Woolworths announced FY17 underlying NPAT of $1.42 billion, down 3.6% and the company declared a final dividend of 50 cents, which includes the one-off item from the sale of Masters. The higher dividend is not likely to recur in FY18.

The market is now looking for WOW to grow NPAT in the range of 5 – 8% and payout approximately $0.90 in full year distributions, placing the stock on 22x forward earnings and 3.1% dividend yield.

We feel WOW is now fully valued and holding the stock can only be justified when an at-the-money covered call is overlaid to boost the annualised cash flow to 10 – 12%.

Coca Cola announced 1H17 underlying NPAT fell 4.3%, to $190 million. The company declared an interim dividend of 21 cents, which is 75% franked.

Forward guidance suggest relatively flat EPS will continue with full year NPAT expected to be $420 million.

Indonesia and PNG are delivering improved earnings metrics and we have the company on a forward dividend yield of 5.4%, assuming 44 cents in annualised DPS.

AMC has delivered FY17 operating earnings of $1.09 billion, up 3% on FY16. The Board declared a final dividend of $0.235.

Underlying net profit for the 12 months to June, came in at $700 million or 4.5% higher on the same time last year.

At 19x forward earnings, AMC is expensive.

However, earnings are defensive and the company should still achieve average EPS growth of 8% into FY18, (net profit in the range of $750 – $770 million), placing the stock of a forward yield of 3.7%.

We expect AMC to trade within a range of $15.00 to $16.50.

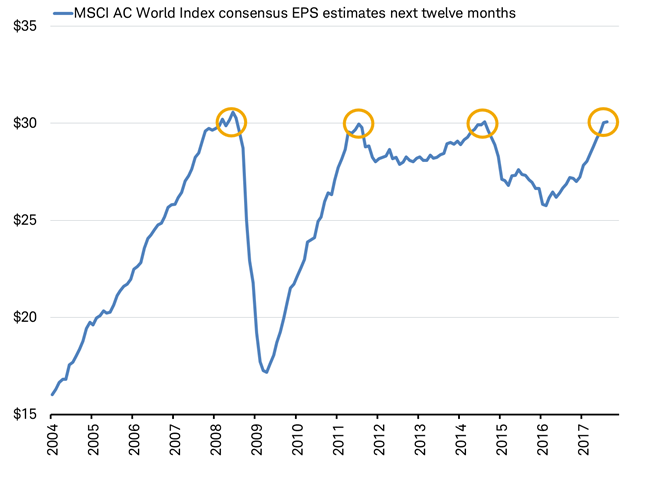

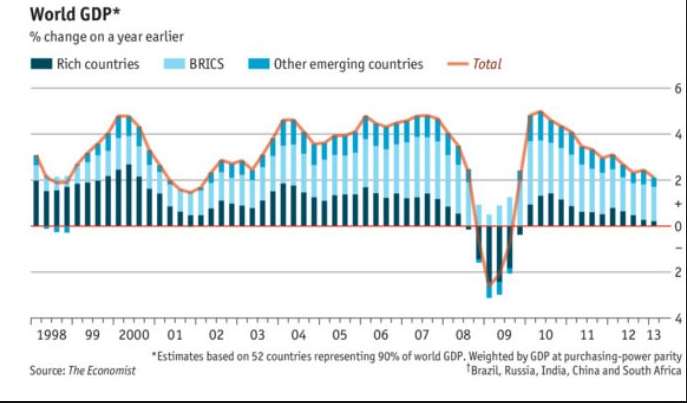

Global equity market price-to-earnings ratio are now trading at a 15 year high and average earnings per share sit at prior peak levels.

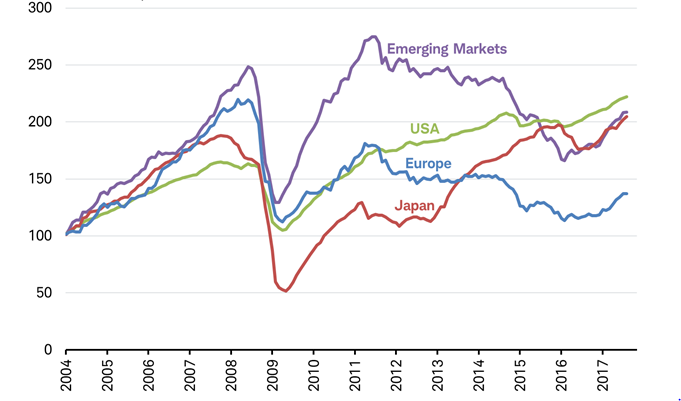

The World Bank forecasts that global growth will strengthen to 2.7 % in 2017 amid a pickup in manufacturing and trade, rising confidence, favorable global financing conditions, and stabilizing commodity prices.

Growth in advanced economies is expected to accelerate to 1.9 % in 2017, a benefit to their trading partners. Growth in emerging market and developing economies will recover to 4.1 % this year, as obstacles to activity diminish in commodity-exporting countries.

Source: Charles Schwab, Factset Data as of 8/17/2017

Looking at the graph below, investors can see the difficulty the global economy has had in maintaining GDP growth.

