Watch Last Night’s US Webinar

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

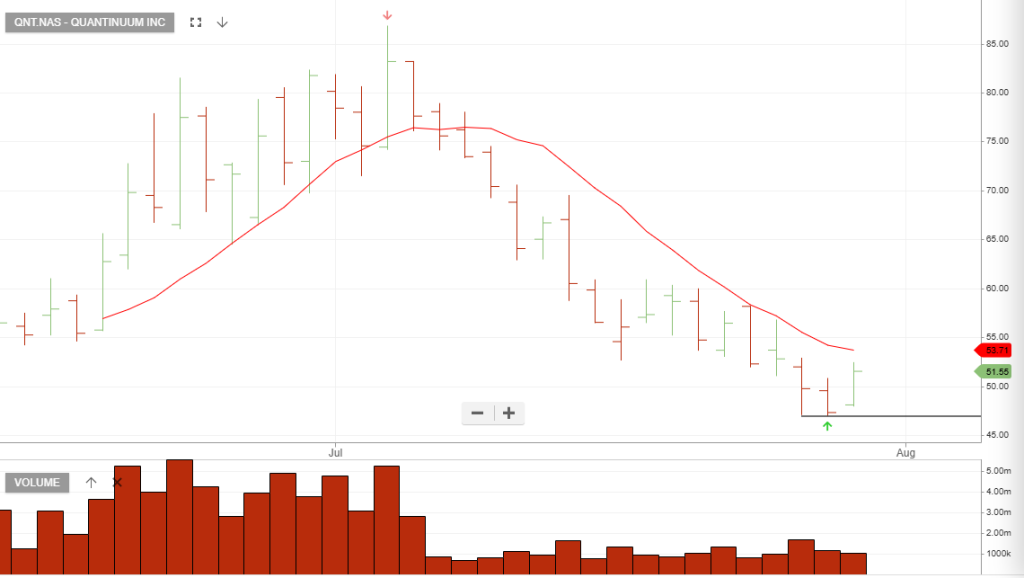

Quantinuum

will report its Second Quarter 2026 financial results after market close on Tuesday, August 11, 2026, followed by a conference call at 5:00 PM Eastern Time.

This marks Quantinuum’s inaugural earnings report as a public company following its $1.68 billion initial public offering (IPO) on June 5, 2026.

QNT has the deepest cash balance sheet and strongest corporate backers (Honeywell/Nvidia/JPMorgan) in the quantum space.

IONQ

{IONQ}

Upcoming Earnings Event: Q2 2026

Reporting Date: Wednesday, August 5, 2026 (After market close at 4:30 PM ET)*.

- Revenue Guidance: Management guided Q2 revenue in the range of $65.0 Million to $68.0 Million.

- Consensus Estimates:

* Revenue Consensus: ~$66.4 Million (+220% YoY).

Fundamental Highlights & Balance Sheet

- Liquidity: IonQ holds a massive liquidity cushion of ~$3.1 Billion in cash, cash equivalents, and marketable investments.

- Commercialization: ~60% of revenue stems from commercial (enterprise) contracts rather than pure government grants, with 35% coming from international markets.

- Vertical Integration: The ongoing acquisition and integration of semiconductor foundry SkyWater Technology ($1.8B deal) aims to onshore and scale chip manufacturing for IonQ’s next-gen systems.

