Algo Update – Caltex

We continue to hold Caltex in our model portfolio with an upside target of $33.00.

We continue to hold Caltex in our model portfolio with an upside target of $33.00.

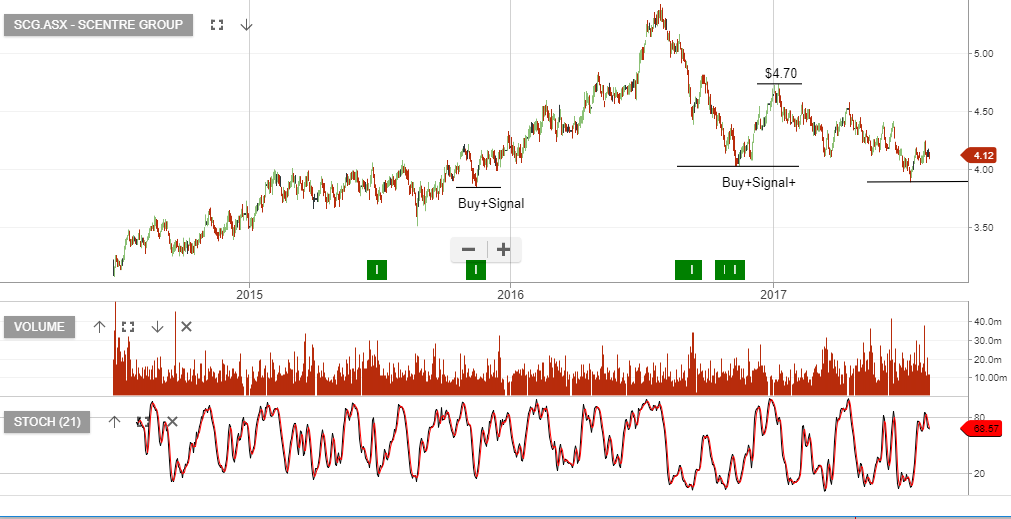

Scentre Group announced their estimated distribution for the six month period ended 30 June 2017 will be $0. 10 cents per ordinary stapled security.

Scentre Group will announce its results for the half year ended 30 June 2017 on Thursday, 24 August 2017.

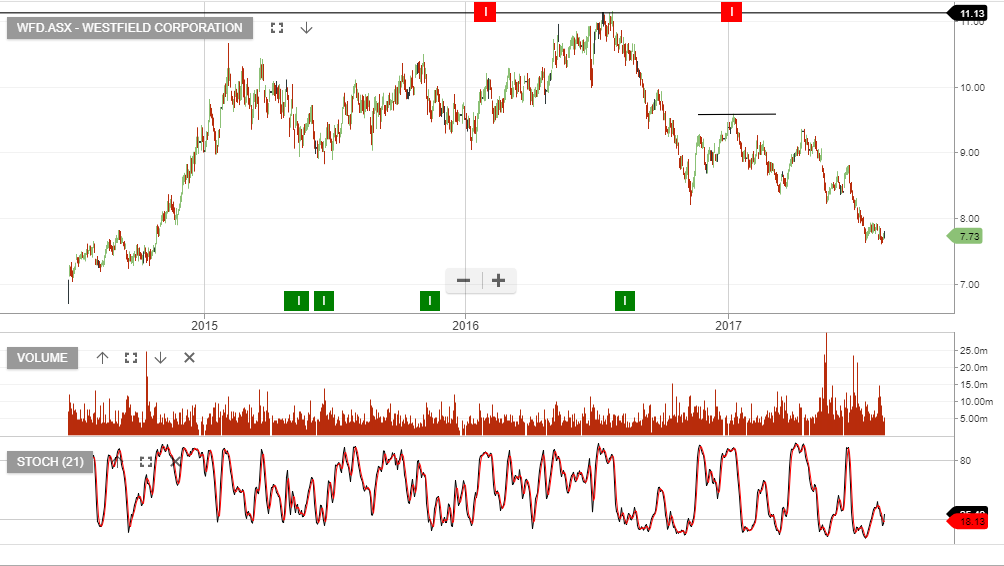

The chart of Westfield below illustrates the price action is now in an oversold range.

