Our Algo Engine recently triggered a buy signal in IPL. With the stock price now beginning to see buying interest at or near $3.20, (as the “higher low” formation develops), we recommend investors continue to hold the long exposure.

Suncorp announced earnings for FY17 which resulted in a sharp drop in the share price during yesterday’s session.

The group delivered NPAT of $1,075m up 3.6% on the same time last year. Suncorp also announced a final dividend of $0.40 taking the full year dividend to $0.73.

We’ve been warning about Suncorp in the monthly ASX 50 video reports and exited all Suncorp holdings 8 weeks back at $14.50 per share. We remain cautious, as downside risks are increasing from higher costs and increased risk of higher BDD charges in the bank.

The previous point is not a unique issue to Suncorp, the pattern of higher expenses and under preforming loans will soon become more evident for all the banking names.

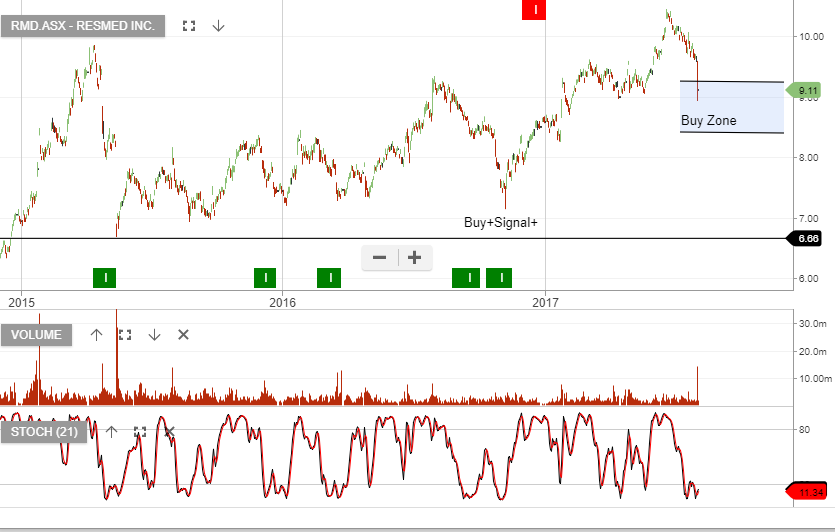

Global mask sales were weaker than expectations, but we see F18 device and mask growth rebounding.

FY18 revenue is forecast to grow by of 5%+ and underlying EPS growth in the high single digits.

RMD is trading at 24x F18 EPS and we see the current sell-off as a buying opportunity.

We need to give this name a wide range to find support and the buying zone is between $8.50 and $9.25. 1, 2 & 3 years out, the stock will be trading at higher prices. Keep an eye out for the next Algo buy signal in RMD!

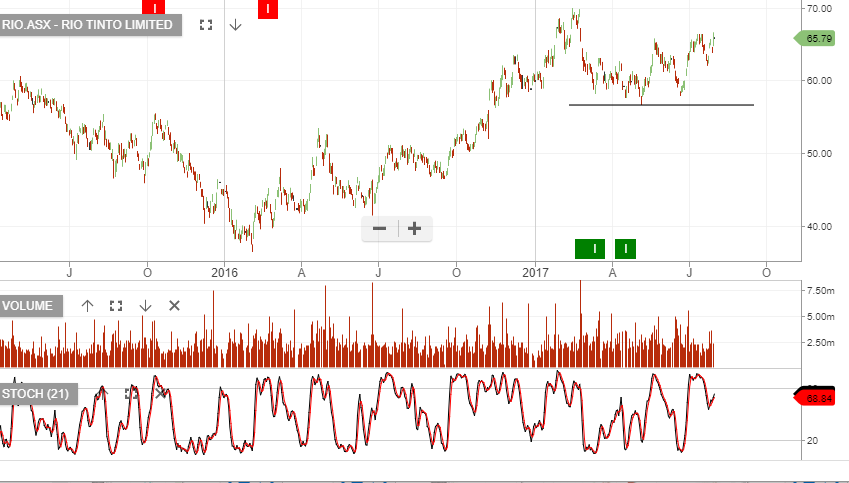

RIO reported 1H17 underlying earnings of US$3.9bn, which was largely in line with market expectations. EBITDA of US$9.0bn was also in line.

