We see continued upside for the fund, which offers investors diversified exposure to infrastructure sectors, including transportation, energy and telecommunications.

CIMIC’s global parent, Grupo ACS, will receive a cash injection of at least $4.5 billion if it accepts an $8 billion offer from French infrastructure group VINCI for its industrial services business.

Should the above transaction proceed, it will relieve pressure on its global cash flows.

The class action lawsuit filed against CIMIC, which alleges the group used supply chain financing to mislead investors about its cash flows and did not fully disclose the financial problems in its Middle Eastern joint venture, remains a negative overhang.

The share price has rallied 10% over the last week, which can be attributed to the funding news for the parent entity. We continue to like the investment theme and exposure to local infrastructure development, which CIMIC offers.

NST and SAR have announced a board-supported A$16bn merger of equals. Under the deal, SAR shareholders would receive 0.3763 NST shares for every SAR share held.

The deal is subject to SAR shareholder approval, Saracen will be merged into NST and no longer exist. The deal is expected to be completed in February 2021.

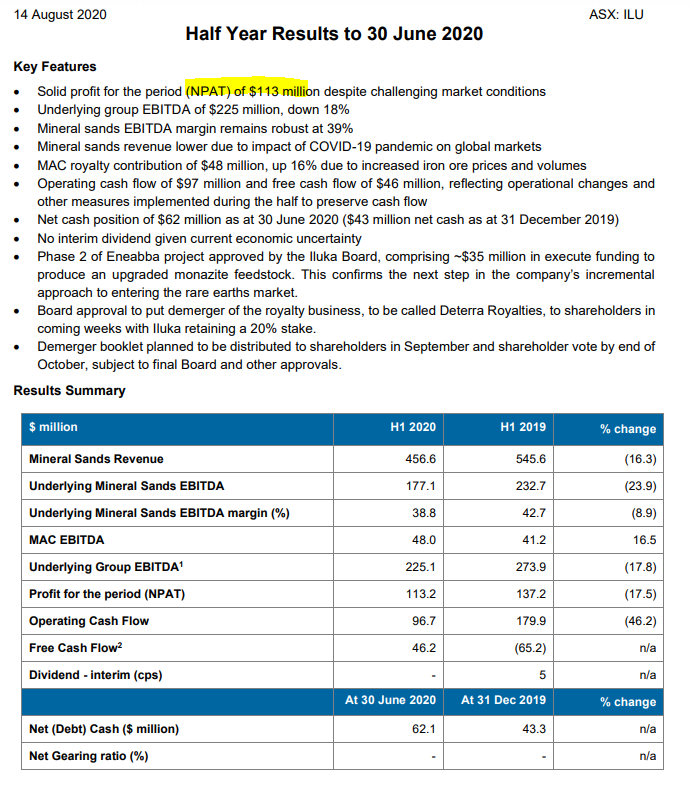

Iluka shareholders will have the opportunity to vote on the demerger at a meeting on 16 October 2020.

If the demerger proceeds, eligible shareholders will receive one share in Deterra for every Iluka share held at the demerger record date. Iluka will retain a minority shareholding interest of 20 percent in Deterra as a long-term investment.

The demerger will result in two independent ASX-listed companies – Iluka Resources Limited, a global leader in the mineral sands industry and Deterra Royalties Limited, the largest independent royalty company listed on the ASX, with the MAC iron ore royalty as its cornerstone asset.

Gold Road Resources is under Algo Engine buy conditions and we expect buying interest to rebuild near the $1.50 support level.

A combination of lower gold prices in the spot market and the recently announced interruption to production has seen the GOR share price fall from the $2.00 highs reached in July.

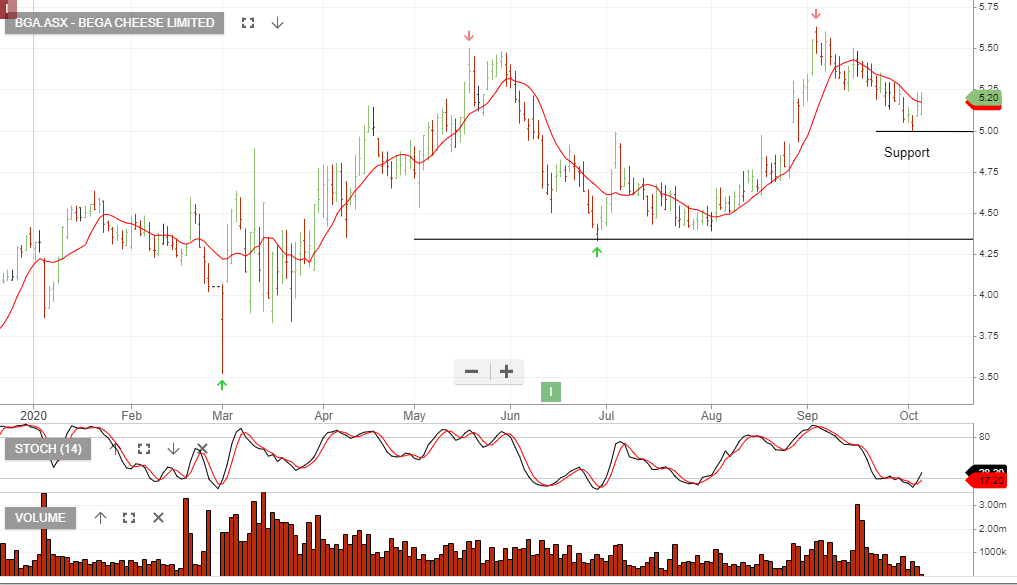

Bega Cheese is under Algo Engine buy conditions since forming a support base at $4.30 back in Jul/Aug. The stock price has since rallied on better FY21 earnings forecasts and the $5.00 level provides another opportunity for investors to accumulate the stock.