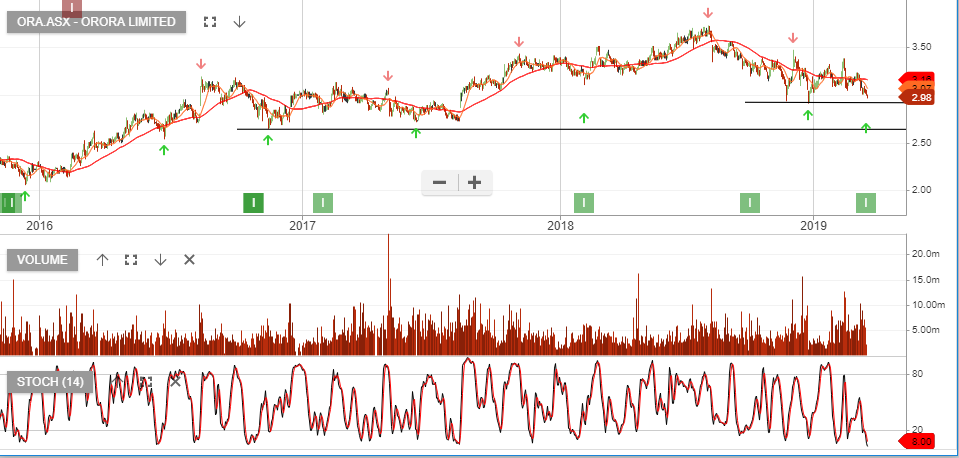

Orora – Buy Signal

Orora has formed a higher low at $3.00 and is now under Algo Engine buy conditions. The short-term indicators are still trending lower and suggest that $2.95 will provide an ideal entry level.

Orora has formed a higher low at $3.00 and is now under Algo Engine buy conditions. The short-term indicators are still trending lower and suggest that $2.95 will provide an ideal entry level.

Following the earnings miss in the February result, we feel Coles share price now reflects fair value. At 15x earnings and 5% yield there’s an opportunity to buy the stock and sell covered call options, to deliver 10% annualized cash flow.

We question the earnings outlook next year, mainly due to increased capital spending requirements. However, for the balance of 2019 we expect the share price to remain within the $11 to $11.75 price range.

For more detail on the derivative strategy, please call our office on 1300 614 002.

The S&P/ASX 100 is nearing a break of the upward trending 10 day moving average. We’re using this as a reference for the shorter term momentum to align with the broader index sell signal.

Since writing the above post we are now seeing the XJO trade below the 10 day average.

Caltex Australia is under Algo Engine sell conditions and was removed from the model portfolio late last year at $28.50.

Fuel retail margin was A$35-45mn lower at end-February, (based on the same time last year), driven by diesel pricing and gasoline retail competition. The company will provide a Q1 trading update at its AGM on 9 May 2019.

In FY20 we assume $25.5b in revenue and 4% increase in EBIT to $1.07b which flows through to $1.25 in dividends, placing the stock on a 4.5% forward yield.

For investors who are not taking up the buy back offer, we recommend selling a covered call option to enhance the income return.

For more detail, please call our office on 1300 614 002.

InvoCare is under current Algo Engine sell conditions, following a recent lower high formation at $15.00.

Invocare’s balance sheet will be strengthened following the announced raising of up to A$85m, via institutional placement which will include $20m via a share purchase plan. We expect this to be done at around $13.30.

We anticipate the next signal to be a Algo Engine “buy” and we’re likely to see this before the end of April.

We see long-term value in IVC and suggest investors watch for an entry signal between $13.30 & $13.80

Crown Resorts is under Algo Engine buy conditions and is a current holding in the ASX 100 model portfolio.

We see technical price support at $11.50 to $11.80. We suggest buying the stock for the upcoming dividend on the 20th of March and adding a Euro call option to boost the cash flow return.

For more detail on this strategy, please call our office on 1300 614 002.

Aristocrat Leisure is under Algo sell conditions following the lower high formation at $26. This is a favourite amongst local fund managers, with analyst price targets as high as $40.

The recent selloff has seen the PE fall from 30x back to a 17x PE. With the share price at $23, buying interest is now building and we may see a counter trend rally extend through to $24.50.

Woolworths Group is a current holding in our ASX 100 model portfolio, as well as the ASX 20 & 50 models.

The stock is up over 9% including dividends after being added at $28.50 back in August last year. With the share price trading at 24x forward earnings and only a 3% dividend yield, we consider it expensive.

We suggest selling a long dated European call option to enhance the income. For more detail on the strategy, please call our office on 1300 614 002.

Amcor has released the scheme booklet for its all-stock acquisition of Bemis with the transaction unanimously recommended by the Boards of both companies.

The Bemis transaction is expected to be completed on 15 May 2019.

AMC reported a solid 1H19 result in February and forecast underlying EPS growth of 3 – 4% supported by US$180m in cost synergies to be realized from the merger over the next 3 years.

Amcor trades on a 4.5% forward yield. In FY20 we expect the combined revenue to exceed US$14b and EBIT to increase to US$1.7b.

We remain buyers at or near $14.50.

Seek is a current holding in our ASX 100 model portfolio. The stock goes ex-div $0.24 on the 25th of March and adding a covered call option will boost the annualized cash flow to 10%+.

Seek delivered recent earnings slightly ahead of market consensus and we consider the stock an attractive income contributor to client portfolios.

For more detail on the covered call strategy, please call our office on 1300 614 002.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453