Shares of QBE are up over 5.5% in early trade as the insurance giant reported a 5% jump in net profit, as well as, a $1 billion share buyback scheme.

In the year up to December 31st, the company announced net profit after tax of $844 million, which is up from $807 million over the previous year. Return on equity also improved from 7.5% to 8.1%.

QBE declared it will pay a 33 cent dividend, compared to 30 cents last year.

QBE is fully valued and we recommend selling covered call options to enhance the investment return.

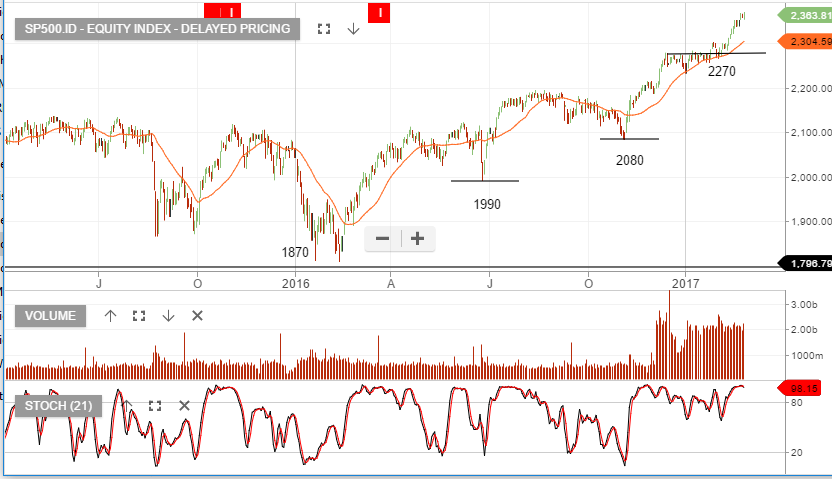

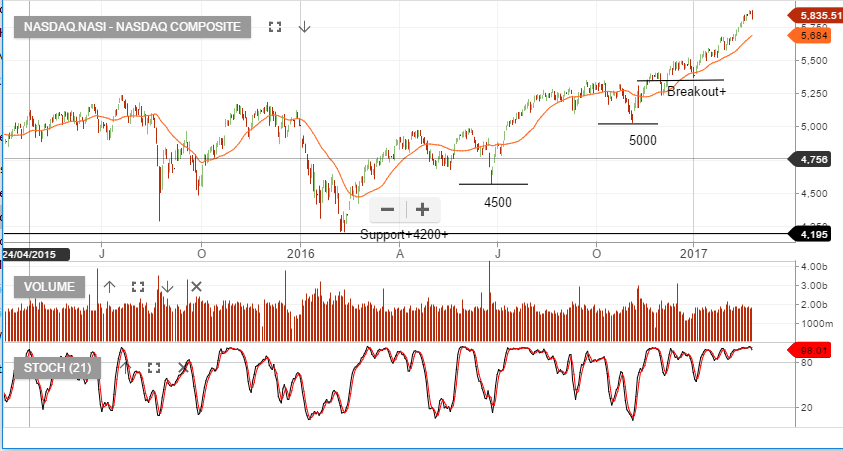

A late push on Wall Street helped US Stocks recover and allow the DOWJONES 30 Index to extend its winning streak to an 11th day.

For the week, the DOW rose 1%, the SP 500 picked up 0.7% and the NASDAQ closed out the week pretty much unchanged.

Looking ahead to next week, President Trump will deliver a speech before a joint session of Congress, when he is expected to give more details about his tax plan, trade policies and the direction of health care in the USA.

It’s interesting to see that the Investor Signals ALGO engine gave a sell signal for 2 pharmaceutical companies today: Eli Lilly (LLY) and Pfizer (PFE). Those sell signals were posted at $82.85 and $34.25, respectfully.

US Drug companies have shown weakness on Mr Trump’s comments about health care reform in the past and investors will be listening closely to his speech on Tuesday.

The DOW Jones 30 Index posted its 10th straight winning day in a row overnight. The fact that each one of those 10 winning days was a new record high has not been achieved since 1987.

This most recent leg higher in Dow started on November 8th, after the result of the US election. Since then, the DOW has gained 2,515 points, or 13.75%.

A widely held theme for the US equity rally has been the reflation of the US economy under a more business-friendly administration. This reflation theme was largely based on across the board tax cuts and a country-wide infrastructure construction plan.

The idea being that these new policy measures would stimulate growth and push inflation, interest rates and stock prices higher. Along these lines, the yield on the US 10-year note climbed over 83 basis points, or 6%, from mid-November to late December.

However, over the last several weeks, the US yields have stopped moving higher and the Treasury curve has stopped steepening. In fact, over the last 10 day rally in the DOW, yields on the 10-year notes have actually dropped from 2.48% to 2.37%.

In short, while the DOW has firmed to new highs over the last 10 sessions, the inflation part of the reflation trade is beginning to fade.

From a traditional value-metric point of view, if the recent move higher in US stocks were signalling a new leg higher in valuations, we would have expected the 10-year yields to have traded higher, not lower.

