US Earnings

Monday, August 10: Simon Property Group, Plug Power.

Tuesday, August 11: Cardinal Health, CoreWeave, Super Micro Computer.

Wednesday, August 12: Tencent, Cisco, Coherent.

Thursday, August 13: Applied Materials.

Monday, August 10: Simon Property Group, Plug Power.

Tuesday, August 11: Cardinal Health, CoreWeave, Super Micro Computer.

Wednesday, August 12: Tencent, Cisco, Coherent.

Thursday, August 13: Applied Materials.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

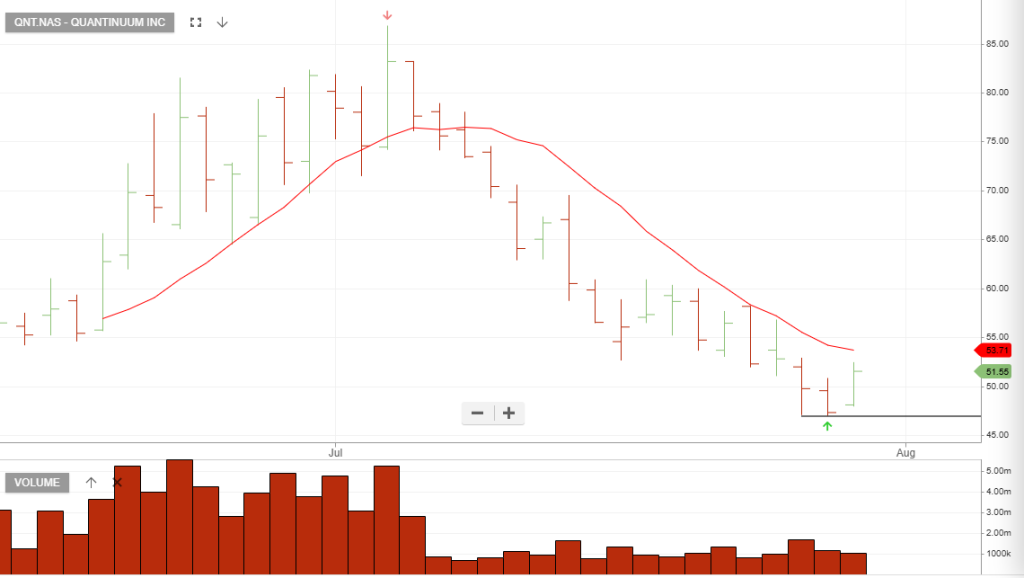

will report its Second Quarter 2026 financial results after market close on Tuesday, August 11, 2026, followed by a conference call at 5:00 PM Eastern Time.

This marks Quantinuum’s inaugural earnings report as a public company following its $1.68 billion initial public offering (IPO) on June 5, 2026.

QNT has the deepest cash balance sheet and strongest corporate backers (Honeywell/Nvidia/JPMorgan) in the quantum space.

{IONQ}

Upcoming Earnings Event: Q2 2026

Reporting Date: Wednesday, August 5, 2026 (After market close at 4:30 PM ET)*.

* Revenue Consensus: ~$66.4 Million (+220% YoY).

Fundamental Highlights & Balance Sheet

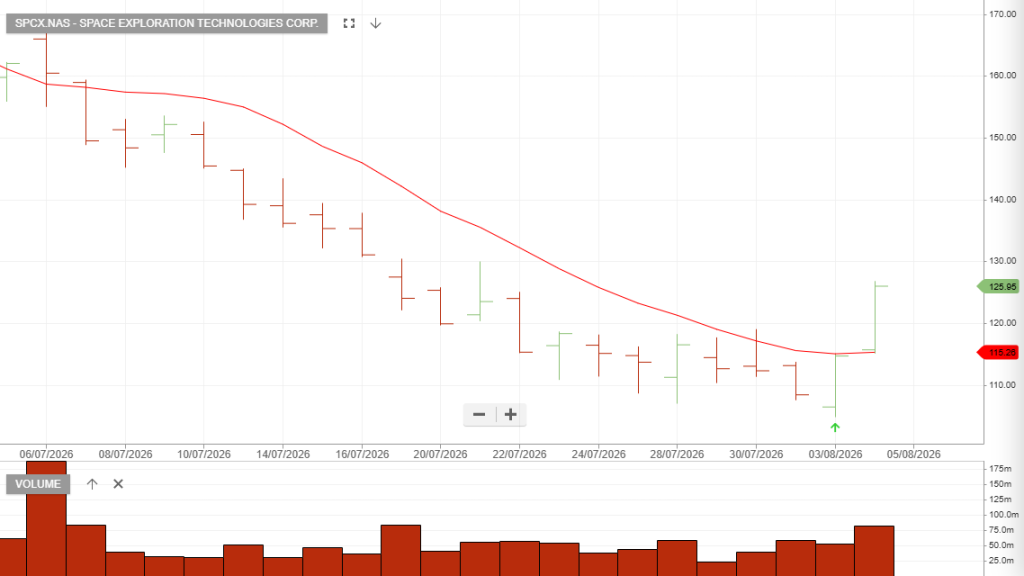

Space Exploration Technologies reported better-than-expected revenue for the second quarter in the company’s first earnings report since its record IPO in June. The stock dropped about 8% in extended trading as capital expenditures soared.

Here’s how the company did compared with analysts’ estimates, according to LSEG

Revenue jumped 92% from $4.1 billion a year earlier, SpaceX said in a statement on Tuesday, while the company’s net loss narrowed to $541 million from $1 billion.

SpaceX lost $4.9 billion last year, largely due to hefty investments in AI infrastructure.

Advanced Micro Devices, Inc. – Common reported second-quarter earnings on Tuesday that beat expectations, but the stock slumped in extended trading after rising during regular trading hours.

Here’s how the chipmaker did versus LSEG consensus estimates for the quarter ended June 27:

Overall, AMD revenue climbed 50% from $7.69 billion a year ago, a sign of the company’s central position in the market for artificial intelligence chips.

AMD’s Data Center unit is what is driving the company’s growth. Data Center sales were $6.7 billion, up 107% on an annual basis, which the company attributed to central processing unit and graphics processing unit sales.

The chipmaker sees $1.4 trillion of that coming from AI accelerators, or GPUs, up from a previous estimate of $500 billion by 2028.

Celestica Inc. is rated a buy with the stop loss at $312.59

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453