Bank of New York

We see further downside pressure on the banking sector and remain on the short-side of the Bank of New York Mellon trade.

We see further downside pressure on the banking sector and remain on the short-side of the Bank of New York Mellon trade.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

South32 is a globally diversified mining and metals company producing bauxite, alumina, aluminium, energy and metallurgical coal, manganese, nickel, silver, lead and zinc in Australia, Southern Africa and South America.

Earlier this week, Citi sent a note to clients suggesting Fortescue may look at a mega deal to buy the $9.7 billion diversified miner.

S32 remains under Algo Engine sell conditions, however, the opportunity is worth keeping an eye on, following the correction in the share price from $4.30 to $2.05 over the past 2 years.

We see value in accumulating Gold Road Resources at $1.50

Saracen Mineral Holdings has been added to the ASX 100 index and we draw investors attention to the strong price momentum.

The gold producer is benefiting from increased production and a strong gold price, which has resulted in record levels of retained cash earnings.

Altium is under Algo Engine sell conditions and is now trading below the downside momentum indicator.

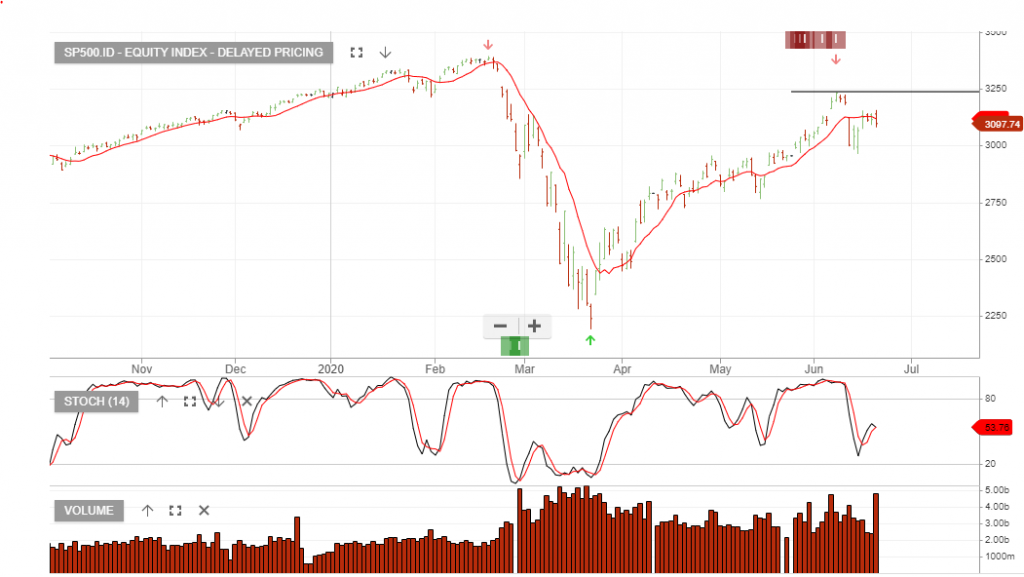

The chart below shows the XJO in after hours trading, which captures the US close on Friday night.

We anticipate the XJO opening Monday below the short-term momentum indicators, which could be the early signs of a large number of short positions within the ASX 200, beginning a corrective move.

We highlight the lower high formed from Friday’s close and the break below the short-term momentum indicator.

This should be monitored on Monday when the US reopens and investors should also be looking at the same patterns in the NASDAQ.

We’ll cover more on these trends in Monday night’s webinar.

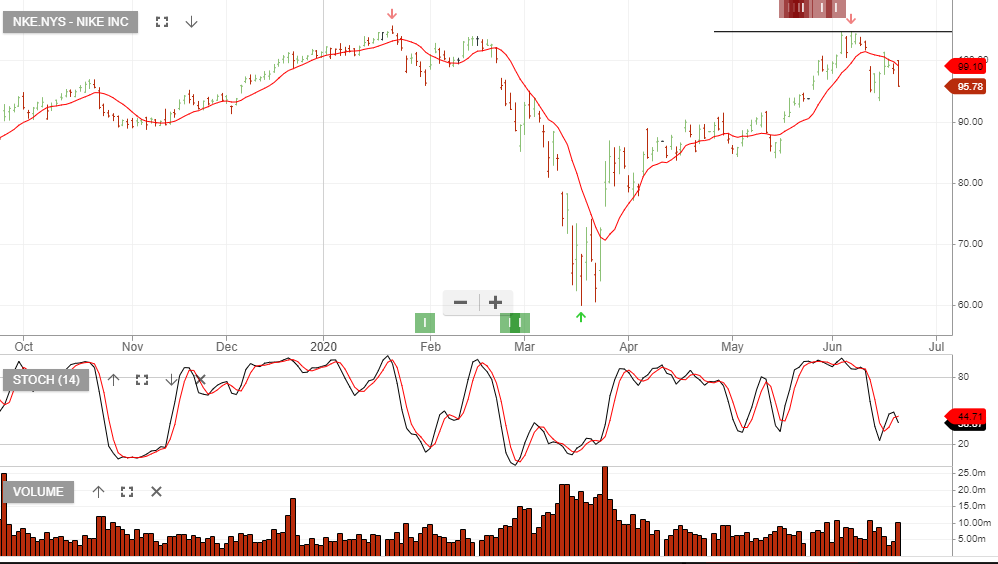

Nike is expected to report EPS of $0.18, down 70% from the prior quarter. Revenue down 20% to $8bn.

We see Nike as a shorting opportunity coming into the June quarter earnings result.

The above post was made on the 29th May and since then, the US market has pushed higher. With retail likely to fall short of earnings estimates, we remain cautious heading into next month’s earnings.

The below chart shows the updated price action in Nike, and of importance, the close below the momentum indicators.

Evolution Mining is on our radar as we soon expect the stock to switch from sell to buy conditions.

Sub $5.00 EVN looks interesting relative to other gold play alternatives.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453