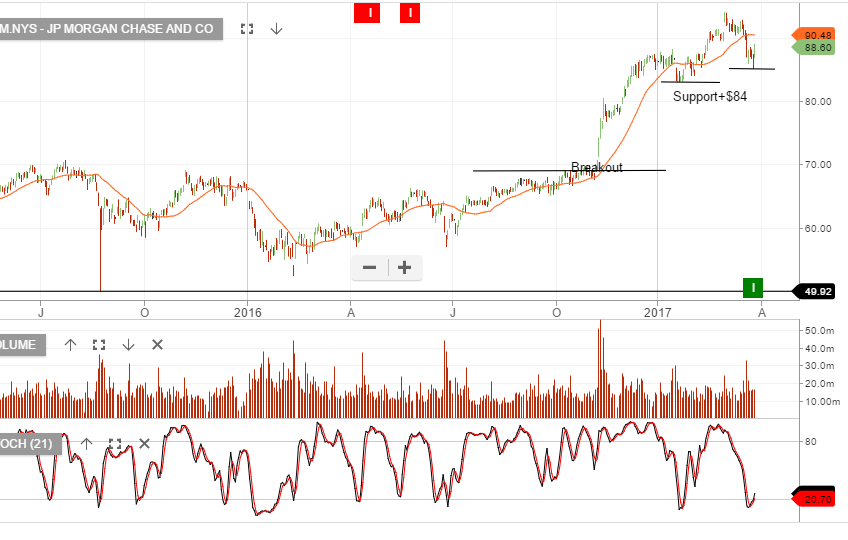

JP Morgan Slips 1% After Q1 Earnings Report

Shares of JP Morgan fell over 1% today as their Q1 earnings report included a sharp increase in write-downs.

The company reported earnings of $1.65 per share, which was up from an adjusted $1.35 reported a year ago and higher than the street estimates of $1.52.

However, concerns emerged in the bank’s consumer group, where credit costs surged to $1.4 billion, up almost $400 million from Q4 2016. This expense was driven by higher credit card charge offs.

As the other major US banks report their earnings next week, we will watch for similar write downs as a source of selling pressure.

JPM shares closed at $84.40, which is over 11% lower than the $94.00 high posted on March 1st.