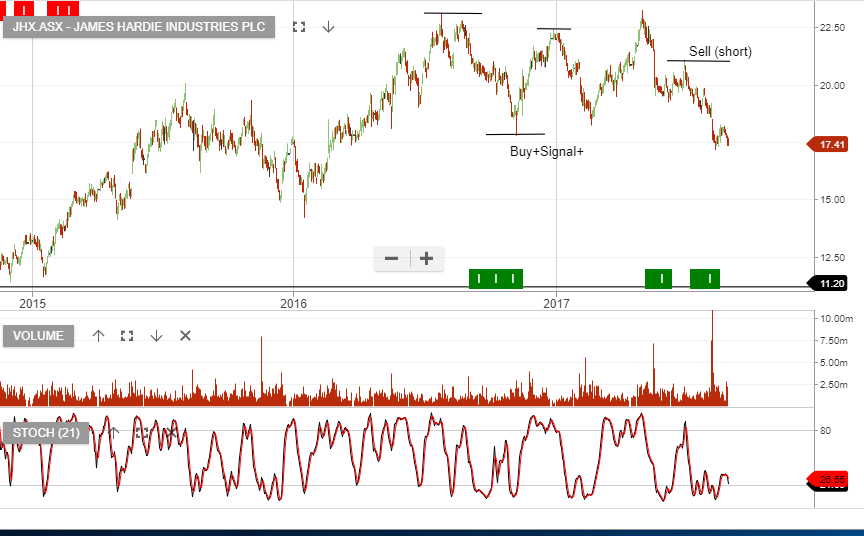

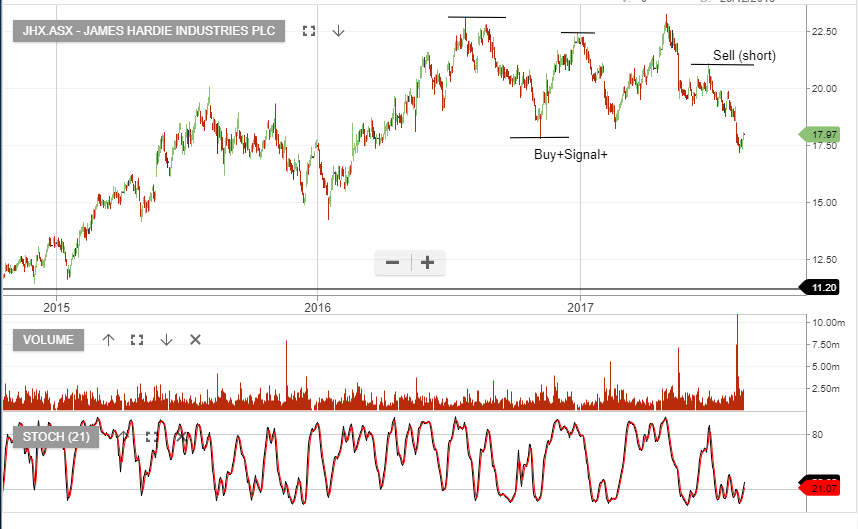

ALGO Signal: Sell James Hardie

Our ALGO engine triggered a sell signal on JHX at $21.51 at yesterday’s ASX close.

Internal momentum indicators have been showing an “overbought” pattern since November 10th, which supports the ALGO Sell signal.

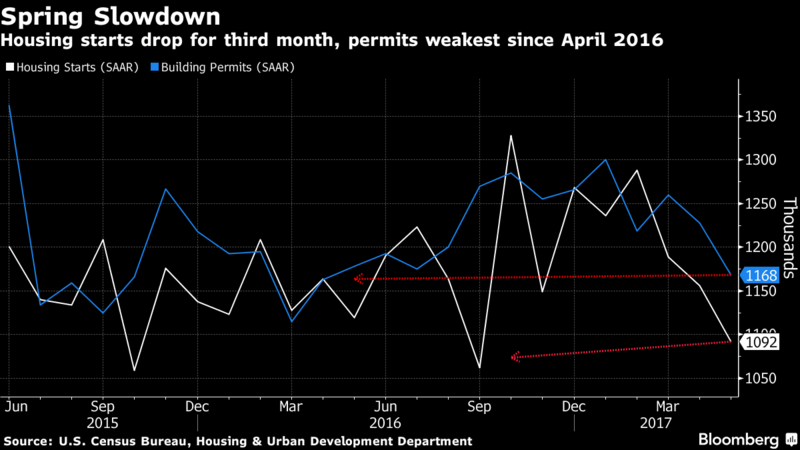

The fundamentals in the building materials sectors have been mixed, but we expect a softer tone overall going into the end of the year.

Our first downside target is at $20.40 with a bigger level of support near the November 6th low of $19.20.

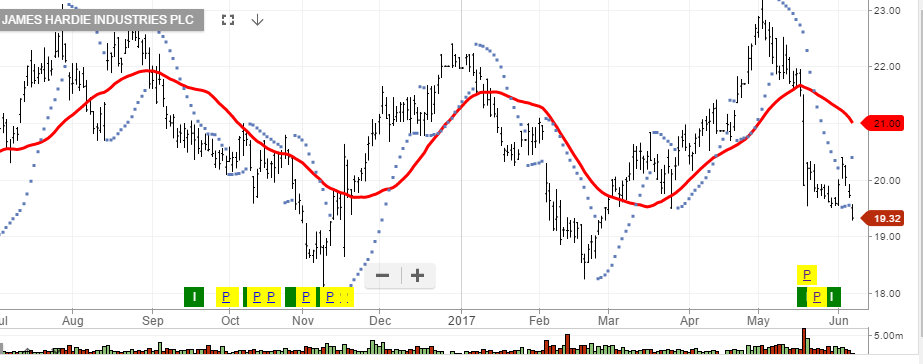

James Hardie

James Hardie

James Hardie

James Hardie

James Hardie