AZJ FY16 Earnings Result

AZJ reported FY16 EBIT of $870 (down 10%). AZJ has a challenging outlook on the revenue front (9% decline to $3.45b) and their 100% payout ratio means that dividends are likely to be cut in the near future. The company remains focused on cost cutting and $130m in savings were achieved in the past 12 months, helping to reduce the impact of softer haulage volumes.

FY16 NPAT of $510m (down 16%) was impacted by higher interest expenses. Dividends per share (DPS) of $0.24.

FY17 EBIT guidance of $900m.

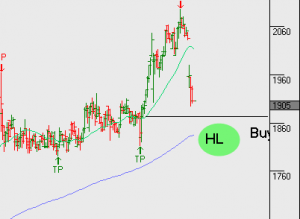

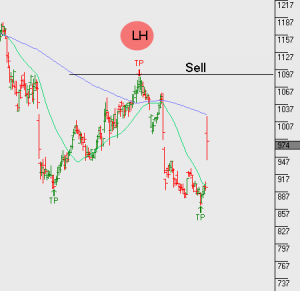

We’ve been on the short side of this trade and we now look to lock in profits.