Short Orica

We recommend the short side of Orica heading into 2H18 earnings announcement on 7th May.

The market is looking for significantly stronger 2H performance and is likely to be disappointed. Orica is trading on stretched valuations and offers a 2.6% forward yield.

Look to sell within the range displayed below.

Orica

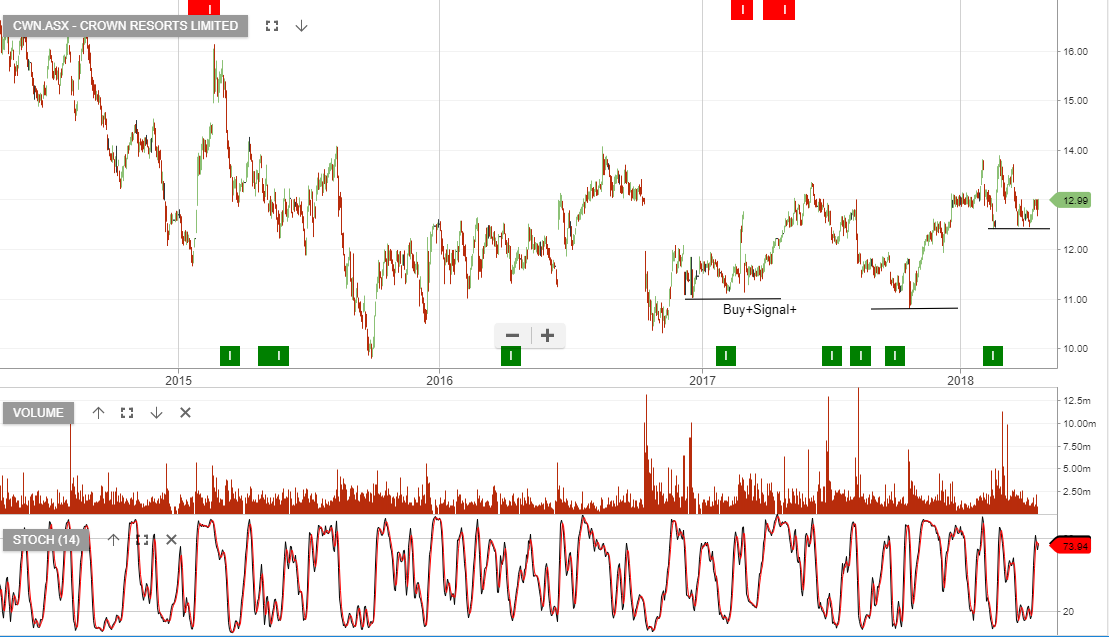

Buy Crown Resorts

Buy Crown Resorts