Alibaba

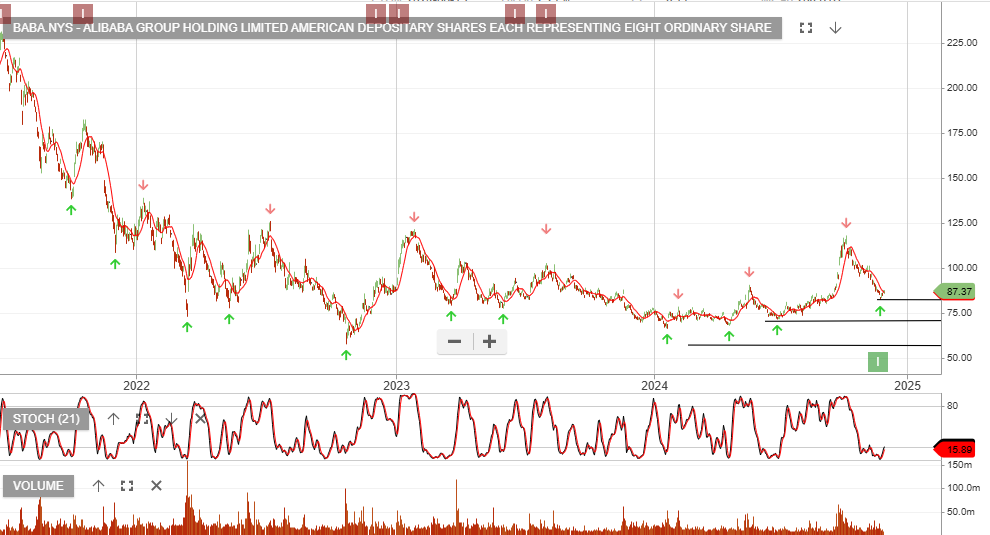

BABA:NYS is rated a buy at $87

BABA:NYS is rated a buy at $87

Despite nearly 16x more revenue and 3.6x more operating income, Alibaba is still trading at the same price as in 2014. We’re buyers of the stock based on an inflection point as new value is unlocked as Alibaba splits into 6 different components.

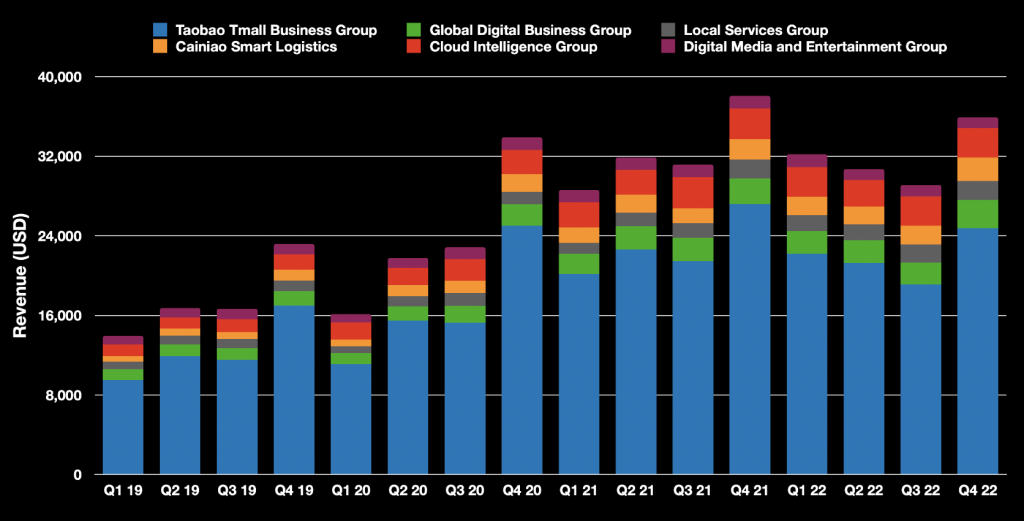

Taobao & Tmall

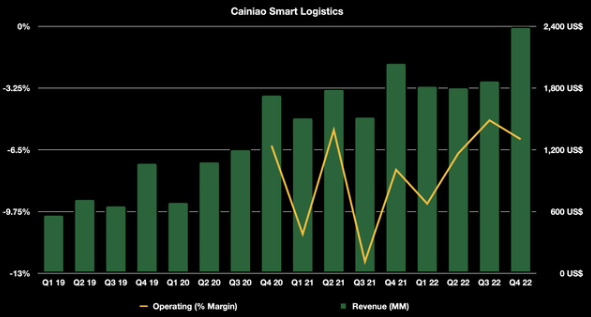

Cainiao Smart Logistics

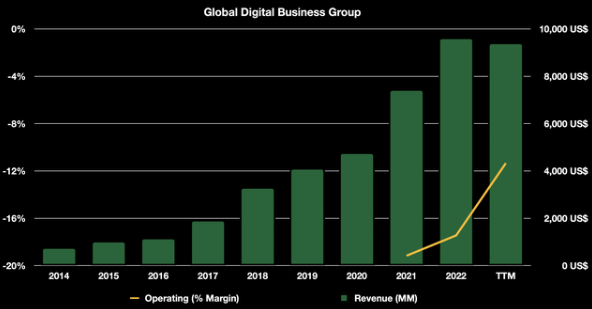

Global Digital

Cloud Intelligence

Local Services

Digital Media & Entertainment

Alibaba’s main business, Taobao & Tmall, is currently driving profits. Taobao is a consumer-to-consumer platform, while Tmall is B2C. Both companies target Chinese consumers.

The Global Digital Business includes Alibaba.com, AliExpress, Lazada and others and is mainly focused on international markets.

Cloud Intelligence, this segment alone could be worth more than Alibaba is currently valued at.

Cainiao Logistics is essential to Alibaba’s operations as it ensures smooth 24-hour delivery across China. The revenue growth of this unit has been quite amazing, with a CAGR of 46.49% since 2018. Widely regarded as one of the largest Unicorns in China.

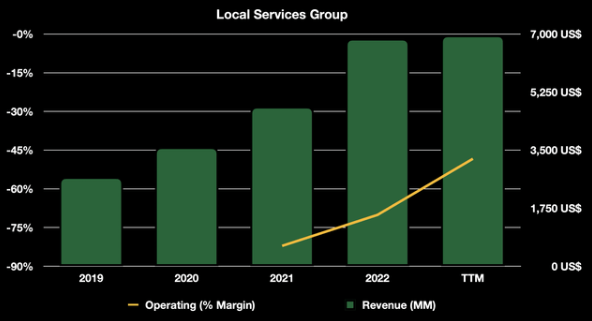

Local Service Group, These are mainly the DoorDash, Takeaway.com, Uber Eats, Yelp, Booking.com etc. in the Chinese economy.

Digital Media & Entertainment, consists of a range of different companies. One of them is Youku, one of the largest video hosting and streaming companies in China.

Buybacks – Almost one year ago, Alibaba Group announced an increase in its stock buyback from $15bn to $25bn. Alibaba bought back $9.66bn worth of shares in 2022 and for 2023 they’ve allocated $12bn+ for buybacks.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453