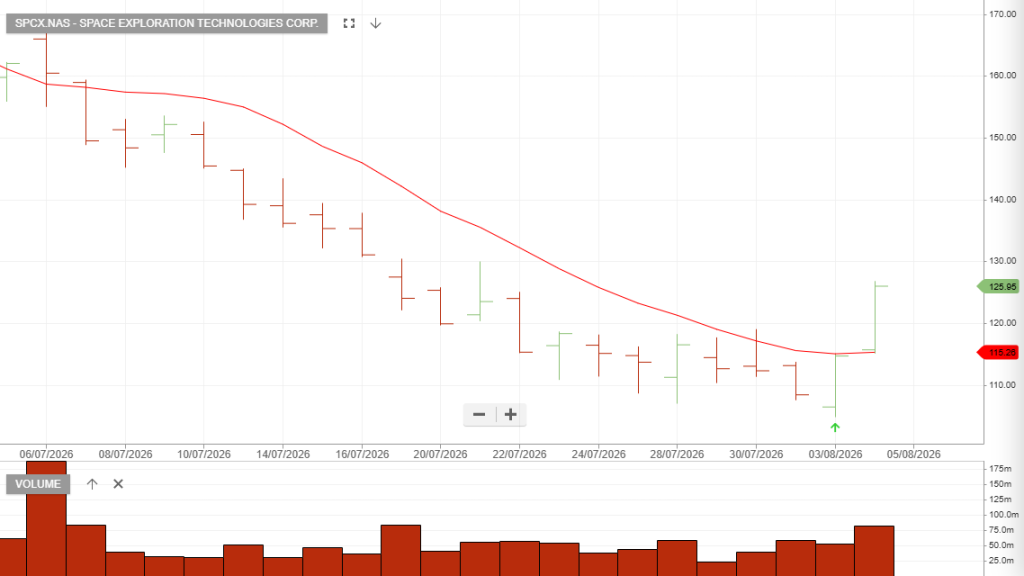

Space X

Space Exploration Technologies reported better-than-expected revenue for the second quarter in the company’s first earnings report since its record IPO in June. The stock dropped about 8% in extended trading as capital expenditures soared.

Here’s how the company did compared with analysts’ estimates, according to LSEG

- Revenue: $7.81 billion vs. $6.93 billion expected

- Loss per share: Loss of 9 cents vs. loss of 26 cents expected

Revenue jumped 92% from $4.1 billion a year earlier, SpaceX said in a statement on Tuesday, while the company’s net loss narrowed to $541 million from $1 billion.

SpaceX lost $4.9 billion last year, largely due to hefty investments in AI infrastructure.

AMD

Advanced Micro Devices, Inc. – Common reported second-quarter earnings on Tuesday that beat expectations, but the stock slumped in extended trading after rising during regular trading hours.

Here’s how the chipmaker did versus LSEG consensus estimates for the quarter ended June 27:

- EPS: $1.66, adjusted, versus $1.62 expected

- Revenue: $11.54 billion versus $11.28 billion expected

Overall, AMD revenue climbed 50% from $7.69 billion a year ago, a sign of the company’s central position in the market for artificial intelligence chips.

AMD’s Data Center unit is what is driving the company’s growth. Data Center sales were $6.7 billion, up 107% on an annual basis, which the company attributed to central processing unit and graphics processing unit sales.

The chipmaker sees $1.4 trillion of that coming from AI accelerators, or GPUs, up from a previous estimate of $500 billion by 2028.

