Pro Medicus – Review

Pro Medicus delivered another record result, with strong growth supported by new contract wins.

We continue to see this as an attractive growth opportunity.

Pro Medicus delivered another record result, with strong growth supported by new contract wins.

We continue to see this as an attractive growth opportunity.

{A2M} is now under Algo Engine buy conditions and we see buying support at $18.50.

TPG Telecom has traded down to $7.07 and we see an opportunity approaching where the stock price is likely to reach oversold levels.

Keep an eye on the short-term momentum indicators, especially if we see a probe below $7.00.

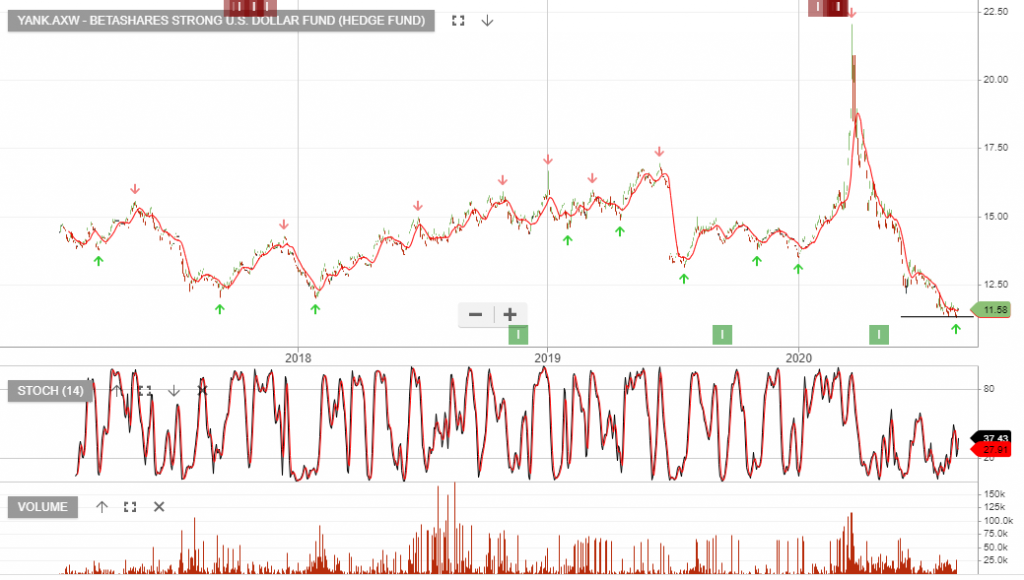

Betashares Strong U.S. Dollar Fund (Hedge

The US dollar has been trading lower over recent weeks and should we see a pick up in market volatility and risk-off sentiment builds, the US dollar may find increased buying support.

YANK looks to be finding support at $11.25

Newcrest Mining remains under Algo Engine buy conditions and we recommend investors accumulate between $32 – $34.

Beach Energy is the only top 100 energy stock under algo engine buy conditions. Buying interest is building above the $1.40 support level.

FY20 underlying NPAT of A$500mn was ahead of market expectations.

The A2 Milk Company is now under Algo Engine buy conditions and has recently been added to our ASX 100 model portfolio.

A2M reported 2HFY20 earnings showing strong EPS growth underpinned by higher infant formula volumes.

The result fell slightly short of high expectations, although revenue growth remained strong, increasing by 30% on the same time last year and FY20 EBIT jumped from $410mn to $550mn.

FY21 consensus for EPS growth is 15%.

At 30x forward earnings and no dividend yield, A2M is expensive but the growth metrics remain attractive.

The company continued its growth trajectory in FY20 with revenue from underlying operations up 24% and underlying profit before tax up 33%.

Brambles remains under Algo Engine buy conditions.

FY20 earnings were in-line with market consensus with EBIT flat on the same time last year. On a constant currency basis, EBIT increased 4%, which was in-line with management guidance for 3 – 5% growth.

BXB generates a large percentage of its revenue from consumer

staples and grocery supply chains, making it a relatively safe harbor for investors. At 22X forward earnings and a 2.2% yield, there’s not much upside in the share price on a 12-month outlook.

We suggest investors add a covered call option to enhance the income return.

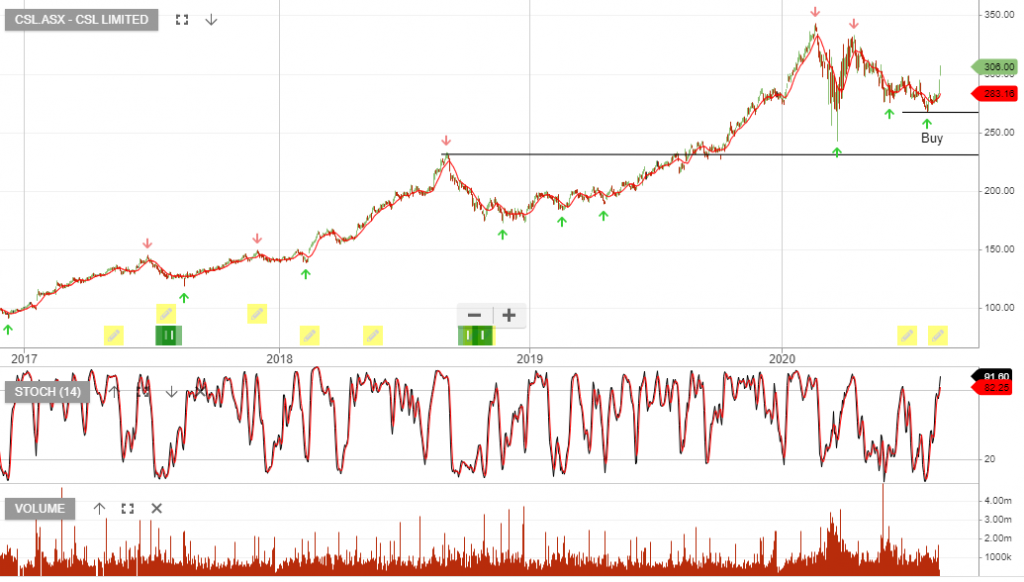

We’ve been highlighting the buy-side opportunity in CSL from the $270 support level. The share price has since rallied 15% and traders can now consider locking-in the gains.

Investors may wish to stick with the longer-term momentum and reassess following the FY20 earnings release today.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453