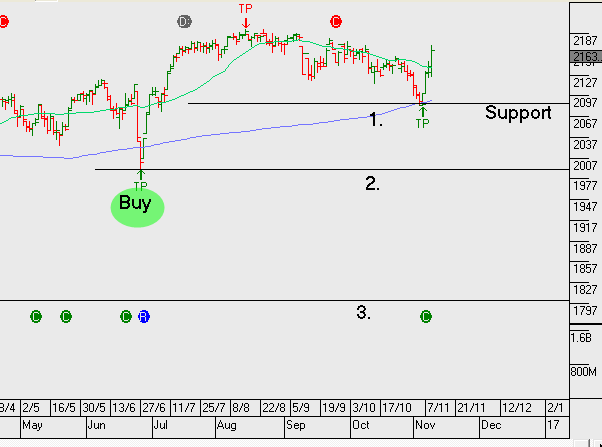

Yield sensitive names remain under pressure as the bond sell-off in the US continues. As bond prices trade lower, the yield is increasing. Higher yields, make interest rate sensitive names like infrastructure and property trusts less appealing.

The sell-off in domestic names such as APA, GMG, GPT, SGP, TLS, TCL, SYD, WFD & SCG has been significant. With many of these names now trading on yields within 4.5 to 6.5% range.

There’s a case to be made for the above stocks to find support as the outlook for interest rates begin to stabilise.

Medibank is struggling with top line growth of 1.5%, meanwhile underlying cost growth is running at an average of 5%.

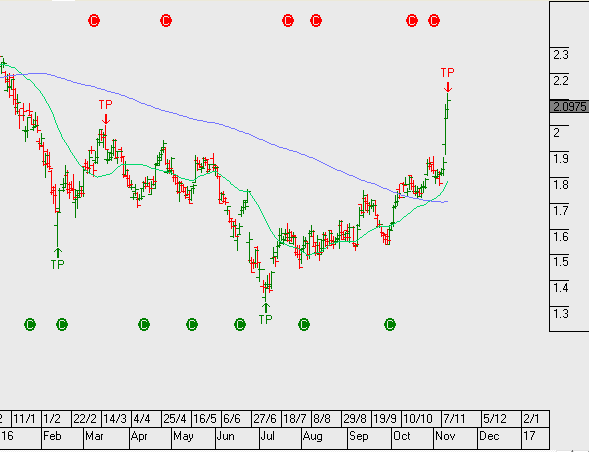

We were recent buyers of MPL at $2.35 and with the stock hitting our $2.60 price target, we sold calls to enhance to yield.

MPL is likely to trades sideways and investors should use covered calls to enhance the yield. Excluding the added income from call options, MPL trades on an FY17 forward yield of 4.7%, assuming profit of $420m, EPS of $0.15 and DPS of $0.12.

Through adding a covered call we are delivering in excess of 10% cash flow (plus franking credit) and allowing for moderate capital growth.

We’ve remained bullish equities and our base case has been that US stocks would hold support following a satisfactory 3Q earnings result. Our resolve was tested in the last 24 hours with US markets down sharply as the election result and Trump Presidency looked possible. However, by the time the Presidential acceptance speech began, the market losses on US indices were cut in half and by the close of US trading markets were up on average by 2%.

We keep our long bias towards equities and turn our focus back to the reality that 3Q S&P500 average earnings per shares growth is tracking at only 3.5% up on the same time last year. Considering the magnitude of share buybacks, we don’t consider the underlying earnings growth to be that encouraging. Chinese export data remains weak, reflecting the slow growth in the global economy and bond yields continue to push higher in the US with the 10year bonds now trading up from 1.3 to 2.05% over the last 3 months.

As stated in the monthly strategy review video, we caution portfolio investors on a blanket buy and hold strategy. We encourage you to establish contact with us, so we can discuss the advantage of adding a call option strategy to your holdings, as well implementing well timed trading ideas around the fringe of your portfolio to help deliver better outright returns.

At yesterday’s AGM, Computershare gave guidance for FY17 which suggests the group has found an inflection point in their earnings. After almost 2 years of earnings downgrades and underperformance, management is increasingly looking towards mortgage servicing for growth, as the mature share registry business faces structural pressure.

CPU guided towards FY17 EPS to be marginally up on FY16. Contribution from Mortgage Servicing is required to deliver the growth.

Forecast FY17 revenue $2b on EBIT of $500m, EPS of $0.57 and DPS of $0.27 placing the stock on a forward yield of 3.3%.

We continue to remain cautious and question the certainty of a sustained turnaround in earnings. We continue to watch this name from the short side. The algorithm engine will be tracking CPU for a short signal as the market bounces back after the post Trump victory rally.

Moranbah production remains strong with output hitting a new record. The Louisiana plant will come in below budget. Any new capital management will be contingent on better fertiliser prices and reliable output from the new Louisiana plant.

With gearing likely to begin falling over the next 12 months we may see capital management in Fy18 or FY19.

FY17 we see revenue increasing to $3.8b, EBIT increasing 10% to $490m, EPS of $0.18 and DPS of $0.11, placing the stock on a forward yield of 3.5%

IPL has struggled with difficult industry conditions over the past 18 months, the tide may be turning but we will wait for a higher low formation from the algorithm engine before setting up new buying levels.

