Strong Buy Signals

Woolworths, Woodside, Medibank & Origin look like they’re setting-up as strong buy signals.

Other names which we view favourably from recent ALGO alerts include, SYD, TCL & GPT.

Woolworths, Woodside, Medibank & Origin look like they’re setting-up as strong buy signals.

Other names which we view favourably from recent ALGO alerts include, SYD, TCL & GPT.

Recent price action in the local ASX market suggests we’ve entered a period of heightened volatility and potential for downside risk. Since posting the high for-the-year at 5945.00, the index for Australian shares has dropped almost 4%.

Looking across the spectrum of ASX top 100 stocks, we have found several names which can offer defensive value in a broadly sideways to lower share market.

These include: IPL, MPL, WOW, CTX, QBE, SHL, SYD, TCL, AMC, and IAG.

We consider these stocks to have the potential for moderate capital growth and, combined with a buy/write strategy, will offer 10 to 12% cash flow on an annualized basis.

ASX: XJO Index

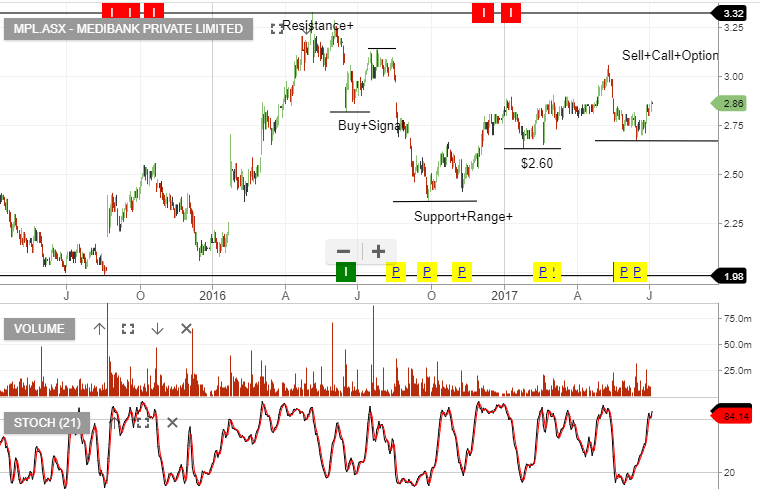

The ALGO engine triggered a buy signal on yesterday’s close for MPL at $2.72.

Internal momentum indicators are showing an oversold condition, which doesn’t rule out a test of the January lows near $2.60.

As a defensive name in an increasingly uncertain market, we suggest buying shares of MPL and using a derivative overlay strategy to enhance the returns.

We still see limited revenue growth and material resistance in the $3.00 area. However, with the 4% dividend yield and income from the option premium, we see the stock as positive income contributor to client portfolios.

Medibank

We’ve been buying MPL and selling at-the-money covered call options to deliver an annualized cash flow of 10%+

There’s limited revenue growth, limited profit growth and a 4% dividend yield. However, we see the stock as a defensive income contributor to client portfolios.

In addition to the 10% cash flow from the dividend and option income, we’re allowing for a small capital gain over the next 4 months.

Medibank Private announced its net profit rose 1.9% in the half-year ending December 31st. The profit of $231.9 million compared to the $227.6 million earned in the year-ago period.

Directors reported an interim dividend of 5.25 cents per share out of earnings per share of 8.4 cents.

However, Medibank shares are down over 3.5% today as the company announced operating profits fell 6.4% to $250 million.

Higher claims by members and amortization on a new information technology system pushed health insurance operating profits down 8.2% to $249.4 million.

Initial chart support for the stock will be found in the $2.60 area, which will place MPL on a 4% forward yield. We own the stock in client portfolio’s and we’ve sold covered calls to enhance the yield.

Medibank is struggling with top line growth of 1.5%, meanwhile underlying cost growth is running at an average of 5%.

We were recent buyers of MPL at $2.35 and with the stock hitting our $2.60 price target, we sold calls to enhance to yield.

MPL is likely to trades sideways and investors should use covered calls to enhance the yield. Excluding the added income from call options, MPL trades on an FY17 forward yield of 4.7%, assuming profit of $420m, EPS of $0.15 and DPS of $0.12.

Through adding a covered call we are delivering in excess of 10% cash flow (plus franking credit) and allowing for moderate capital growth.

Medibank (MPL.ASX) is now trading at a price level that warrants attention. The stock is forecast to pay a fully franked dividend in FY17 of $0.12, placing the stock on a forward yield of 4%+.

We don’t see too much in the way of earnings growth with forecast NPAT in FY17 being similar to FY16, in or around $430m on EPS of $0.16.

The stock is approaching an oversold level and may see a small bounce, otherwise we’re likely to see sideways consolidation at or $2.50 – $2.60 at which time longer term holders should sell covered calls.

For the trader, deeper selling from today’s price will provide an entry level with a likely bounce back to the above stated target range.

MPL.ASX NPAT $418m on EPS of $0.154 and final dividend of $0.065

FY17 outlook is for more of the same, growth will be difficult to achieve and revenue will remain flat, whilst net insurance margins will likely decline or remain flat at best. FY17 EPS $0.15 and DPS $0.12

Buy on a pullback into the $2.60 $2.75 range. Our algorithm engines will track for the entry alert.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453