We consider this an interesting contradiction to record PE valuations and EPS growth. For the most part, this is best explained through understanding the impact of share buy-back programs, helping to deliver financially engineered EPS growth.

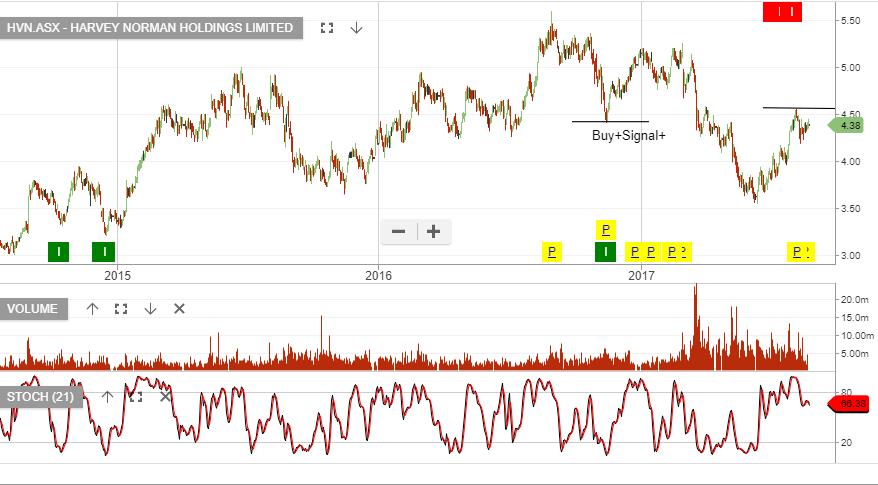

As the Algo Engine identified the “higher low” price pattern in both Woolworths and Origin Energy, we’ve regularly highlighted these as preferred buying opportunities.

We’ve remained buyers of ORG and WOW throughout the past 12 months but now feel that we’re approaching a level where we see full value.

Resistance in ORG will likely be found at or near $8.00 and WOW is likely to experience selling based on valuation grounds at or near $27.50.

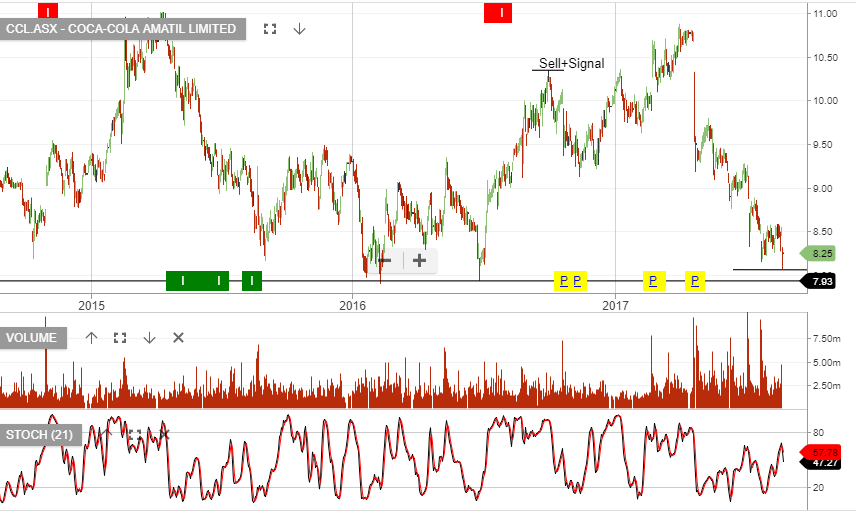

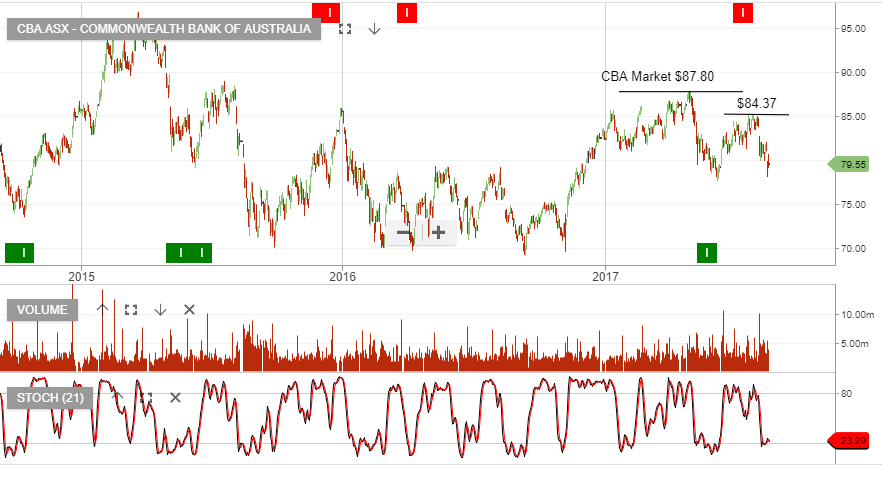

Our Algo Engine flagged the negative technical structure in leading financials firms Commonwealth Bank and Goldman Sachs. These are both leading industry names which have bearish price action developing.

Investors should remain on the short side of these assets.

The charts below illustrate the recent Algo Short signals along with the resistance or selling pressure, which is now building.

Chart – CBAChart – GS

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.