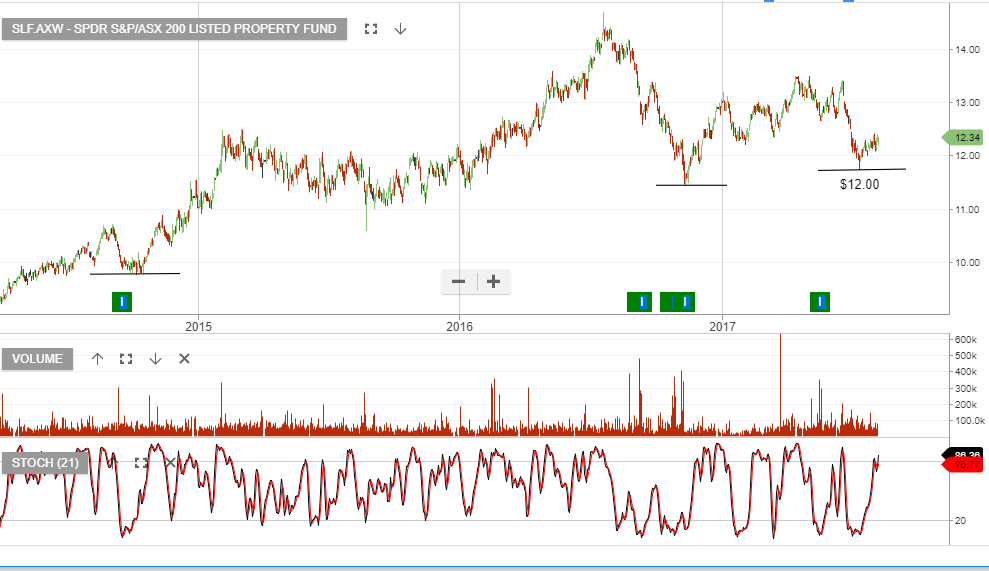

Our Algo Engine triggered a buy signal in the SPDR Property Fund ETF.

Our Algo Engine triggered a buy signal on Invocare and it now appears that the stock is finding buying support. The share price is pivoting higher after making a low at $13.60 on August 3rd.

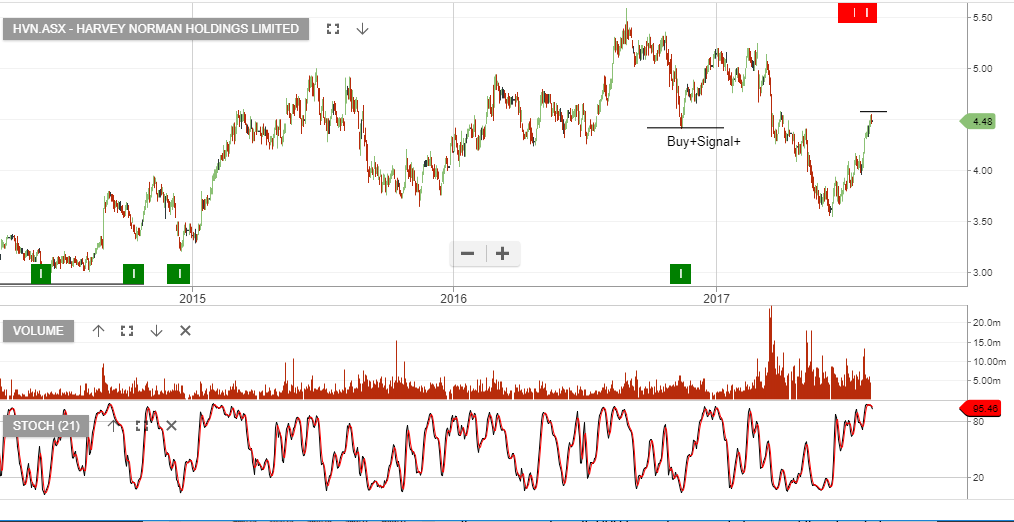

The technical pattern for Harvey Norman started to break-down early this year when the price action traded through the $4.50 support level.