Lower capex resulted in cash flow and net debt coming in slightly better than exceptions (gearing now 13%) with net debt end of June US$7.6bn.

Buy-back was boosted by US$1.0bn increase, helping to offset a softer interim dividend. The interim dividend announced was US$1.10 and assumes 50% payout ratio.

In 2018 we expect RIO to see flat earnings growth at best, and we have the stock trading on a forward yield of 4.5%.

We’ve been long Woolworths following the recent Algo Engine buy signal.

Through adding a $28 December covered call option we’ve boosted the annualized cashflow to 10 – 12%, which includes capturing the $0.58 September dividend.

WOW reports on the 23rd August. The stock is trading on 20x FY18 earnings and 3.3% forward yield.

FY17 EPS is likely to around $1.50 per share and the market is forecasting underlying EPS growth into FY18 of 8 %, to $1.65 per share.

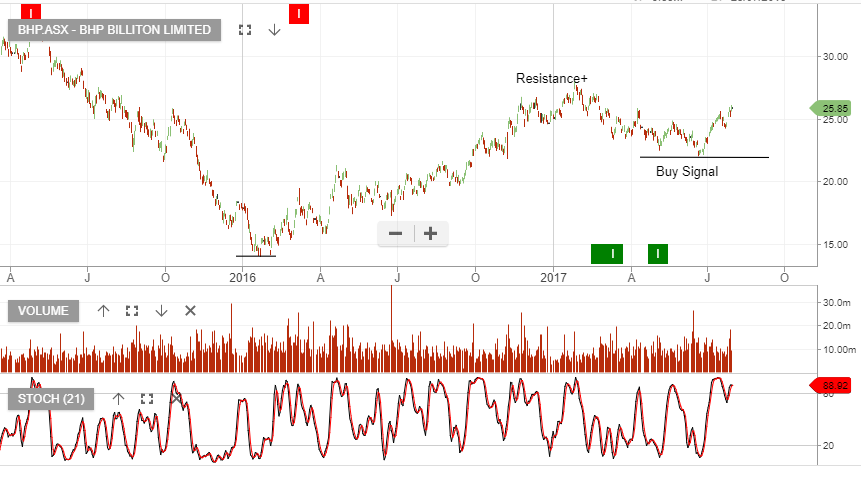

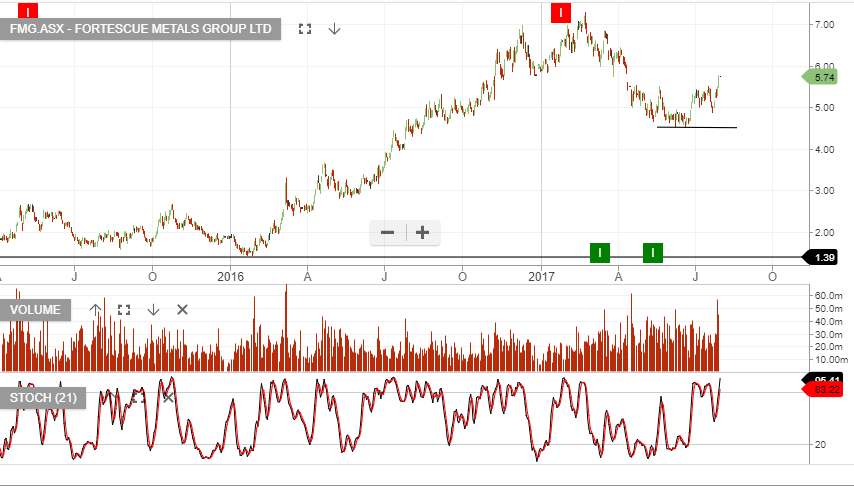

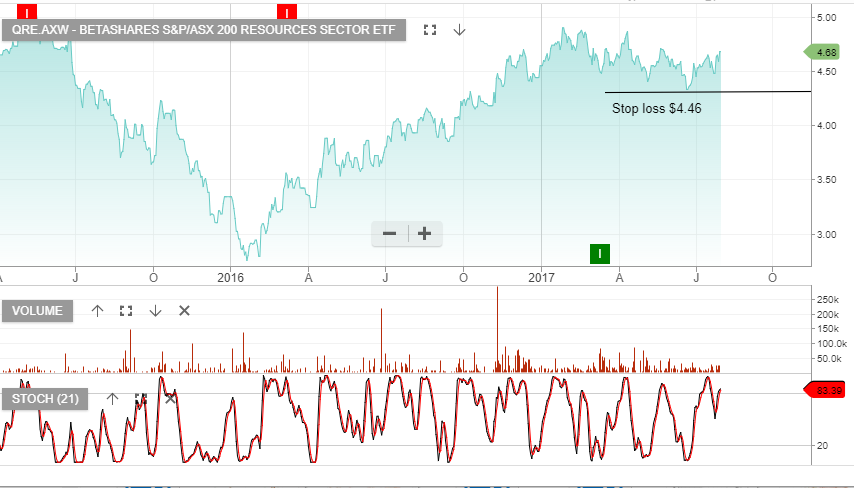

In late May our Algo Engine started flagging the “higher low” structure in large cap resource names, including a number of resource specific ETF’s.

Within the ASX 100, FMG, RIO and BHP were the standout Algo Engine buy signals. In client portfolio’s we allocated towards BHP as our preferred exposure.

