Insurance Australia FY16 Earnings Result

IAG.ASX reported FY16 cash NPAT of $867m and EPS of $0.36 and a final dividend of $0.13

FY17 guidance is for slightly softer insurance margins and DPS of $0.28 placing stock on a forward yield of 5%.

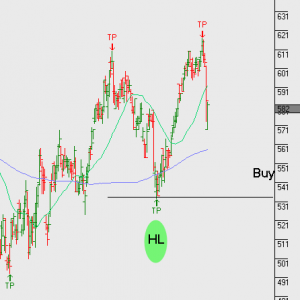

We’re comfortable buying IAG.ASX on a pullback to $5.50