Link Administration Is Approaching Oversold Levels

Link Administration has been sold off following the Federal Budget measures aimed at increasing consolidation of inactive super accounts.

Although the announcement now creates a headwind for Link from FY20, we consider the stock “oversold”.

We suggest investors can accumulate Link at or near $7.00 support.

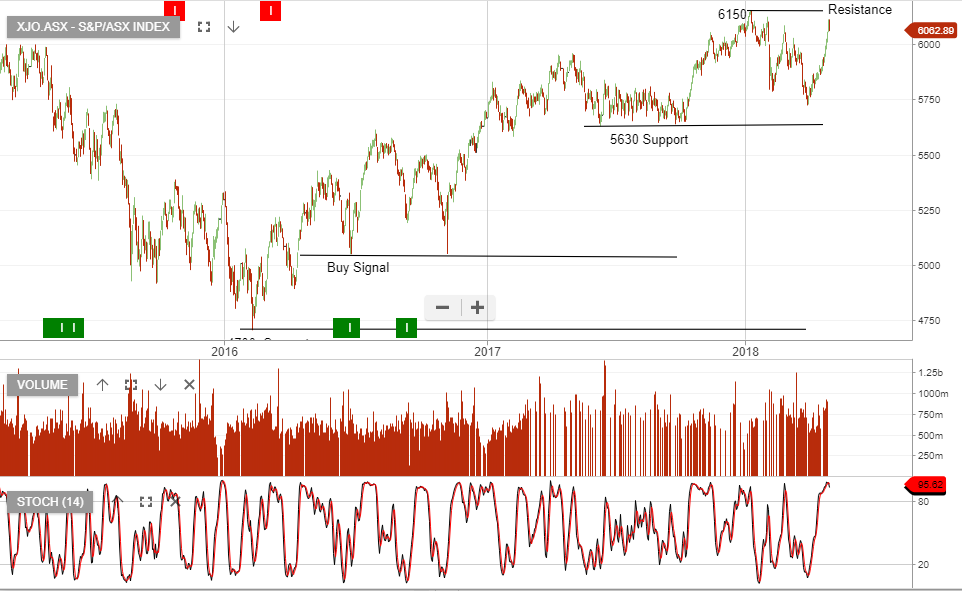

Link

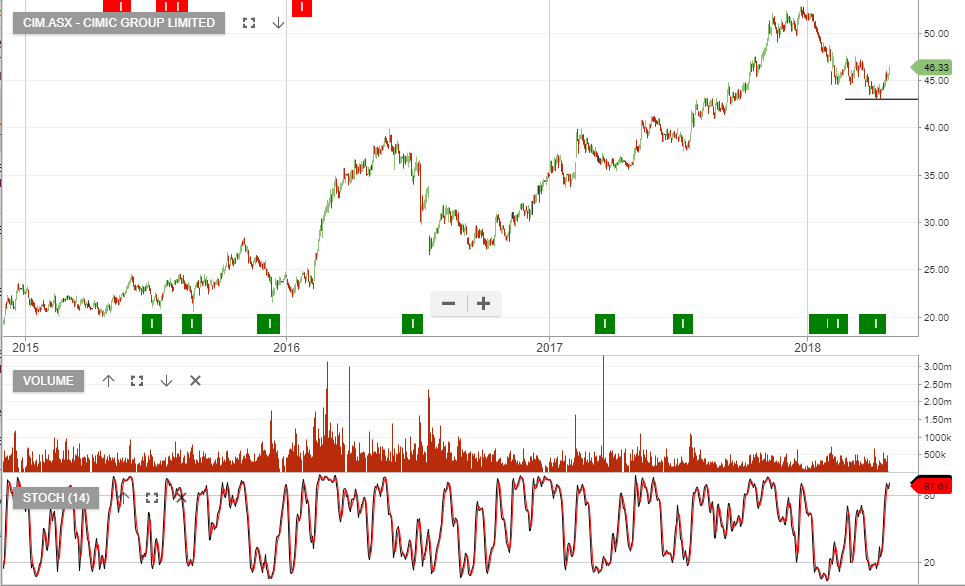

CIM

CIM