Over recent weeks, a rally in Iron Ore prices from US$56 per tone to US$72 per tone, has helped to accelerate the share price advance, and crude oil back at almost $50 per barrel has helped BHP.

Fund managers continue to position in BHP ahead of a potential corporate restructure, as the market speculates on the divestment of the US shale and energy assets, into a separate listed US company.

BHP reports on the 22nd August . Assuming FY17 total dividends of $1.10, BHP trades on a 4.7% yield. EPS forecasts into FY18 should remain similar to FY17 at around $1.70 per share.

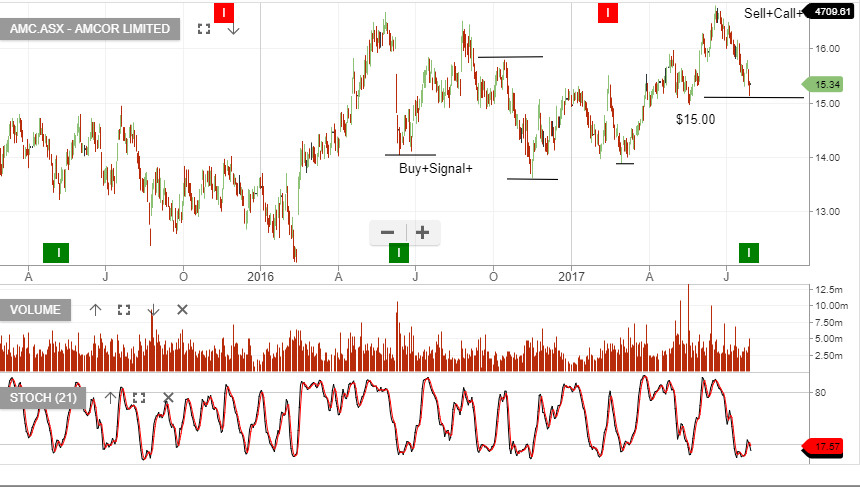

Our Algo Engine triggered a buy signal on Amcor as the stock forms a “higher low” pattern at or near $15.30.

Amcor reports earnings on the 22nd August, the market in looking for EPS growth of 8 – 10%. The recent rally in the AUD may see forward guidance reduced slightly, if the AUD was to stay above $0.80.

We continue to like Amcor as a buy and hold portfolio position, complimented with a covered call option. We’re allowing moderate capital growth and when combining the dividend with the covered call option, we’re generate 10 – 12% annualised cashflow.