Since then, HVN made a low in June at $3.55 and has now had a counter-trend rally back to $4.50.

Our Algo Engine is now flagging the “lower high” structure and we’ve added HVN to the short trade list with a stop loss above the $4.75 area.

Short term traders may prefer to use the momentum indicators to compliment the entry and stop loss rule.

HVN reports on the the 31st August. The market is looking for NPAT to increase to $377m, (from $337m last year), and DPS up 1 cent to $0.18.

Overly optimistic property revaluations, along with weak consumer trends, concern us and support our bearish view.

Following the recent Algo Engine buy signal, Sonic Healthcare looks like it is finding support at or near $22.50.

We continue to like RMD, SHL, CSL, MPL & RHC in the healthcare sector.

Both SYD and TCL are core investor holdings where we’ve applied “buy-write” strategies to enhance the cash flow. A combination of the December dividend and the call option income is generating 10 – 12% annualised cash flow.

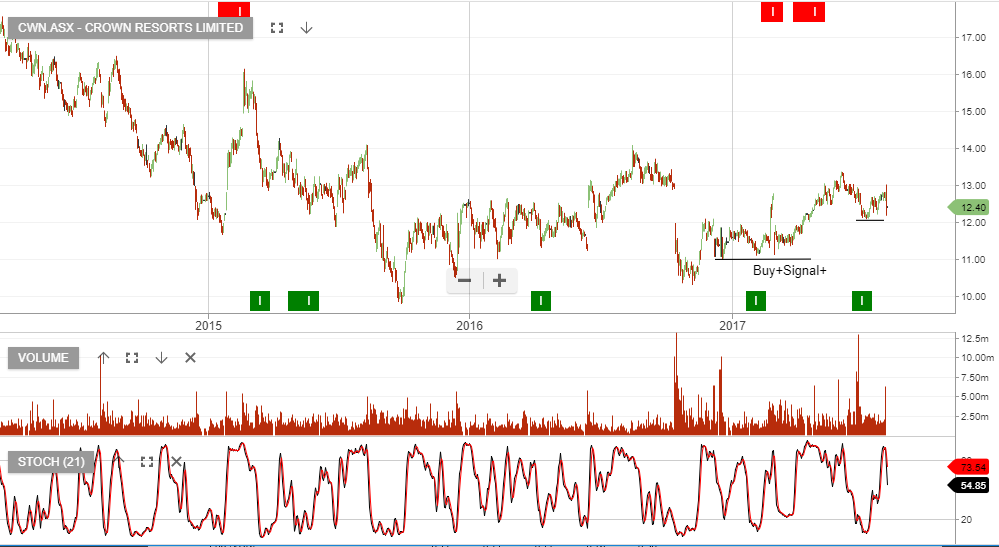

Crown Resorts reported their FY17 earnings on Friday, and the result showed a 13% decline in revenue and 11% fall in EBITDA. Helping to offset this was a further $375m share buyback.

Based on $0.60 of DPS in FY18, Crown trades on a forward yield of 4.8%.

