WOW – Algo Update

We feel Woolworths provides further upside potential heading into tomorrow’s quarterly trading update.

Price target $27.00

We feel Woolworths provides further upside potential heading into tomorrow’s quarterly trading update.

Price target $27.00

We’ve been buyers of WPL and ORG following the recent Algo Engine buy signals.

We forecast $400+ million in reported profit for FY17, up from $350 million in FY16.

Global fertilizer prices continue to push higher and an improved demand/supply situation is helping to sustain the rally in IPL’s share price.

The stock is now close to full value and has rallied 20% since the Algo Engine buy signal back in July at $3.25.

IPL reports earnings on Tuesday the 14th of November.

IPL

SGR has delivered a solid start to FY18. Completion of the upgrade project at Sydney and Gold Coast resorts will be finished in early 2018, helping to drive earnings momentum through 2020.

We forecast FY18 EPS growth of +12%+, underlying EPS $0.29 and DPS $0.16 placing the stock on a forward yield of 3%.

SGR is likely to provide a number of trading opportunities. We see the current rally exhausting within the $5.70 to $6.00 range. We recommend taking profit within this range and waiting for a pullback to $5.50.

Longer-term holders may prefer to sell covered call options at or near $6.00 and hold the stock through to June 2018.

Star Group

Oil prices are likely to remain well supported as OPEC said to work on exit strategy alongside supply cut extension.

Our Algo engine generated a buy signal in WPL back in June and we now see support building near the $28.00 price point.

Investors can add long exposure here in WPL with stops below $28.00.

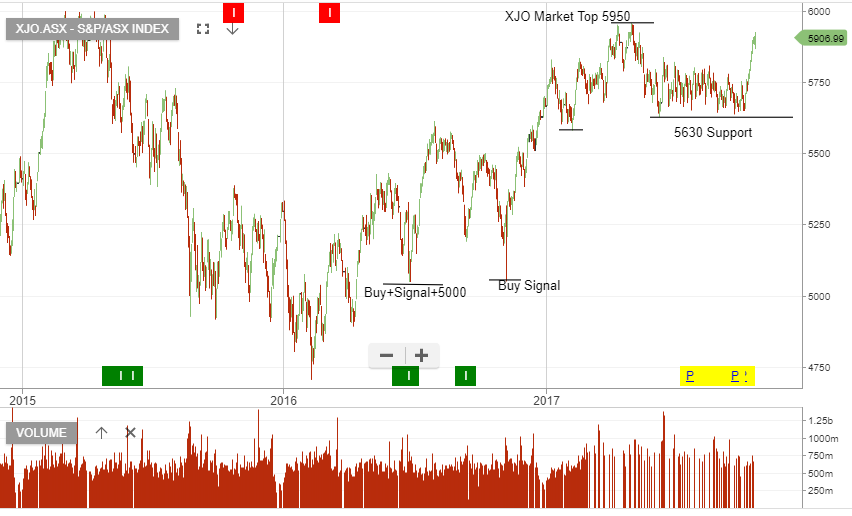

The S&P/ASX 200 Index finished the week to Friday up 1.6%, the best performing sector was the Utilities sector, up 3.9%. AGL Energy Ltd led the performance rising by 5.0% and the worst performing sector was the Telecoms sector, up only 0.7%.

The XJO index found support at 5640 early this month and has since rallied to the top end of the trading range, making a high in Friday’s session of 5925.

We last had an Algo Engine short signal in NCM around the 5th of September when the stock was trading at $23.85. Since then, NCM has sold-off over $2.00 and the chart below shows the lower high pattern and the need for the price action to trade back through $22.75 to establish a change in trend.

BXB’s 1Q18 sales trading update was slightly better than market expectations with robust 6% constant currency revenue growth for the first quarter.

Underlying FY18 earnings will likely grow at 5 – 6% and increase to $1bn.

On the back of increase to earnings, our target price range for BXB is $9.25 support and $10.00 resistance. BXB is a strong business with dominant global market positions, we’re comfortable running a buy write strategy on BXB.

FY18 forecast dividend yield is 4%, we allow for moderate capital growth and cap the gains with a covered call option to boost the annual cash flow to 10%+.

Brambles

Wesfarmers reports 1Q FY18 sales on 25th of October and industry feedback suggests that Coles is not executing as well as it was and is losing market share back to Woolworths.

We expect 10% growth from Bunnings and Coles to deliver flat or low single digit growth.

FY18 forecast revenue is $70b, EBIT $4.3b with net profit after tax of $3 billion.

EPS $2.60 and DPS of $2.35 places the stock on a forward yield of 5.5%. We see relatively flat earnings for the conglomerate over the next 2 – 3 years.

Buying WES and selling an at the money European call option will provide investors with access to the dividend, franking credits and an additional 6% per year of income, on top of the 5.5% dividend yield.

Wesfarmers

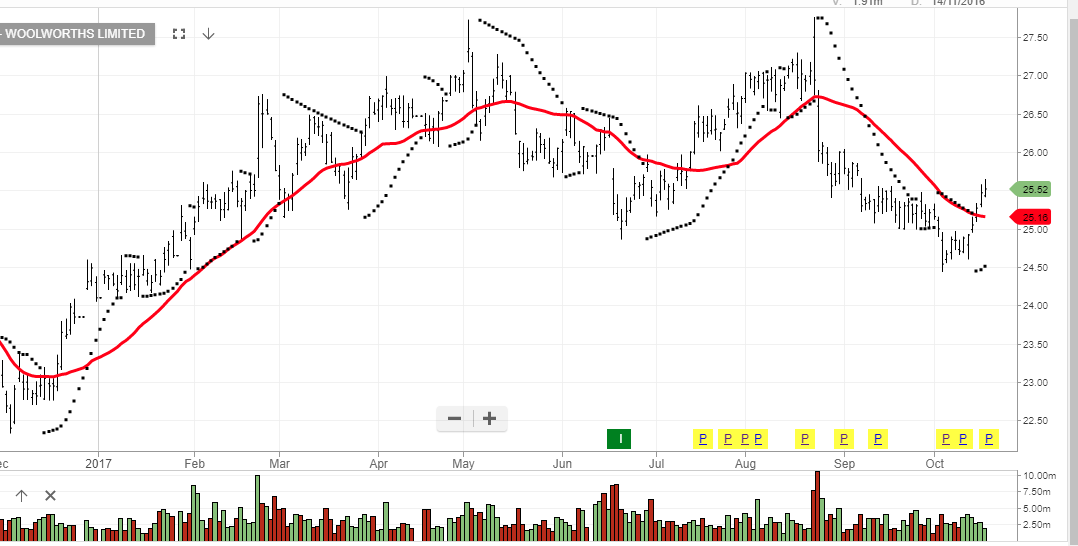

Woolworths will report their first quarter sales for FY18 on the 31st of October. We expect continued growth of around 5% from the key Food and Liquor business, while Big W is likely to struggle.

FY18 total revenue if forecast to be $58b, EBIT, $2.5b delivering underlying net profit of $1.6b.

EPS $1.35 and DPS of $1.00, places the stock on a forward yield of 3.5%.

Our Algo Engine generated a buy signal in Woolworths near $25, we see this as fair value and when complimented with a covered call, we’re delivering 10 – 12% per annum in cash flow ASX:WOW

Woolworths

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453