Caltex Trade Recommendation

Caltex delivered upbeat profit guidance following strong performances in Lytton and Marketing & Supply divisions. Fy17 revenue $16b, EBIT $900m on EPS of $2.30 and DPS of $1.20. This represent year on year underlying growth of around 10%.

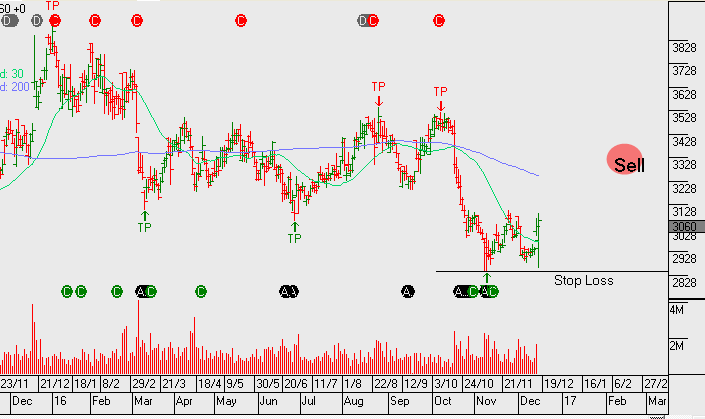

The chart below shows the market’s favourable reaction to the updated guidance with CTX rallying $1.40 from yesterday’s session lows. CTX trades on Fy17 PE of 13x and 4% dividend yield.

Here is our strategy recommendation on Caltex…

Buy CTX at market, sell May $32.50 call for $1.00 credit. March dividend will be $0.50+

Total return if exercised 13%+ in 5.5 months.