S&P500 Healthcare Index

The S&P500 Healthcare index is within 5% of finding support.

The S&P500 Healthcare index is within 5% of finding support.

The S&P 500 Materials index is within 5% of creating a support level.

INTC:NAS has moved to TSMC 3nm. That ensures the company’s GPU success is not tied to its new foundry business. Intel’s U.S. government support remains critical, and the new 18A node should help generate revenue growth.

We’re yet to see a shift in momentum, and the stock remains under Algo Engine sell conditions.

META:NAS is forecast to deliver 22% revenue growth this year, with sustained growth driven by AI and digital advertising.

Meta announced its Q3 results on October 30th, reporting 20% revenue growth and 26% operating profit growth. Q4 revenue should be $45-48 billion.

Meta was added to our US Tech Disruptors portfolio in August last year, and since then, the stock has increased 120%.

Lam Research Corporation – Common is rated a buy with a stop loss at $70.40

GE HealthCare Technologies Inc. – Common is rated a buy at $83

Medtronic plc. Ordinary is rated a buy $86

JD:NAS is rated a buy at $37

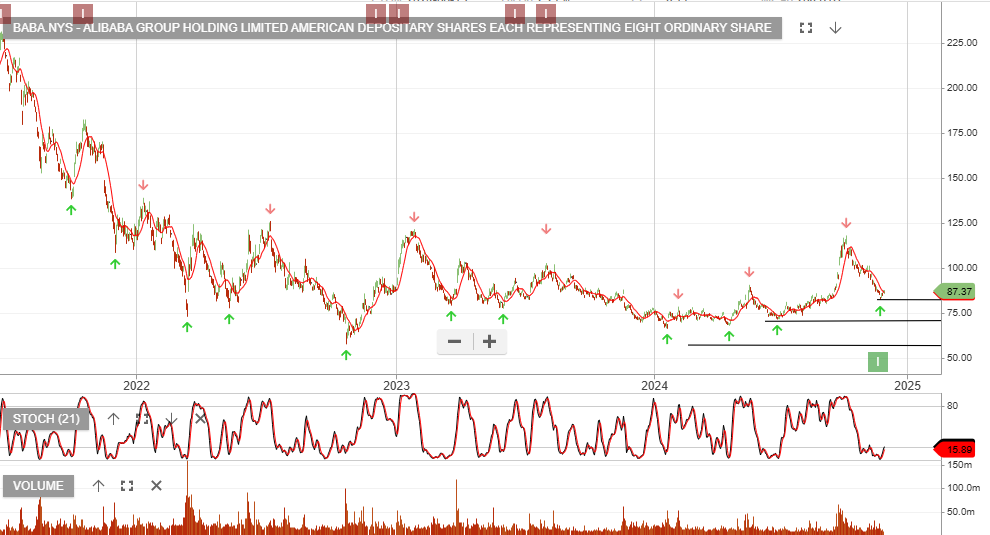

BABA:NYS is rated a buy at $87

Boeing Company (The) Common is rated a buy at $155

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453