Celestica

Celestica Inc. is rated a buy with the stop loss at $312.59

ARM Holdings

Arm Holdings is rated a buy with the stop loss at $219.39

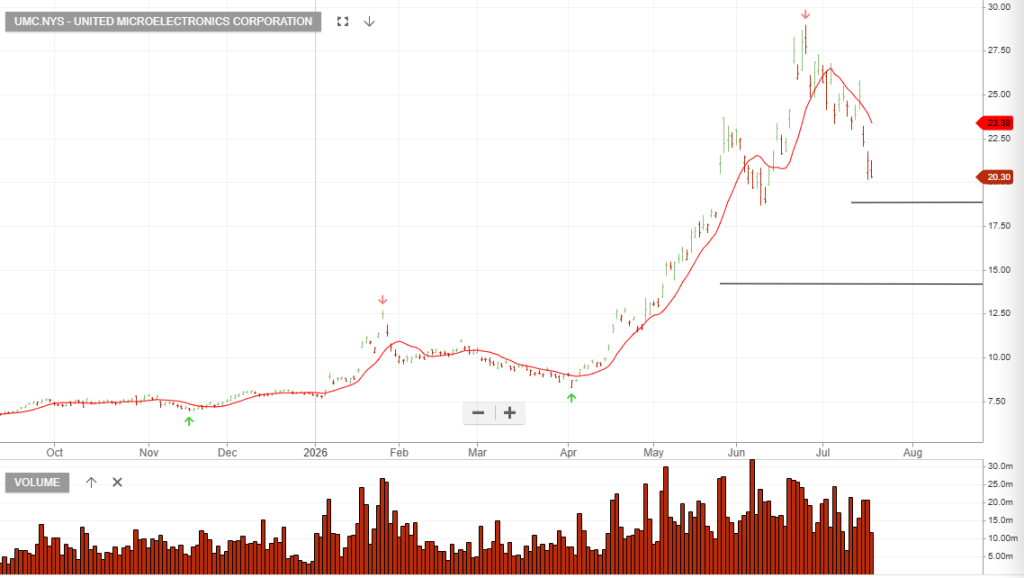

United Micro

5/8 update: is rated a buy with the stop loss at $17.49

Add to watchlist and look for interest to build near $18.50

In early 2026, UMC announced a high-profile partnership with Intel to collaborate on a 12nm platform manufactured in the US. This partnership is slated for commercial production in late 2027 and vastly diversifies UMC’s geographic footprint.

- Strong Balance Sheet: Fitch affirmed UMC’s BBB+ credit rating with a “Stable” outlook in June 2026. The company boasts a low debt-to-equity ratio of ~0.19 and a healthy current ratio of ~2.72.

- Next Earnings Release: UMC is scheduled to report its Q2 2026 earnings on Wednesday, July 29, 2026. Analysts expect EPS of 15 cents on revenue of ~$2.06 billion, representing growth over the prior year.

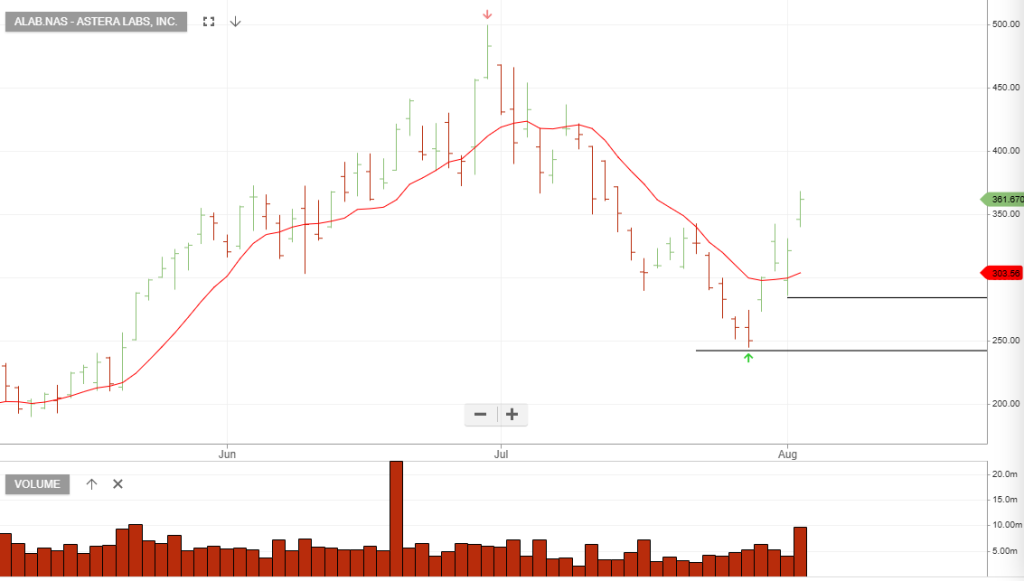

Astera Labs

Astera Labs, is rated a buy with the stop loss at $285.68

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453