NASDAQ Top 30 ETF

China Large Cap

Austal

4D Medical

Price Movement: Shares surged as much as 38% in early trade, reaching a record high of $6.40.

The primary catalyst for today’s rally is the announcement that 4DMedical’s flagship CT:VQ™ technology has been deployed at the Mayo Clinic in the United States.

- Significance: Mayo Clinic is globally recognized as one of the world’s leading healthcare institutions. This partnership is viewed by the market as a “landmark moment” and a top-tier endorsement of 4DMedical’s respiratory imaging technology.

- Agreement Details: The clinic will integrate CT:VQ into clinical workflows for ventilation and perfusion analysis, allowing clinicians to evaluate the technology across multiple use cases.

### Market Reaction

Commercial Momentum: This marks the company’s sixth major U.S. deployment in just seven months since receiving FDA clearance in September 2025. Other major sites include the Cleveland Clinic, Stanford, UC San Diego Health, University of Chicago Medicine, and the University of Miami.

Watch Last Night’s Webinar

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

James Hardie

James Hardie Industries is under Algo Engine buy conditions.

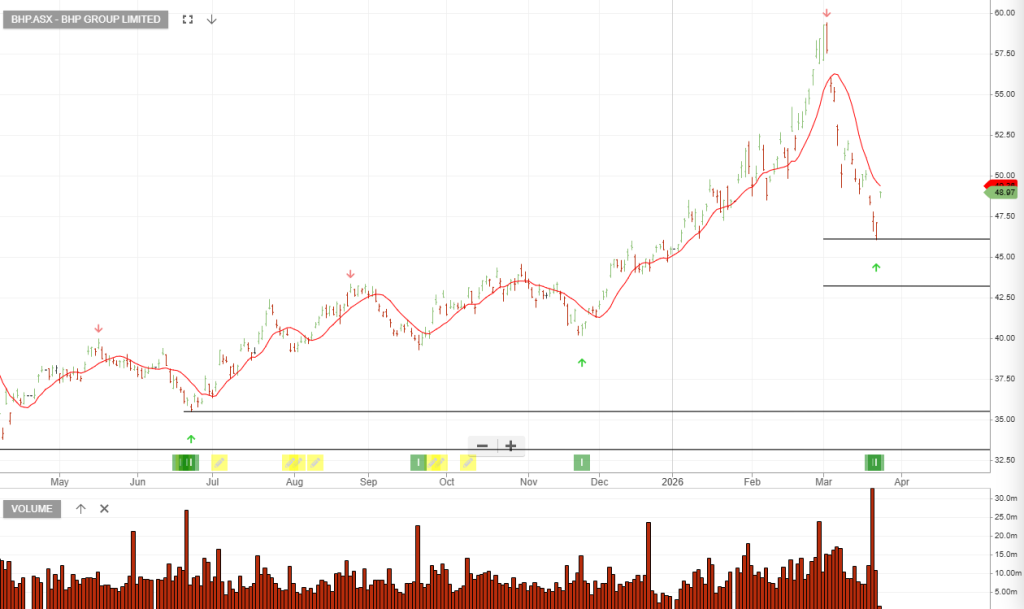

BHP

AS:BHP is under Algo Engine buy conditions.

Amcor

Amcor is under Algo Engine buy conditions.

Pax Gold

Pax Gold is under Algo Engine buy conditions.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453