ConocoPhillips

Pfizer

Occidental Petroleum

Uber

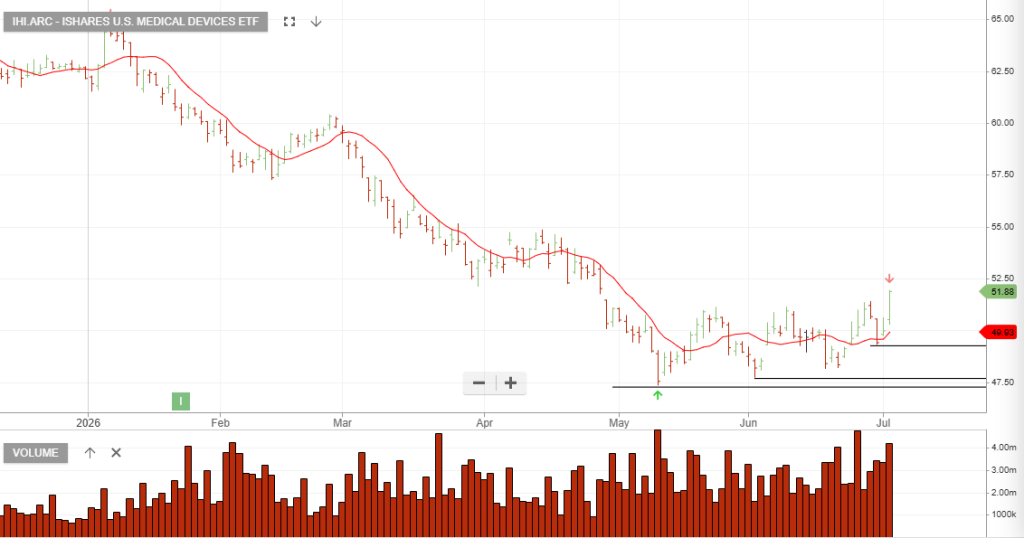

Medical Devices

Lockheed Martin

Regeneron Pharmaceuticals

Medtronic

Northrop Grumman

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453