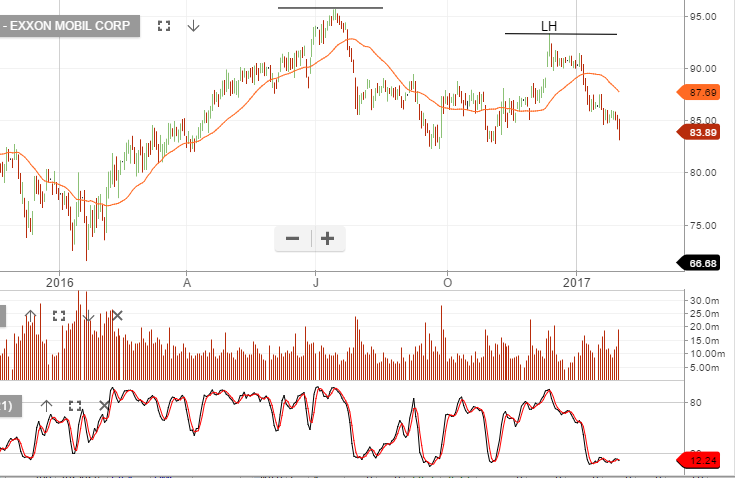

Exxon Q4 Results

Shares of Exxon Mobil hit a 4-month low of $83.10 after the company missed Q4 earnings and revenue expectations.

The company announced earnings of 41 cents per share on revenue of $61.1 billion. This compares to expectations of 70 cents per share on revenue of $61.4 billion.

The year-over-year data was mixed as Exxon earnings fell from 67 cents per share, but revenue rose from $59.8 billion against this time last year.

An upstream asset impairment charge of $2 billion, related to dry gas operations in the Rocky Mountain region, impacted Q4 as well as full-year earnings.

From a technical perspective we’re in a lower high structure with the next significant level of support near $80.00