Australian equities increased by 4% in October

Australian equities increased by 4% in October with IT up 9.3%, Energy 5.8% and Healthcare 5.5%.

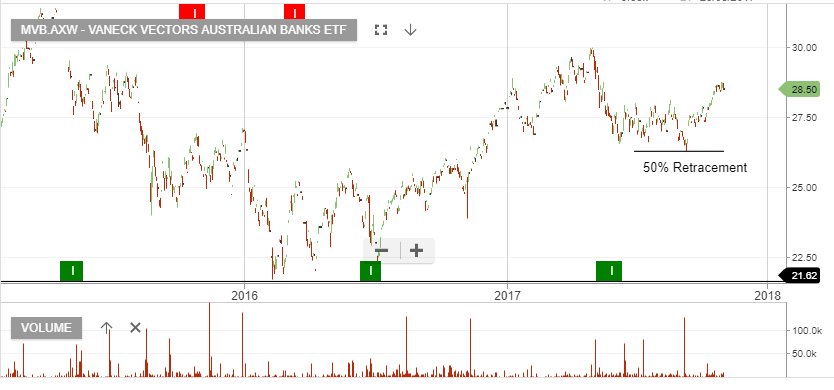

We’ve been allocating towards ORG, WPL, RHC & RMD to help capture these returns. There are incremental further gains in resources and energy, we’re cautious on banks and financials and forecast sideways to lower price consolidation.

High PE companies with US dollar earnings should now run into resistance. Examples being JHX, BLD, RMD, and CPU.

Newcrest Mining

Newcrest Mining AUD/ USD

AUD/ USD