Australian market finished the week….

|

|

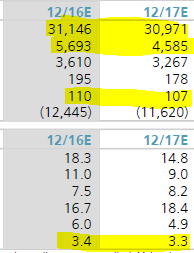

Earnings CTX.ASX

First half 16 EBIT $340 million is well above the $265 million in first half 15. Underlying forecast growth tracks at around 7% and forecast FY17 dividend of $1.03 (up from $0.94 in FY16) puts CTX on a forward yield of 3.3%.

Continue to maintain long position with $34 target + covered call.

Earnings IPL.ASX

First half 2016 underlying profit of AUD$137 million is down 6% of the same time last year. Full 2016 earnings should be around $360 million down 10% on Fy15.

Start up of new Louisiana plant in 2017 should create support for future earnings and we’re probably looking at the low point in the cycle for IPL.

FY17 forecast for $430 million profit on $0.25 EPS and $0.127 in dividends. No buy rec at this stage, waiting for the next bullish signal.

Earnings RIO.ASX

Starting at the top: Top line revenue flat, EBIT down 19%, dividend flat at $1.07 and trading on a 3.3% yield. Sell call options at $55 into November 16.

Note: 19th July – June quarter production numbers will be announced.

Long TCL.ASX

TCL reported 4Q16 traffic – trend remains positive for NSW, some softening is emerging in Melbourne and Brisbane. FY16 Proportional revenue across Australian roads was $1.7 billion. Look for FY17 dividend to increase from $0.45 in FY16 to $0.50 in FY17. This places TCL on a forward yield of 4.2%.

TCL is close to full value short term (12 month outlook) and should be complemented with a $12.70 covered call into March. We’ve collected an additional $0.50 for this call option and we expect to remain exposed to the $0.22 cent dividend in December. This trade allows for some capital gain if exercised. If TCL trades sideways, a combination of the dividend and the call option income creates approximately 10% cash flow on a stand still basis.

Rally in Resources

As discussed in the July video market update report, I forecast that money was in the early stages of rotating back towards the banks and resources. We’re now seeing this reflected in strong momentum within BHP and RIO. It’s likely that this trend will help lift the energy names as well.

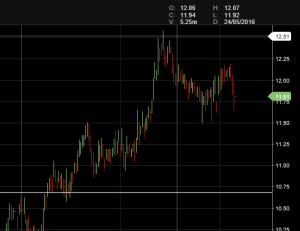

Long TLS.ASX

We had a buy signal at $5.20 in June. Telstra is now in a higher high, high low technical pattern and supported by 6% div yield. Investors are positioning ahead of the upcoming 1.5billion dollars to be retuned to shareholders in the next 6 months. TLS can rally through to $6.00 before investors may wish to look at locking in gains.

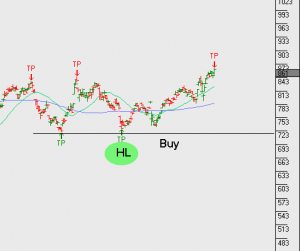

Long CWN.ASX

Crown is a slightly higher risk trade, however, I think James Packer is going to continue to be innovative in ways to unlock value for shareholders and it’s worth gaining exposure to the potential breakup story. Crown investors will gain exposure to the international assets, domestic property and domestic gaming assets. I’m looking for CWN to trade to $14 in the near term. Run a stop-loss below $11.30

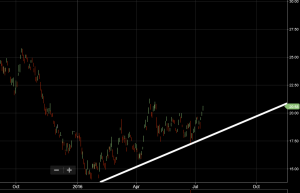

Long RMD.ASX

We’ve been long RMD since the buy signal back in March at $7.30. The rally is continuing with strong bullish momentum and we suggest clients lift the trailing stop-loss and allow price to trade into the $9.00+ range before taking profit.

Australian market finished the week….

The S&P/ASX 200 Index (XJO.ASX) finished the week down 0.3%. Materials sector showed buying interest with a rally of over 2.8% for the week, whilst financials lagged with the Financials ex-Property down 2.4%.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453