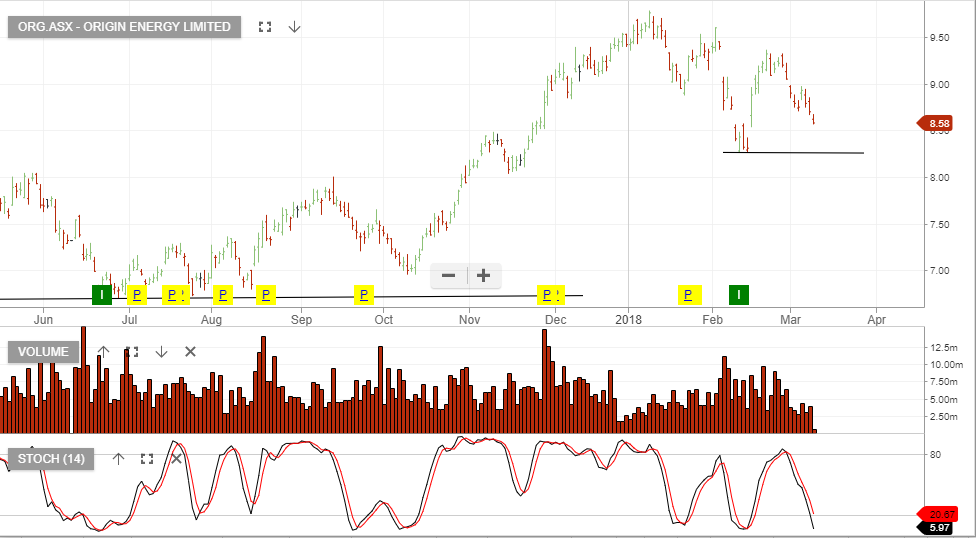

Buy – Origin Energy

We recommend buying ORG Energy when the short-term indicators turn positive. We expect the entry level will be confirmed early next week.

Keep this one on your watch list.

Origin

We recommend buying ORG Energy when the short-term indicators turn positive. We expect the entry level will be confirmed early next week.

Keep this one on your watch list.

Origin

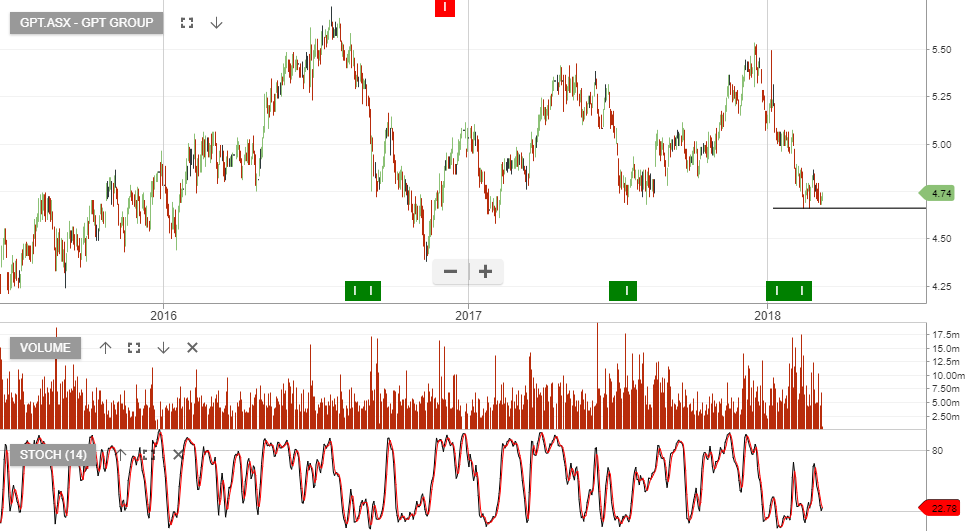

We recommend buying GPT Group and placing a stop loss below the recent $4.65 low.

Investors may prefer to hold the stock and sell September $5.00 call options to enhance the cash flow, whilst staying exposed to the June dividend.

GPT will pay $0.123 dividend on June 29th.

Invocare has under performed following their recent earnings report, in which the company indicated flat forward earnings and an increase in capital expenditure.

Technically, a “higher low” formation remains in place and we flag to our readers the strength in today’s price action.

IVC

We recommend buying Transurban Group and selling covered call options to enhance the income.

TCL will pay a $0.27 dividend on June 29th.

TCL

We recommend buying Star Entertainment and placing a stop loss below the recent $5.19 low.

SGR will pay $0.085 dividend on August 28th.

We recommend buying Sydney Airports and placing a stop loss below the recent $6.30 low.

SYD will pay $0.165 dividend on June 29th.

We recommend buying Amcor and placing a stop loss below the recent $13.90 low.

AMC will pay $0.30 dividend on September 4th.

The video runs for 5 minutes and if you’d like to discuss the ideas presented, please call our office on 1300 614 002.

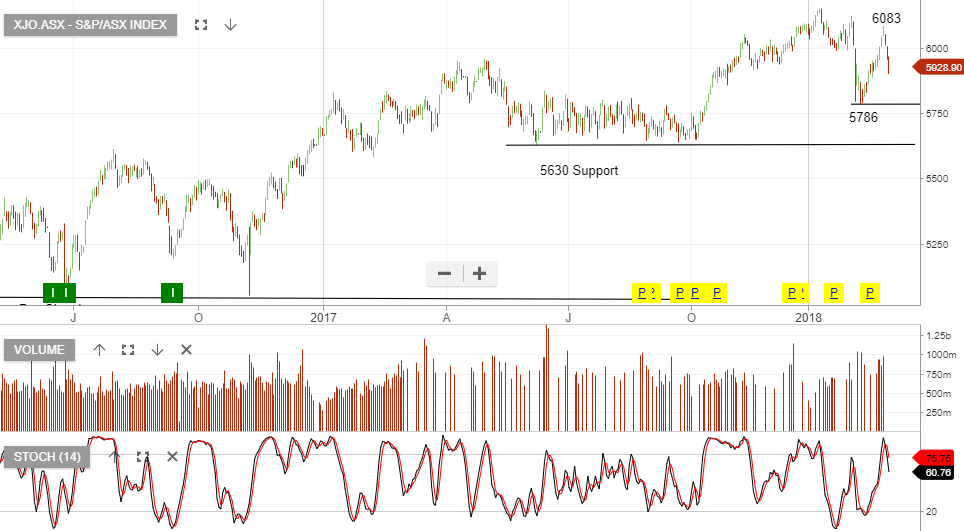

The S&P/ASX 200 Index finished the week down 1.2%.

The best performer was the Property Trust sector, up 0.3% and the worst performer was the Telecoms sector, down 4.8%.

The market found resistance at 6083, the top end of the range we forecast.

SGR was recently triggered as an Algo Engine buy signal and we now look to accumulate the stock within the value range marked on the chart below.

Star Group

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453