Intuitive Surgical

Moderna

Zoom

Sea

Meta

ConocoPhillips

Occidental Petroleum

Comcast

Comcast Corporation – Class A Common plans to spin off its NBCUniversal and Sky businesses into a new publicly traded company, just months after completing its separation of the Versant brands.

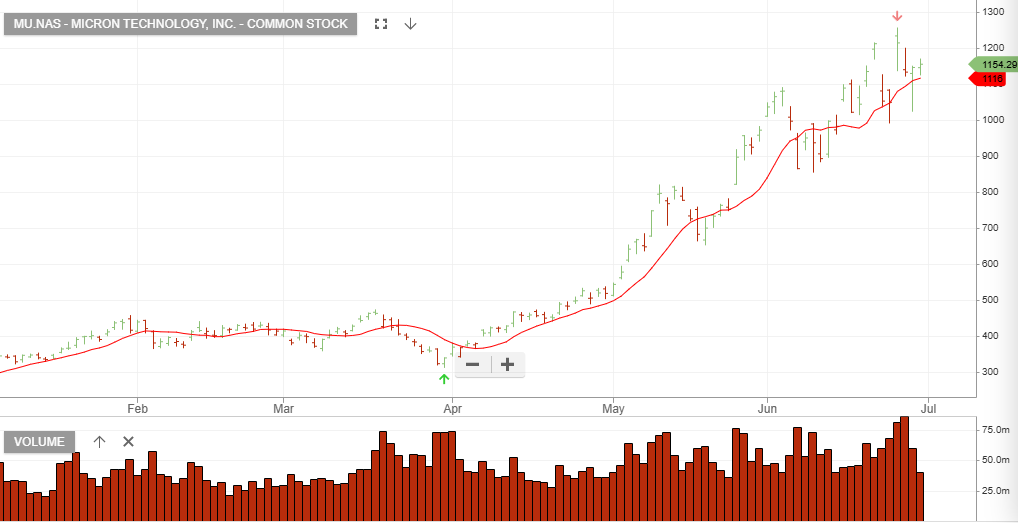

Micron

Micron Technology, Inc. – Common

Q3 revenue $41.46 billion +345.8% Y/Y increase, which is simply ridiculous to think about! The margin story is also impressive as non-GAAP gross margin stood at 84.9%.

Segment-wise – Core data centre 7x to $11.5B, cloud memory hit $13.8B and even automotive and embedded more than quadrupled to $4.6B.

Cash generation has also been phenomenal as operating cash flow stood at $25.4B and adj. FCF at $18.3B

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453