Buy CIMIC & Sell Call Options

CIMIC is a current holding in the ASX 100 model portfolio. We originally recommend accumulating the stock at $42.50, back in November.

Chart from 26th Nov…

Updated chart as at 24th Jan

CIMIC is a current holding in the ASX 100 model portfolio. We originally recommend accumulating the stock at $42.50, back in November.

Chart from 26th Nov…

Updated chart as at 24th Jan

Our Algo Engine has a sell signal on the XJO and we also draw your attention to the sell signals in the large cap miners, BHP & RIO.

The lower high formations and subsequent sell signals occurred in these two names, well ahead of the sell signal on the index.

The charts below show selling pressure has gathered momentum, following flat production guidance and lower price realisation in 2019.

BHP

RIO

Ansell is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

ANN made a higher low formation at $22 and we see the potential for the stock to trade higher based on supportive macroeconomic data and moderation of raw material prices.

At 15x forward earnings and 3.2% dividend yield, the valuation is below historical averages. 2019 EPS growth should be around 6 – 8%.

Our Algo Engine triggered a “sell” signal in Webjet on Monday and after taking a closer look at the financials, there’s reason to add this one to your watch list.

It appears the market is now starting to factor in a meaningful deceleration in the revenue & earnings trajectory. Original expectations were for Webjet to continue growing revenue at 13 – 17% but headwinds in 2019 and 2020, make this unlikely.

With the stock trading 32x FY18 and 25x 2019, we see little room for disappointment in upcoming earnings and future guidance.

Run a stop-loss above $12.50 and watch the short-term momentum indicators.

InfraCo is still a key part of Telstra’s business strategy and they’re making major investments in infrastructure.

Telstra will upgrade its huge network of submarine cables. The overhaul will increase the capacity of the lines and allow Telstra to carry half as much data again, as they do now. Helping to secure Telstra’s position as the largest network of subsea cables in the Asia Pacific region.

High quality subsea cables are essential because they link Telstra Australia to the rest of the world.

In recent years Telstra has been making “lower lows & lower highs”, reflected in the Algo Engine sell conditions. We feel 2019 will produce the first “buy signal” in over 2 years.

TAH reports their 1H19 result Wed 13 Feb. With stock now under Algo Engine sell conditions, we’ve taken a more cautious positioning ahead of the earnings release.

The stock looks fair value at 12x FY19 and 11x FY20 earnings. FY20 EPS growth of 8% places TAH on a forward yield of 4.6%

FY20 revenue $5.5bn and EBITDA $1.14mn.

Technical resistance between $4.70 and $4.90.

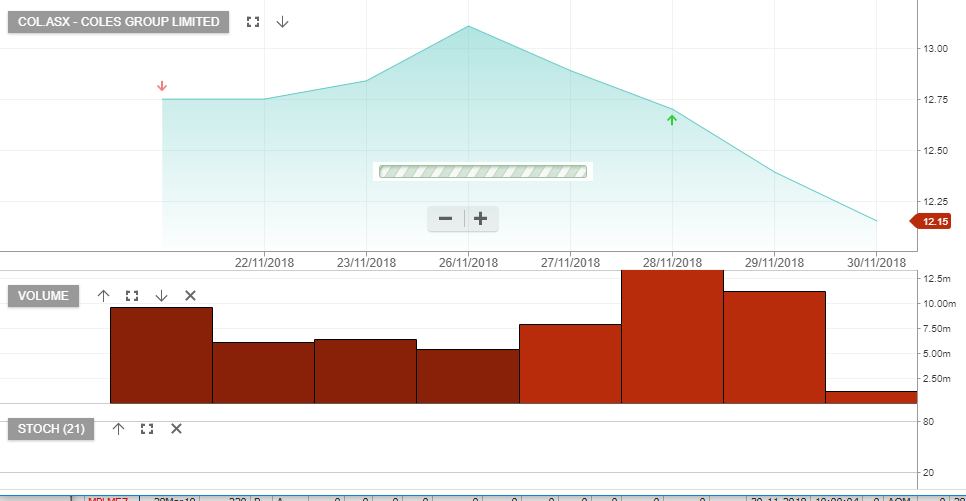

Coles has under invested in the supply chain and online platform vs Woolworths and therefore, investors need to be prepared for lower returns as Coles steps up capital expenditure over the coming years.

If we assume 3 – 5% EPS growth, (half that of WOW), Coles will offer a 5.4% dividend yield into FY20, based on earnings per share of $0.80

Coles trades on 18x FY19 earnings and with little upside to the share price, we recommend investors add a covered call to enhance the income return.

We consider the 2019 recovery rally in the below names, as now largely complete.

The post below is from the 14th of November.

GARP is an acronym which is referenced to “growth at a reasonable price”.

This is how we now view ALL, TWE, CAR and SEK.

Downer EDI has now moved into our “sell” target range of $7.20 to $7.50. After buying DOW at lower levels we recommend investors look to lock-in the gains.

S32 reported their Dec quarter production numbers which came in above market consensus. The strong numbers increase the likelihood of capital return to shareholders, later this year.

We have S32 trading on 5% forward yield with relatively flat EPS growth.

We note the current Algo Engine sell signals across most resource names, (excluding the energy complex).

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453