Buy Crown – Value Emerging

Crown is likely to find buying support within the $13 – $13.50 price range.

As such, we recommend investors accumulate the stock and look to sell a covered call option to enhance the yield.

Crown Resorts

Crown is likely to find buying support within the $13 – $13.50 price range.

As such, we recommend investors accumulate the stock and look to sell a covered call option to enhance the yield.

Crown Resorts

Healthscope has retested the $2.07 price gap and has seen strong buying support.

We see HSO as a good long-term value play with improving earnings over the next 2 – 5 years.

Healthscope

Ansell has found short-term support at $24.70 during yesterday’s trade.

However, with the USD weakening overnight, we’re “on watch” for a break of this level.

We see a good buying opportunity, should the stock trade down to $23.50.

Keep ANN on your watch list.

Ansell

After reaching a high of $1370.00 in mid-April, the price of gold dropped over $200.00 and traded as low as $1160.00 on August 16th.

By many technical measures, the 4-month correction in the yellow metal looks to have run its course.

Increased trade tensions, EM currency weakness and Geo-political risks are all fundamental elements which support higher prices for Gold.

The next point of resistance is near $1214.00, with solid support at $1185.00

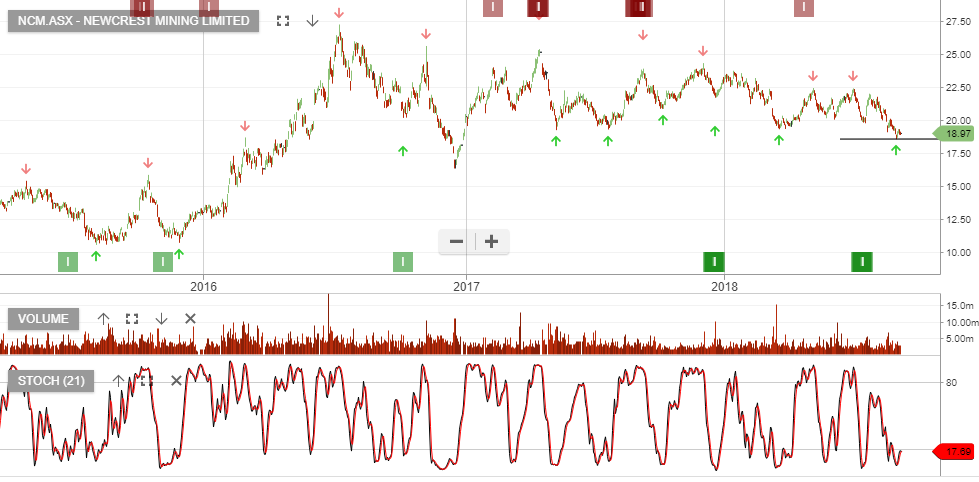

Our preference within the gold miners is NCM, followed by EVN.

Since posting a high of $3.30 on August 20th, shares of MPL have dropped over 12% and posted a low of $2.87 in early trade today.

Internal momentum indicators are now reflecting and oversold condition on the daily charts.

We recommend accumulating MPL in the 2.75 – $2.90 range.

MediBank Private

Insurance Australia Group, (IAG) is retracing into a price zone that provides a discounted entry point to begin accumulating the stock.

We see a cluster of support dating back to December of last year on the daily charts and good value between $7.00 and $7.30

IAG

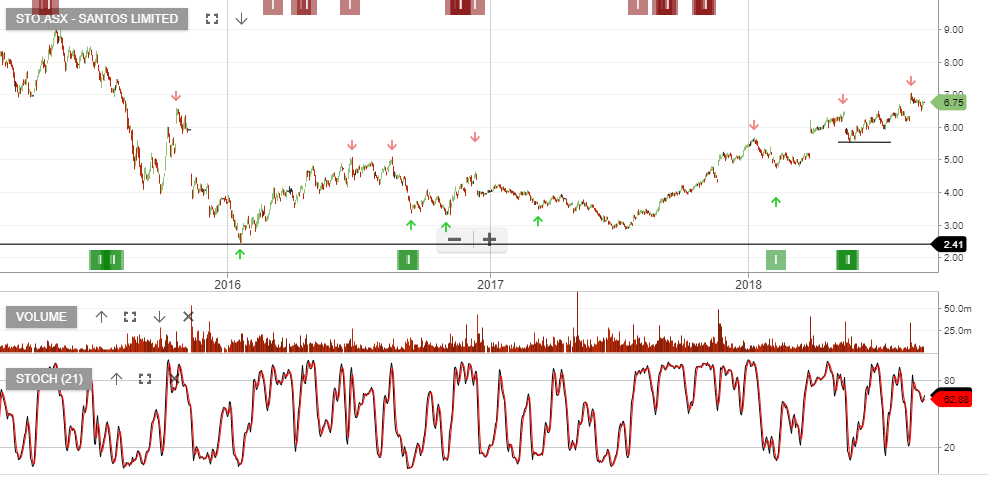

Shares of STO have firmed over the last week as investors see the company’s recent acquisition of Quadrant Energy as a net positive to growth.

The addition of Quadrant will increase STO’s ownership of high-grade gas assets in Western Australia.

In addition, the Quadrant fields will strengthen STO’s operating capacity and increase last year’s rise in underlying profit into FY19.

We see initial chart resistance in the $7.35 area.

Santos

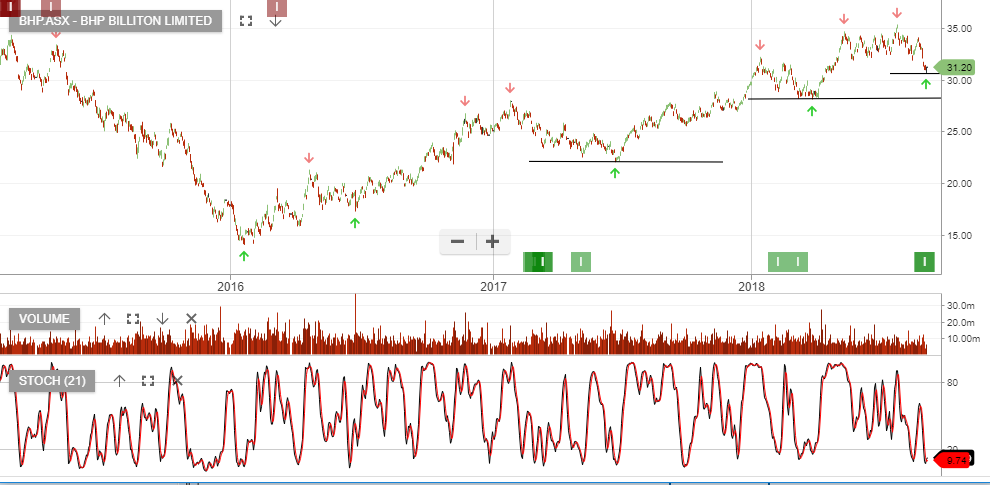

Our Algo Engine generated a buy signal in BHP following the recent “higher low” chart formation.

We see value in the $30 – $31 range and suggest accumulating BHP with a view towards selling covered call options to enhance the overall investment return.–

BHP

We currently hold Crown Resorts in our ASX top 100 model portfolio, following a Algo Engine buy signal back in February at $12.50.

The stock has recently retraced from the $14.59 high made on the 10th August.

We now feel the sub-$13.50 level provides an opportunity to accumulate Crown shares at a fair valuation.

NOTE: Star Entertainment is also back in the buy zone between $5.13 – $5.30

Crown

We recommend accumulating Origin Energy shares at $7.70.

Origin

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453