CBA reported 1Q17 earnings of $2.4 billion, which was largely in line with market expectations. On pre-provision basis the result was marginally below consensus.

CBA’s result was supported by an improvement trading income and lower impairment expense. Revenue growth trends continued to slow with growth falling from 5% in FY16 to 3% in FY17.

FY17 outlook is for EPS of $5.40 and DPS of $4.20 placing the stock on a forward yield of 5.8%

CBA remains in a structural downtrend and like all bank holdings should be complemented with covered call options to enhance the risk reward scenario. Additionally, investors need to be cautious about being overweight banks as other more attractive opportunities exist within the group of ASX top 50 stocks. These companies also offer high yield plus franking credits supported by solid EPS growth.

DMP’s upgraded FY17 earnings guidance to NPAT growth of 30% and upgraded margin targets.

Group store openings guidance of 175-195 was maintained.

FY17 revenue $1.2b, EBITDA $250m, Net Profit $130m, EPS $1.48 & DPS $1.05 placing the stock on a forward yield of 1.5%. PE = 46x

The recent low on the 2nd of November created the first lower low pattern we’ve seen in DMP since December 2014. Nevertheless, with the earnings upgrade, it’s likely the stock price will bounce from here but we’re thinking momentum will fade once the rally gets into the $75 range.

On the 7th of September in the weekly video market review we looked at 4 short signals, CPU, QAN, ORI and FLT.

All four short trades have performed very well, although a question mark remains over ORI following the markets positive response to Friday’s earnings update.

Flight Centre has now sold off over 20% from our algorithm short signal, which was triggered in late August. The rapid sell-off last week in FLT was caused by the company downgrading their earnings guidance. We take this as an opportunity to cover the short position.

Sonic Healthcare (SHL.ASX) announced that they’re acquiring German Staber Lab Group for €120m or approximately AUD$175m. The deal will be funded by debt and cash on hand.

Sonic indicated that Staber revenue is around €80m or AUD115m and will be 4% earnings accretive in FY17. The market should view this transaction positively.

FY17 growth consensus for Sonic is 5%+ with a forward yield into FY17 of 4.4%.

We have been recent buyers of SHL on the pullback as indicated by the algorithm signal posted on last week’s blog.

Westpac 2H16 earnings result was in-line with market expectations and the dividend was maintained. 2H16 cash profit came in at $3.9b and DPS $0.94 with a payout ratio of 80%. ROE has fallen from 15% to a target of 13 – 14%.

Revenue growth was slightly negative which has been the case across most of the recent banking results.

FY17 outlook is for revenue to remain flat and underlying profit to be 3% higher at $12.6b, on EPS of $2.38 and DPS of $1.88 placing the stock on a forward yield of 6.3%.

We’re running covered calls over the bank holdings to enhance returns in what we see as a low growth environment.

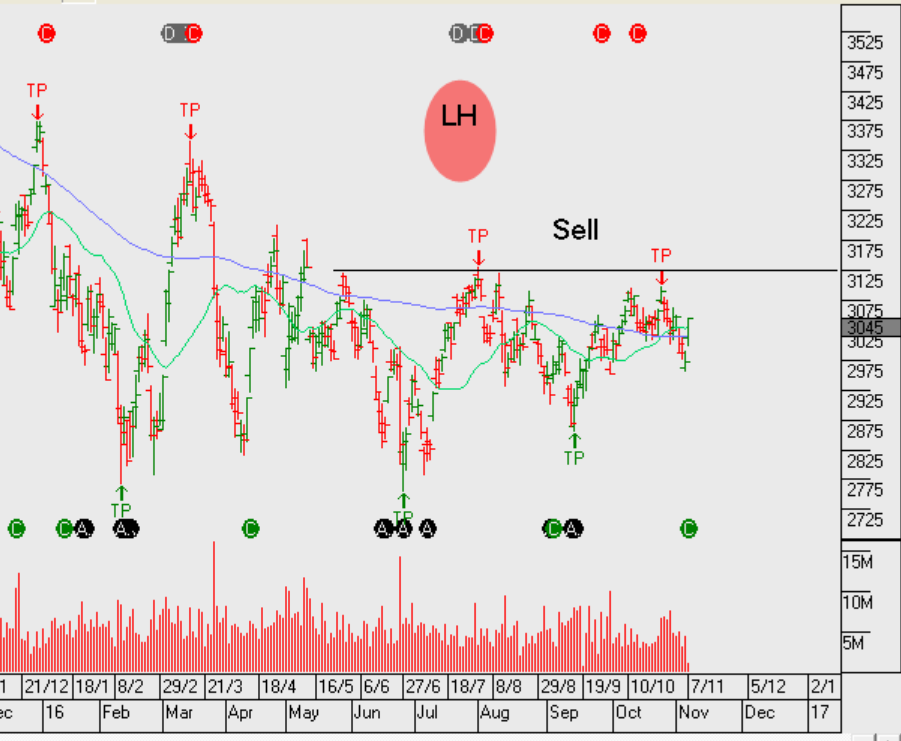

Chart Westpac Bank

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.