CCL Has Reached The Sell Zone

Shares of CCL are up 3% in early trade as the company announced an 80% increase in net annual profit to $445.2 million.

Despite the underlying EBIT falling .7%, the share price has reached a 7-month high of $9.07.

In a blog post last Wednsday, we highlighted the bullish technical structure and that a break of the $8.45 level could point to an extention above $9.00.

Internal momentum indicators are now overbought and we suggest exiting long positions and looking to enter again at a lower level.

The company announced a dividend of 26 cents (70% franked) and goes ex-dividend on February 27th.

The first area of technical support for CCL will be at, or around, the $8.65 level.

Coca-Cola Amatil

Sydney Airport

Sydney Airport Transurban

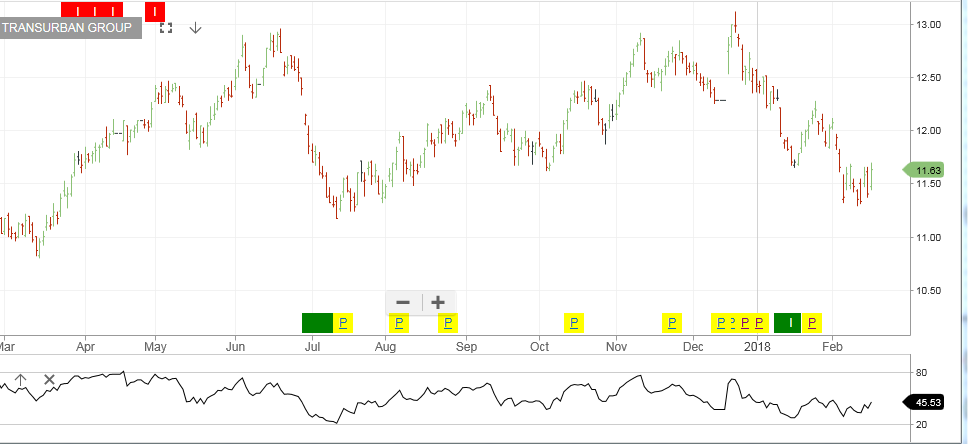

Transurban