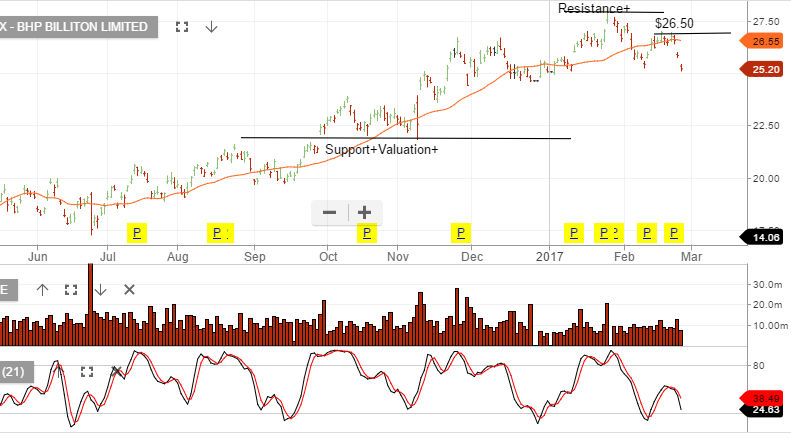

We’ve sold $27 call options over BHP into April and quit all other metals exposure. Our preference for BHP over other resource names is based on our assumption that energy prices will remain supported in the near term.

Three factors will likely support energy prices short term: The Trump administration’s policy will likely be bullish for energy, OPEC and Saudi production cuts and the Saudi Aramco IPO early next year (biggest IPO in history). The IPO will be better received in a supportive energy environment.

For this reason we’ve kept BHP, and sold at the money call options to boost cash flow to 10 – 12%.

We’re not overweight the stock since we see risks building for the market, in general, and Iron Ore prices, specifically.

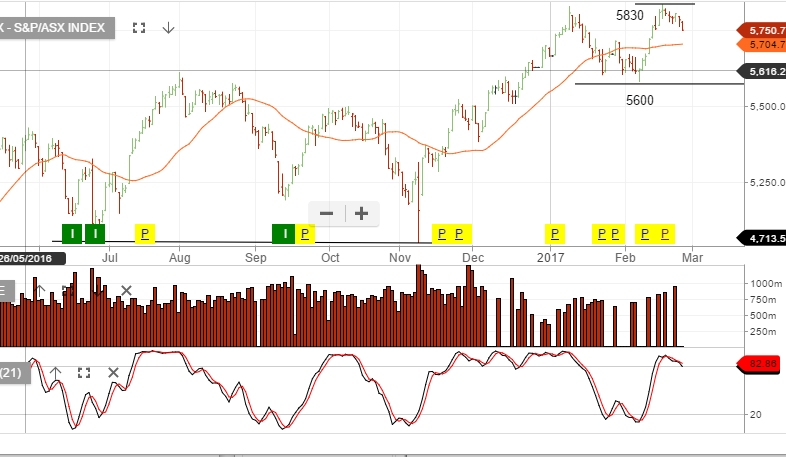

We’ve been cautious of the resource names rolling over from the recent highs and the potential negative impact on the overall XJO index. It appears that the broader Australian market may be in the early stages of a price correction.

Also, the Australian banks appear fully valued given the low revenue and profit growth outlook across the next 12 to 18 months.

Insurance Australia Group (IAG) reported a 4.3% drop in first-half profits to $446 million, which was down from $466 million from the previous corresponding period but slightly higher than the street’s expectations.

Amid an atmosphere of increased claim pressures, Australia’s largest insurer by market share announced its gross written premium grew by 4.7% to $5.8 billion.

IAG declared an interim, fully franked, dividend of 13 cents per share to be paid on March 30th. This dividend represents a cash payout ratio of 64.3 %.

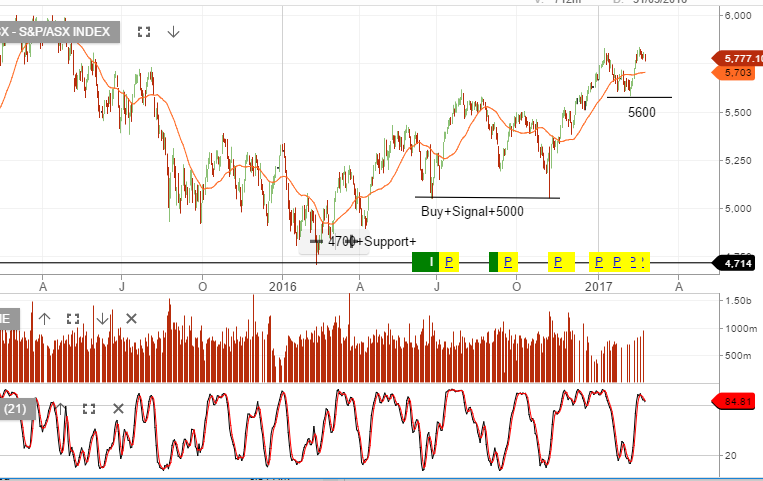

The XJO remains near recent resistance as more than 50% of top 200 companies have reported their earnings. Average reported revenue is up 3.4% on the same time last year and underlying average profits are up 6%.

The Dow Jones chart shows the index breaking to the upside of the recent 20,000 consolidation range.

We remain cautious of the extended share price valuations and moderate underlying earnings growth.

For this reason we continue to tilt client portfolio’s towards defensive assets. We prefer reducing exposure to resource and banking stocks across the next quarter and increasing exposure to healthcare and consumer staples.

Our tight covered call overlay is boosting cash flow to 10 – 12% per year.

Coca Cola delivered solid 2016 earnings result (+6.2%), which met market expectations. The announcement of a $350 million share buyback was a positive surprise.

Structural pressures from shrinking CSD consumption will need to be off-set by continued cost out programs, such as the announced closure of the SA bottling plant.

A positive trend remains the growth in Indonesia/PNG, which delivered double-digit earnings over the past 12 months.

Looking into 2017, we expect revenue of $5.2billion, EBITDA $980m, EPS $0.58 and DPS of $0.48 placing the stock on a forward yield of 4.8%.

We own CCL in client portfolios and we’ve been selling tight covered call options to boost the cash flow to 10 – 12%+ on an annualised basis.

Chart – CCL

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.