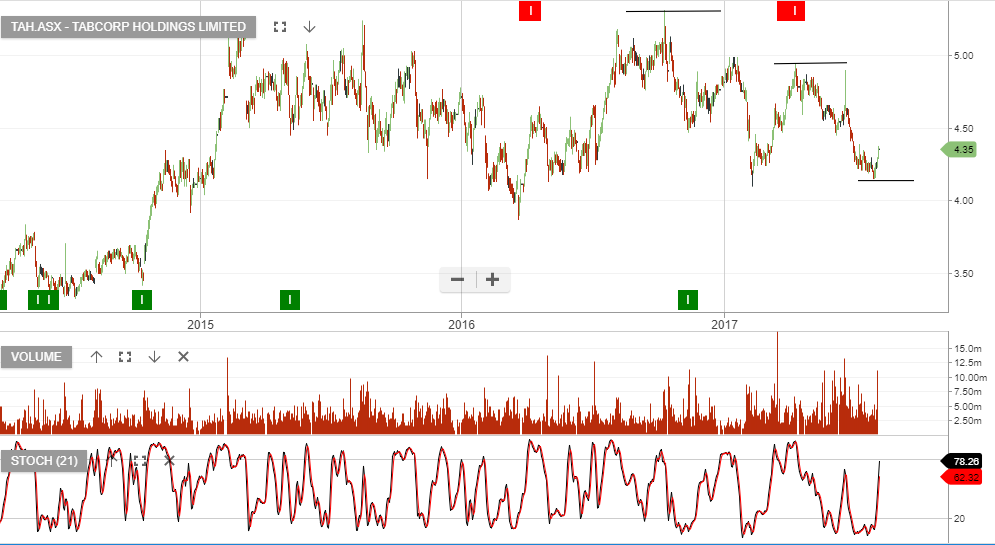

TabCorp Holdings reported FY17 earnings on Friday with underlying net profit of $179m, down 4% on the same time last year. We see encouraging trends within the core wagering business with digital turnover up 14% and fixed odds revenue growth of 15%.

We expect the Tatts merger to be completed by the end of the year and with the FY18 dividend yield at 6%, we see upside potential to $4.50 – $5.00.

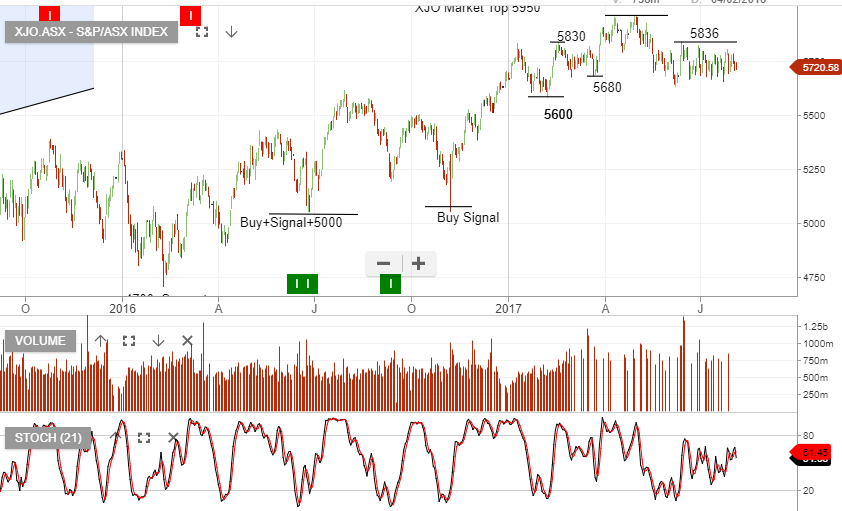

The S&P/ASX 200 Index finished the week up 0.31%

The best performer was the Utilities sector, up 3.6% and the worst performer was the Financials ex-Property sector, down 1.1%.

The XJO remains in a “lower high” pattern, as illustrated on the chart below.

On June 29th, when CBA was trading at $84, our Algo Engine generated a sell signal, as CBA formed a “lower high” structure.

Since then, selling pressure has gradually increased with the $84 to $85 range forming the resistance of the bearish pattern.

Our Algo Engine has been alerting us to the retracement and “higher low” pattern developing in GrainCorp.

The stock price bounced from oversold conditions in Thursday’s trading, after touching $8.51. Friday displayed strong follow through buying with the price action closing near session highs.

We’ve been looking for a move higher in GNC, it looks like it could be underway, and a rally back to $9.25 – $9.50 is our target.

Apply a stop loss below $8.51.

Invocare is another name we’re watching for confirmation on a developing “higher low” pattern. Friday’s closing price was a little weak. We’ll watch this name into next week and keep you updated on our analysis.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453