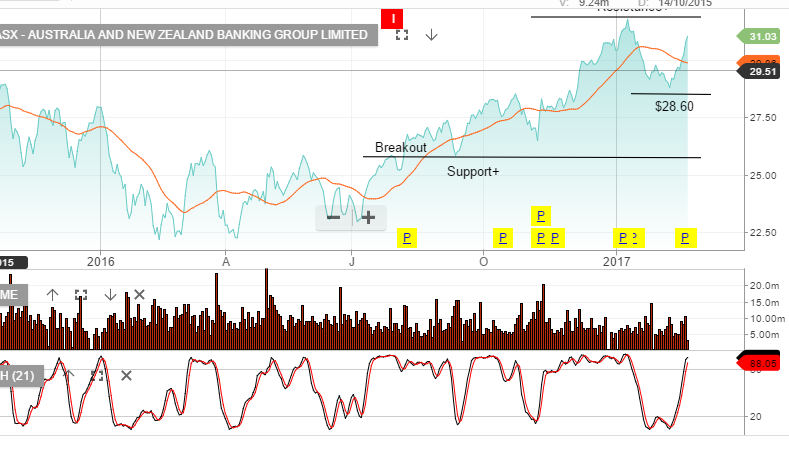

ASX- Valuation Review

Following the recent 1H17 earnings update, we will take a look at establishing fair value for the ASX.

1H17 NPAT of A$219m represented 3% underlying earnings growth. Moderate revenue growth occurred across most major ASX activities.

Here is the issue: the stock trades at 22x forward earnings on a 3.9% dividend yield. The earnings are stable but the stock is expensive. And whilst ASX delivered 3% revenue growth in 1H17, this is down on the 6% average level achieved over the last 3 years.

Our conclusion on fair value is; buy ASX on a pullback to $47 or a 4.5% dividend yield.