The soft underlying revenue trends which impacted the other major bank results over the last week were obvious in CBA’s Q3 result. Offsetting the weak revenue trends in the major banks has been a strong performance on asset quality.

We see downside risks building around regulatory change & economic weakness leading to higher bad debts.

CBA FY18 forecasts net profit to remain flat at $9.8b, EPS $5.50, placing the stock on a forward yield of 4.9%.

The Algo Engine has triggered a buy signal on the higher low formation in ANZ. We’re happy to look at this from a very short term perspective but remain on the short side of the banks and we’re inclined to sell any technical bounce from the current levels.

NOTE: The Australian Government announced the introduction of the Bank levy in its 2017 budget. Based on the Treasury estimates this levy will raise $6.2billion which will reduce earnings by up to 5% for the majors’.

IPL reported 1H earnings of $152m, slightly ahead of market expectations.

IPL’s outlook was the most positive it has been in years. Although, global fertiliser prices have started to soften, with seasonal demand peak in April/May. US ammonia prices to are forecast to trade within the US$300/t to US$330/t. A weaker AUD offers a some upside to IPL’s earnings.

FY18 forecast revenue $4b, EBIT $640m, EPS $0.25, DPS $0.15, placing the stock on a forward yield of 3.7%.

Underlying earnings growth now tracking in the 10 – 20% range.

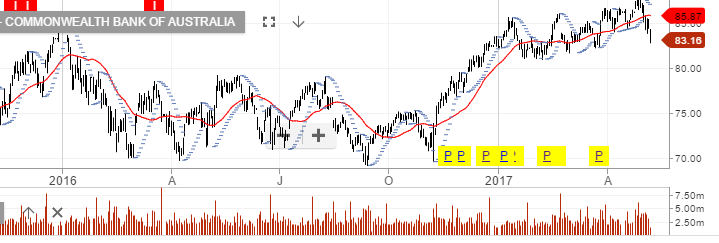

CBA, Australia’s largest bank, posted an un-audited Q3 profit of $2.4 billion for the three months ending march 31st.

This is up 4.3% from last year’s number of $2.3 billion. The level of bad debts rose to $6.7 billion compared to $6.3 billion a year ago. CBA shares opened over 2% lower at $83.30.

The ALGO engine gave buy signals on the 5 major banks during the last several months. Over the last several weeks, we have been suggesting that based on future growth prospects, the banking names were fully valued.

We will watch for ALGO buy signals over the near-term as the banking sector sell of extends lower.

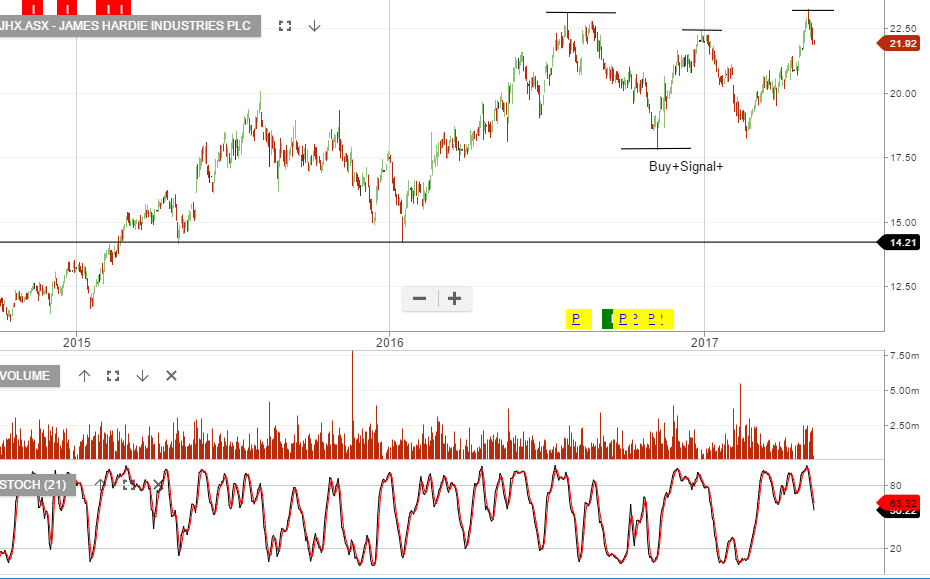

We forecast JHX FY17 NPAT of US$250m vs Management’s guidance of US$245-255.

On FY17 numbers JHX is looking expensive. FY17 EPS of $0.56 places the stock on a PE of 29x and a 2.4% yield.

Based on the current share price valuation, the market is looking for a 30% lift in underlying earnings into FY18, to support an EPS target of $0.72 and a reduction in the forward PE to 22x.

CSL’s FY17 NPAT guidance implies US$1.38b net profit after tax.

The company has purchased 1.4m shares during 2HFY17, of the $500 million share buy-back program.

With the stock price now trading 28x FY18 earnings, much of the good news is priced in. FY18 revenue $7.2b, EBIT $2.2b, forecast net profit up 20% to $1.7b, EPS US$3.60, DPS US$1.75 places the stock on a forward yield of 1.8%.

We remain attracted CSL and look for the next Algo Engine buy signal to provide a discounted entry point.